Você também pode gostar

- SP Meuble ConceptDocumento7 páginasSP Meuble ConceptHugoAinda não há avaliações

- Hotel Asset Management GuidefDocumento12 páginasHotel Asset Management GuidefLaurentiuAinda não há avaliações

- Map IslamabadDocumento1 páginaMap Islamabadmuhammadazmatullah100% (2)

- Practice Questions - Eqty1Documento17 páginasPractice Questions - Eqty1gauravroongtaAinda não há avaliações

- Chapter 8 Interest Rates and Bond Valuation: Corporate Finance, 12e (Ross)Documento37 páginasChapter 8 Interest Rates and Bond Valuation: Corporate Finance, 12e (Ross)ZiyadGhaziAinda não há avaliações

- "Attock Cement Pakistan LTD.": Research and Analysis ProjectDocumento36 páginas"Attock Cement Pakistan LTD.": Research and Analysis ProjectSalman Khawaja100% (1)

- Installation Manual StandaloneDocumento11 páginasInstallation Manual Standalonevarimember752Ainda não há avaliações

- Audit International Firm Training 19.01 10102017 CASEWAREDocumento226 páginasAudit International Firm Training 19.01 10102017 CASEWAREnnauthooAinda não há avaliações

- IFRS - IFRS 15 Shipping Terms Decision Tree - January 2019Documento7 páginasIFRS - IFRS 15 Shipping Terms Decision Tree - January 2019Juanito TanamorAinda não há avaliações

- Company ValuationDocumento216 páginasCompany Valuationmalvert91100% (2)

- Historical Financial Analysis - CA Rajiv SinghDocumento78 páginasHistorical Financial Analysis - CA Rajiv Singhవిజయ్ పి100% (1)

- Harley Davidson Stock ValuationDocumento43 páginasHarley Davidson Stock ValuationRahul PatelAinda não há avaliações

- NFRS IiiDocumento105 páginasNFRS Iiikaran shahiAinda não há avaliações

- IFRS 4 Insurance Contracts Phase II: Preparing For ActionDocumento53 páginasIFRS 4 Insurance Contracts Phase II: Preparing For Actionsai madhavAinda não há avaliações

- An Independent Correspondent Member ofDocumento10 páginasAn Independent Correspondent Member ofRizwanChowdhury100% (1)

- Bosse, Harrison, and HoskissonDocumento48 páginasBosse, Harrison, and HoskissonKhanh Linh HoangAinda não há avaliações

- 5011 - Worksheet - Group Audit InstructionsDocumento39 páginas5011 - Worksheet - Group Audit Instructionssinra kongAinda não há avaliações

- The Business, Tax, and Financial Environments The Business, Tax, and Financial EnvironmentsDocumento30 páginasThe Business, Tax, and Financial Environments The Business, Tax, and Financial EnvironmentsShah KhanAinda não há avaliações

- Ias 21Documento22 páginasIas 21Jayesh S BoharaAinda não há avaliações

- Accounting For InsuranceDocumento14 páginasAccounting For InsuranceJudith GabuteroAinda não há avaliações

- Accounting For Insurance Contracts - Ifrs 4: International Financial Reporting StandardsDocumento32 páginasAccounting For Insurance Contracts - Ifrs 4: International Financial Reporting StandardsKylie TarnateAinda não há avaliações

- Audit Manual - SME - 2018-19 - FormatsDocumento39 páginasAudit Manual - SME - 2018-19 - FormatsDsp VarmaAinda não há avaliações

- Sample Managment Representation LetterDocumento3 páginasSample Managment Representation LetterSONITAAinda não há avaliações

- Historical Evolution of Management Accounting and 7 TrendsDocumento6 páginasHistorical Evolution of Management Accounting and 7 TrendsEulaine Ann AlcantaraAinda não há avaliações

- Automation of Accounting Processes Impact of Artificial IntelligenceDocumento7 páginasAutomation of Accounting Processes Impact of Artificial IntelligenceLakesh kumar padhyAinda não há avaliações

- Financial Accounting and Reporting 02Documento6 páginasFinancial Accounting and Reporting 02Nuah SilvestreAinda não há avaliações

