Você também pode gostar

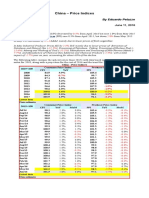

- China - Price IndicesDocumento1 páginaChina - Price IndicesEduardo PetazzeAinda não há avaliações

- México, PBI 2015Documento1 páginaMéxico, PBI 2015Eduardo PetazzeAinda não há avaliações

- WTI Spot PriceDocumento4 páginasWTI Spot PriceEduardo Petazze100% (1)

- Brazilian Foreign TradeDocumento1 páginaBrazilian Foreign TradeEduardo PetazzeAinda não há avaliações

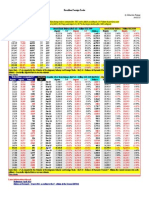

- Retail Sales in The UKDocumento1 páginaRetail Sales in The UKEduardo PetazzeAinda não há avaliações

- Euro Area - Industrial Production IndexDocumento1 páginaEuro Area - Industrial Production IndexEduardo PetazzeAinda não há avaliações

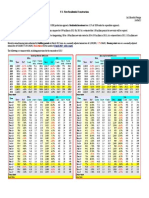

- U.S. New Residential ConstructionDocumento1 páginaU.S. New Residential ConstructionEduardo PetazzeAinda não há avaliações

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Final Year Project Query: Compiled by Moosa Naseer & Assisted by TeamDocumento3 páginasFinal Year Project Query: Compiled by Moosa Naseer & Assisted by TeamMoosa NaseerAinda não há avaliações

- Oil Refining Process Units For Sale and Relocation - All ClientsDocumento1 páginaOil Refining Process Units For Sale and Relocation - All ClientsRahim1850Ainda não há avaliações

- Adjustments of Fuel Oil SystemsDocumento16 páginasAdjustments of Fuel Oil SystemsndlongndAinda não há avaliações

- HK-1003 User ManualDocumento8 páginasHK-1003 User ManualtswAinda não há avaliações

- 2018.11.25 Grease Book FuchsDocumento18 páginas2018.11.25 Grease Book FuchsnghiaAinda não há avaliações

- Energy LectureDocumento98 páginasEnergy LecturefanusAinda não há avaliações

- Working Paper - 2015 Sulphur Impact - 5.14. 13Documento30 páginasWorking Paper - 2015 Sulphur Impact - 5.14. 13Naresh SharmaAinda não há avaliações

- Notes Chemistry XDocumento43 páginasNotes Chemistry XMM CobraAinda não há avaliações

- Cauvery Basin Seen Key Oil Region For India: Current ActionDocumento2 páginasCauvery Basin Seen Key Oil Region For India: Current ActionibrahimhomeAinda não há avaliações

- LubricantsDocumento6 páginasLubricantsVrajAinda não há avaliações

- East Coast Group - Profile2012Documento2 páginasEast Coast Group - Profile2012Ishnad ChowdhuryAinda não há avaliações

- Quality and Functions of Palm Oil - MPOCDocumento117 páginasQuality and Functions of Palm Oil - MPOCAhmad Fadzli Abdul Aziz100% (1)

- HeaterDocumento12 páginasHeaterErwin Paulian SihombingAinda não há avaliações

- Mangalore Refinery (MRPL) : Phase III Near CompletionDocumento10 páginasMangalore Refinery (MRPL) : Phase III Near CompletionDhawan SandeepAinda não há avaliações

- Anderson, W. G. - Wettability Literature SurveyDocumento97 páginasAnderson, W. G. - Wettability Literature SurveyMARCO100% (1)

- Crude Oil ContractDocumento11 páginasCrude Oil Contractillion100% (1)

- Case Studies - Proactive Managed-Pressure Drilling and Underbalanced Drilling Application in San Joaquin Wells, VenezuelaDocumento0 páginaCase Studies - Proactive Managed-Pressure Drilling and Underbalanced Drilling Application in San Joaquin Wells, VenezuelaMaulana Alan Muhammad100% (1)

- In Focus Pipe Wraps BelzonaDocumento4 páginasIn Focus Pipe Wraps BelzonaAhmed ELmlahyAinda não há avaliações

- Low Pressure Storage TanksDocumento79 páginasLow Pressure Storage TanksDeep Chaudhari100% (3)

- Red Line Synthetic 10W 60 Technical DatasheetDocumento2 páginasRed Line Synthetic 10W 60 Technical DatasheetMario FliesserAinda não há avaliações

- JPT 2020-10 PDFDocumento84 páginasJPT 2020-10 PDFRosario Villca JerezAinda não há avaliações

- 11 Time Sheet Okt - Nop 2021 Duri-KefriDocumento75 páginas11 Time Sheet Okt - Nop 2021 Duri-KefriMailbak MailbakAinda não há avaliações

- Lean Oil Absorption 01Documento14 páginasLean Oil Absorption 01Shri JrAinda não há avaliações

- 300KSDR-L2-08A-OPE - Operation Manual (Rev-4) 10-Apr-19 PDFDocumento189 páginas300KSDR-L2-08A-OPE - Operation Manual (Rev-4) 10-Apr-19 PDFThem Bui XuanAinda não há avaliações

- Briefer On Mining Laws and Issues in The PhilippinesDocumento50 páginasBriefer On Mining Laws and Issues in The PhilippinesSakuraCardCaptorAinda não há avaliações

- Technical ProposalDocumento5 páginasTechnical ProposalAmeerHamzaWarraichAinda não há avaliações

- 04 WPTDocumento86 páginas04 WPTapi-3698996Ainda não há avaliações

- A SWOT Matrix For Byco Petroleum Pakistan Limited: Strengths WeaknessesDocumento1 páginaA SWOT Matrix For Byco Petroleum Pakistan Limited: Strengths WeaknessesUsmanSarwarAinda não há avaliações

- ASTM G205-16 Standard Guide For Determining Emulsion Properties, Wetting Behavior, and Corrosion-Inhibitory Properties of Crude Oils PDFDocumento10 páginasASTM G205-16 Standard Guide For Determining Emulsion Properties, Wetting Behavior, and Corrosion-Inhibitory Properties of Crude Oils PDFSergio DiazAinda não há avaliações

- API 676 Positive Displacement P - APIDocumento52 páginasAPI 676 Positive Displacement P - APIHadi ZareiAinda não há avaliações