Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (120)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Cornell ComplaintDocumento41 páginasCornell Complaintjspector100% (1)

- Joseph Ruggiero Employment AgreementDocumento6 páginasJoseph Ruggiero Employment AgreementjspectorAinda não há avaliações

- Stat Con Interpretation and ConstructionDocumento5 páginasStat Con Interpretation and ConstructionGraziela MercadoAinda não há avaliações

- Locating and Defining The CaribbeanDocumento29 páginasLocating and Defining The CaribbeanRoberto Saladeen100% (2)

- State Health CoverageDocumento26 páginasState Health CoveragejspectorAinda não há avaliações

- Pennies For Charity 2018Documento12 páginasPennies For Charity 2018ZacharyEJWilliamsAinda não há avaliações

- IG LetterDocumento3 páginasIG Letterjspector100% (1)

- Federal Budget Fiscal Year 2017 Web VersionDocumento36 páginasFederal Budget Fiscal Year 2017 Web VersionjspectorAinda não há avaliações

- Teacher Shortage Report 05232017 PDFDocumento16 páginasTeacher Shortage Report 05232017 PDFjspectorAinda não há avaliações

- NYSCrimeReport2016 PrelimDocumento14 páginasNYSCrimeReport2016 PrelimjspectorAinda não há avaliações

- Film Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFDocumento8 páginasFilm Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFjspectorAinda não há avaliações

- Abo 2017 Annual ReportDocumento65 páginasAbo 2017 Annual ReportrkarlinAinda não há avaliações

- Inflation AllowablegrowthfactorsDocumento1 páginaInflation AllowablegrowthfactorsjspectorAinda não há avaliações

- Darweesh Cities AmicusDocumento32 páginasDarweesh Cities AmicusjspectorAinda não há avaliações

- 2017 08 18 Constitution OrderDocumento27 páginas2017 08 18 Constitution OrderjspectorAinda não há avaliações

- SNY0517 Crosstabs 052417Documento4 páginasSNY0517 Crosstabs 052417Nick ReismanAinda não há avaliações

- Oag Sed Letter Ice 2-27-17Documento3 páginasOag Sed Letter Ice 2-27-17BethanyAinda não há avaliações

- Class of 2022Documento1 páginaClass of 2022jspectorAinda não há avaliações

- Opiods 2017-04-20-By Numbers Brief No8Documento17 páginasOpiods 2017-04-20-By Numbers Brief No8rkarlinAinda não há avaliações

- 2017 School Bfast Report Online Version 3-7-17 0Documento29 páginas2017 School Bfast Report Online Version 3-7-17 0jspectorAinda não há avaliações

- Youth Cigarette and E-Cigs UseDocumento1 páginaYouth Cigarette and E-Cigs UsejspectorAinda não há avaliações

- Hiffa Settlement Agreement ExecutedDocumento5 páginasHiffa Settlement Agreement ExecutedNick Reisman0% (1)

- Schneiderman Voter Fraud Letter 022217Documento2 páginasSchneiderman Voter Fraud Letter 022217Matthew HamiltonAinda não há avaliações

- Activity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017Documento4 páginasActivity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017jspectorAinda não há avaliações

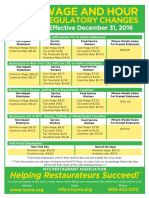

- Wage and Hour Regulatory Changes 2016Documento2 páginasWage and Hour Regulatory Changes 2016jspectorAinda não há avaliações

- Siena Poll March 27, 2017Documento7 páginasSiena Poll March 27, 2017jspectorAinda não há avaliações

- 16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsDocumento55 páginas16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsjspectorAinda não há avaliações

- Review of Executive Budget 2017Documento102 páginasReview of Executive Budget 2017Nick ReismanAinda não há avaliações

- p12 Budget Testimony 2-14-17Documento31 páginasp12 Budget Testimony 2-14-17jspectorAinda não há avaliações

- Pub Auth Num 2017Documento54 páginasPub Auth Num 2017jspectorAinda não há avaliações

- 2016 Local Sales Tax CollectionsDocumento4 páginas2016 Local Sales Tax CollectionsjspectorAinda não há avaliações

- Voting Report CardDocumento1 páginaVoting Report CardjspectorAinda não há avaliações