- Isre 2400Documento21 páginasIsre 2400naveedawan321Ainda não há avaliações

- Lesson 3 ABC Question Set 1231Documento17 páginasLesson 3 ABC Question Set 1231Kathryn TeoAinda não há avaliações

- Review of Internal Control Over Financial ReportingDocumento20 páginasReview of Internal Control Over Financial ReportingMark Angelo Bustos100% (1)

- PAS 1 Presentation of Financial StatementsDocumento53 páginasPAS 1 Presentation of Financial Statementsjan petosilAinda não há avaliações

- Financial Statements Based On Philippine Accounting Standards (PAS) #1Documento17 páginasFinancial Statements Based On Philippine Accounting Standards (PAS) #1Corpuz TyroneAinda não há avaliações

- Events After The Reporting Period (IAS 10)Documento16 páginasEvents After The Reporting Period (IAS 10)AbdulhafizAinda não há avaliações

- Strategic Marketing For Micro Finance InstitutionsDocumento33 páginasStrategic Marketing For Micro Finance InstitutionsKshitij JindalAinda não há avaliações

- Consolidated Financial Statement HandoutDocumento9 páginasConsolidated Financial Statement HandoutMary Jane BarramedaAinda não há avaliações

- Ias 39Documento11 páginasIas 39Muhammad Qasim FareedAinda não há avaliações

- ISA 550 & 570 - PresentationDocumento25 páginasISA 550 & 570 - Presentationsajida mohdAinda não há avaliações

- Ias 2Documento6 páginasIas 2Malik Ikram Ul HaqAinda não há avaliações

- Flowchart Symbols DefinedDocumento3 páginasFlowchart Symbols DefinedNicolás DijkstraAinda não há avaliações

- PFRS Updates For The Year 2018Documento7 páginasPFRS Updates For The Year 2018nenette cruzAinda não há avaliações

- Monitoring Icq PDFDocumento3 páginasMonitoring Icq PDFPatrick GoAinda não há avaliações

- Diff Bet USGAAP IGAAP IFRSDocumento7 páginasDiff Bet USGAAP IGAAP IFRSMichael HillAinda não há avaliações

- Chapter Five: Activity-Based Costing (ABC) and Activity-Based Management (ABM)Documento38 páginasChapter Five: Activity-Based Costing (ABC) and Activity-Based Management (ABM)Rangga PurnaAinda não há avaliações

- Update On Government Reportorial Requirements 2016Documento32 páginasUpdate On Government Reportorial Requirements 2016Rheneir MoraAinda não há avaliações

- The Balanced Scorecard: A Tool To Implement StrategyDocumento39 páginasThe Balanced Scorecard: A Tool To Implement StrategyAilene QuintoAinda não há avaliações

- IAS37Documento2 páginasIAS37Mohammad Faisal SaleemAinda não há avaliações

- List of Coop NameDocumento4 páginasList of Coop NameEdwin RustiaAinda não há avaliações

- Ias 12Documento27 páginasIas 12Kuti KuriAinda não há avaliações

- Acc 101 Module 1Documento9 páginasAcc 101 Module 1Felicity CabreraAinda não há avaliações

- Presentation On Operational AuditDocumento57 páginasPresentation On Operational AuditctcamatAinda não há avaliações

- Chapter 11 Audit Reports On Financial StatementsDocumento54 páginasChapter 11 Audit Reports On Financial StatementsKayla Sophia PatioAinda não há avaliações

- Michael Cayabyab Research 1Documento14 páginasMichael Cayabyab Research 1Michael CayabyabAinda não há avaliações

- Optional Standard Deductions ExampleDocumento7 páginasOptional Standard Deductions ExampleSandia EspejoAinda não há avaliações

- Performance ReportingDocumento62 páginasPerformance ReportingLive LoveAinda não há avaliações

- Ias 10 Events After The Reporting PeriodDocumento9 páginasIas 10 Events After The Reporting PeriodTawanda Tatenda HerbertAinda não há avaliações

- Financial StatementDocumento83 páginasFinancial StatementDarkie DrakieAinda não há avaliações

- At 04 Auditing PlanningDocumento8 páginasAt 04 Auditing PlanningJelyn RuazolAinda não há avaliações

- Ifrs 15 (Telecom Industry)Documento19 páginasIfrs 15 (Telecom Industry)Emezi Francis Obisike100% (2)

- Programme Based Budget 2016 - 2017Documento257 páginasProgramme Based Budget 2016 - 2017inyasiAinda não há avaliações

- Related Party DisclosuresDocumento15 páginasRelated Party DisclosuresArthur PlazaAinda não há avaliações

- Conceptual Framework For Financial Reporting: March 2018Documento20 páginasConceptual Framework For Financial Reporting: March 2018Mubarrach Matabalao100% (1)

- Module 1B - PFRS For Medium Entities NotesDocumento25 páginasModule 1B - PFRS For Medium Entities NotesLee SuarezAinda não há avaliações

- IAS 16 by FFQADocumento9 páginasIAS 16 by FFQAMohammad Faizan Farooq Qadri Attari0% (1)

- Engagemt LetterDocumento14 páginasEngagemt LetterAnonymous xPSEQTG0AeAinda não há avaliações

- Auditing Fundamentals Unit 1 Meaning of Auditing: Financial StatementsDocumento14 páginasAuditing Fundamentals Unit 1 Meaning of Auditing: Financial StatementsNandhakumarAinda não há avaliações

- Cash and Cash EquivalentDocumento12 páginasCash and Cash EquivalentEllenAinda não há avaliações

- Ias 16Documento4 páginasIas 16Alloysius ParilAinda não há avaliações

- 19095as36announ10377 PDFDocumento13 páginas19095as36announ10377 PDFratiAinda não há avaliações

- Retirement Benefit PlansDocumento1 páginaRetirement Benefit Plansm2mlckAinda não há avaliações

- International Islamic University IslamabadDocumento9 páginasInternational Islamic University IslamabadmuhammadazmatullahAinda não há avaliações

- Bank GuaranteesDocumento12 páginasBank Guaranteesmuhammadazmatullah100% (2)

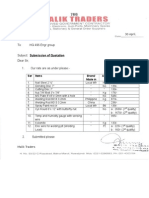

- To: HQ 496 Engr Group: Ser Items Brand/ Made in A/U Rate Per UnitDocumento1 páginaTo: HQ 496 Engr Group: Ser Items Brand/ Made in A/U Rate Per UnitmuhammadazmatullahAinda não há avaliações

- Tow Tug - Gpu TT-5000: Information Technology SolutionsDocumento1 páginaTow Tug - Gpu TT-5000: Information Technology SolutionsmuhammadazmatullahAinda não há avaliações

- List of Approved Training Organizations: TO-Code Firm Name Approved W.E.F City Name of MRT and AddressDocumento29 páginasList of Approved Training Organizations: TO-Code Firm Name Approved W.E.F City Name of MRT and AddressmuhammadazmatullahAinda não há avaliações

- Pakistan: Doing Business 2015Documento111 páginasPakistan: Doing Business 2015muhammadazmatullahAinda não há avaliações

- Voucher # Date Basis of Transactionamount: Client: Jet Stream International (PVT) Limited Year Ended: 30 June 2014Documento2 páginasVoucher # Date Basis of Transactionamount: Client: Jet Stream International (PVT) Limited Year Ended: 30 June 2014muhammadazmatullahAinda não há avaliações

- Horwath Hussain Chaudhury & Co.: Varification of Opening Balances of NCL As at 1 July 2013Documento2 páginasHorwath Hussain Chaudhury & Co.: Varification of Opening Balances of NCL As at 1 July 2013muhammadazmatullahAinda não há avaliações

- Fatima TextileDocumento124 páginasFatima TextilemuhammadazmatullahAinda não há avaliações

- Excel FunctionsDocumento4 páginasExcel FunctionsmuhammadazmatullahAinda não há avaliações

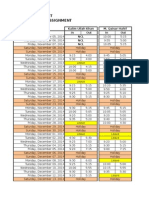

- Attendance Sheet For Tele Sehat Assignment: Kalim Ullah Khan M. Qaisar Hahif in Out in Out NCL NCL NCLDocumento4 páginasAttendance Sheet For Tele Sehat Assignment: Kalim Ullah Khan M. Qaisar Hahif in Out in Out NCL NCL NCLmuhammadazmatullahAinda não há avaliações