- Reasons For Collapse of Ottoman EmpireDocumento8 páginasReasons For Collapse of Ottoman EmpireBilal Ahmed Khan100% (2)

- Application For Social Security Card - Ss-5Documento1 páginaApplication For Social Security Card - Ss-5Casey Orvis100% (1)

- 227 - Luna vs. IACDocumento3 páginas227 - Luna vs. IACNec Salise ZabatAinda não há avaliações

- The Soviet Paradise Lost Ivan Solonevich 1938 313pgs COM - SMLDocumento313 páginasThe Soviet Paradise Lost Ivan Solonevich 1938 313pgs COM - SMLThe Rabbithole WikiAinda não há avaliações

- A 3 Commonwealth Flags Poster 2010Documento2 páginasA 3 Commonwealth Flags Poster 2010Jose MelloAinda não há avaliações

- January 2024-CompendiumDocumento98 páginasJanuary 2024-CompendiumKirti ChaudharyAinda não há avaliações

- Thuy Hoang Thi ThuDocumento8 páginasThuy Hoang Thi Thukanehai09Ainda não há avaliações

- Cbsnews 20230108 ClimateDocumento27 páginasCbsnews 20230108 ClimateCBS News PoliticsAinda não há avaliações

- Social Movements (Handout)Documento4 páginasSocial Movements (Handout)Mukti ShankarAinda não há avaliações

- Nafta Good-Bad - Michigan7 2013 PCFJVDocumento301 páginasNafta Good-Bad - Michigan7 2013 PCFJVConnor MeyerAinda não há avaliações

- (Saurabh Kumar) Polity Mains 2021 NotesDocumento197 páginas(Saurabh Kumar) Polity Mains 2021 NotesJeeshan AhmadAinda não há avaliações

- Invoice 1708 Narendra Goud Narendra GoudDocumento1 páginaInvoice 1708 Narendra Goud Narendra GoudNarendra GoudAinda não há avaliações

- HUM111 Pakistan StudiesDocumento17 páginasHUM111 Pakistan StudiesMuneebAinda não há avaliações

- Judith Butler 1997 Further Reflections On The Conversations of Our TimeDocumento4 páginasJudith Butler 1997 Further Reflections On The Conversations of Our TimeSijia GaoAinda não há avaliações

- Tesco Share Account Clean Version Final 30 10 15Documento4 páginasTesco Share Account Clean Version Final 30 10 15George DapaahAinda não há avaliações

- Appeals, 368 Phil. 412, 420 (1999)Documento5 páginasAppeals, 368 Phil. 412, 420 (1999)Vin LacsieAinda não há avaliações

- Degree Prelims Stage 2 MarkedDocumento25 páginasDegree Prelims Stage 2 MarkedDeepak JoseAinda não há avaliações

- (2014) Big Boxes, Small PaychecksDocumento18 páginas(2014) Big Boxes, Small PaychecksJordan AshAinda não há avaliações

- Form "D-1" Annual Return (See 2020-2021 General Information: Regulation 2.1.13)Documento2 páginasForm "D-1" Annual Return (See 2020-2021 General Information: Regulation 2.1.13)Shiv KumarAinda não há avaliações

- Sumbingco v. Court of AppealsDocumento2 páginasSumbingco v. Court of AppealsRubyAinda não há avaliações

- Class 8 Revolt 1857 QADocumento3 páginasClass 8 Revolt 1857 QAAK ContinentalAinda não há avaliações

- Application Form For Entry Pass H.C. LkoDocumento2 páginasApplication Form For Entry Pass H.C. LkoDivyanshu SinghAinda não há avaliações

- Hakaraia-Sj l4 May 2015Documento5 páginasHakaraia-Sj l4 May 2015api-277414148Ainda não há avaliações

- Prospective Member LetterDocumento1 páginaProspective Member LetterClinton ChanAinda não há avaliações

- Afghan National Army (ANA) : Mentor GuideDocumento76 páginasAfghan National Army (ANA) : Mentor GuidelucamorlandoAinda não há avaliações

- 00 IdeologiesDocumento4 páginas00 Ideologies朱奥晗Ainda não há avaliações

- Listening ST AnswersDocumento16 páginasListening ST AnswersHELP ACADEMYAinda não há avaliações

- Joseph Ejercito EstradaDocumento12 páginasJoseph Ejercito EstradaEricka CozAinda não há avaliações