- Subject: Allotment of A Plot On Compassionate GroundsDocumento1 páginaSubject: Allotment of A Plot On Compassionate GroundsmuhammadazmatullahAinda não há avaliações

- FM Notes Vol1Documento1 páginaFM Notes Vol1muhammadazmatullahAinda não há avaliações

- Job Add 2009Documento1 páginaJob Add 2009muhammadazmatullahAinda não há avaliações

- Mutual FundsDocumento5 páginasMutual FundsParthAinda não há avaliações

- Bond Valuation PracticeDocumento2 páginasBond Valuation PracticeMillat Equipment Ltd PakistanAinda não há avaliações

- Instructivo para La Configuración de Material LedgerDocumento20 páginasInstructivo para La Configuración de Material LedgerStefania MarquezAinda não há avaliações

- ELEC2 - Module 1 - Fundamentals Principles of ValuationDocumento32 páginasELEC2 - Module 1 - Fundamentals Principles of ValuationMaricar PinedaAinda não há avaliações

- CFA EthicsDocumento14 páginasCFA EthicsAnnie XuAinda não há avaliações

- R2P BrochureDocumento4 páginasR2P BrochureazovkoAinda não há avaliações

- RAILROAD Joint Petition For Rulemaking To Modernize Annual Revenue Adequacy DeterminationsDocumento182 páginasRAILROAD Joint Petition For Rulemaking To Modernize Annual Revenue Adequacy DeterminationsStar News Digital MediaAinda não há avaliações

- FIN300 Course Outline, S6, F13Documento7 páginasFIN300 Course Outline, S6, F13Alex JonesAinda não há avaliações

- Chapter 01 Multinational Financial Management An OverviewDocumento45 páginasChapter 01 Multinational Financial Management An OverviewGunawan Adi Saputra0% (1)

- 2 Deenitchin PikulDocumento19 páginas2 Deenitchin Pikulwhy_1234_5678Ainda não há avaliações

- PT Adaro Energy Indonesia TBK (ADRO)Documento15 páginasPT Adaro Energy Indonesia TBK (ADRO)Arief RahmatullahAinda não há avaliações

- Valuation of Your Early Drug Candidate: by Linda Pullan, PH.DDocumento15 páginasValuation of Your Early Drug Candidate: by Linda Pullan, PH.DYinsheng XuAinda não há avaliações

- ContentServer PDFDocumento42 páginasContentServer PDFSava KovacevicAinda não há avaliações

- Investment Banking, 3E: Valuation, Lbos, M&A, and IposDocumento3 páginasInvestment Banking, 3E: Valuation, Lbos, M&A, and IposBook SittiwatAinda não há avaliações

- Chapter 3 Summary of Bussiness Valuation Approaches PDFDocumento4 páginasChapter 3 Summary of Bussiness Valuation Approaches PDFAliux CuhzAinda não há avaliações

- RigelDocumento19 páginasRigelcmlimAinda não há avaliações

- The Analysis and Valuation of Disruption: by Derek NelsonDocumento38 páginasThe Analysis and Valuation of Disruption: by Derek NelsonDiego SandersonAinda não há avaliações

- Review Book Dmbok DR YutubDocumento61 páginasReview Book Dmbok DR YutubdestiAinda não há avaliações

- Chapter 6 - Q&ADocumento17 páginasChapter 6 - Q&APro TenAinda não há avaliações

- IFRS StandardsDocumento25 páginasIFRS StandardsvarunabyAinda não há avaliações

- S2021 Financial Accounting and Reporting UK GAAPDocumento10 páginasS2021 Financial Accounting and Reporting UK GAAPChoo LeeAinda não há avaliações

- SAP S4hana Profitability Analysis (COPA)Documento124 páginasSAP S4hana Profitability Analysis (COPA)Nawair IshfaqAinda não há avaliações

- Fibonacci Trading (PDFDrive)Documento148 páginasFibonacci Trading (PDFDrive)ARK WOODYAinda não há avaliações