Você também pode gostar

- Bar Review Companion: Taxation: Anvil Law Books Series, #4No EverandBar Review Companion: Taxation: Anvil Law Books Series, #4Ainda não há avaliações

- Tax Ordinance Sub Section 114 and 115Documento4 páginasTax Ordinance Sub Section 114 and 115faiz kamranAinda não há avaliações

- 1040 Exam Prep: Module II - Basic Tax ConceptsNo Everand1040 Exam Prep: Module II - Basic Tax ConceptsNota: 1.5 de 5 estrelas1.5/5 (2)

- ITR's and AssessmentDocumento11 páginasITR's and Assessmentashutosh4iipmAinda não há avaliações

- Rules For A Tax YearDocumento5 páginasRules For A Tax YearJ Khan HotiAinda não há avaliações

- Return of IncomeDocumento9 páginasReturn of Incomes4sahithAinda não há avaliações

- Section 194LB Section 194LC Section 194LDDocumento2 páginasSection 194LB Section 194LC Section 194LDSid MehtaAinda não há avaliações

- Chapter - Registration 1. Application For Registration: Form GST Reg-01Documento10 páginasChapter - Registration 1. Application For Registration: Form GST Reg-01Abhishek MehtaAinda não há avaliações

- Application For RegistrationDocumento9 páginasApplication For RegistrationSarinAinda não há avaliações

- CST - Delhi - Rules 2005 - DelhiDocumento11 páginasCST - Delhi - Rules 2005 - DelhiRakesh SinghAinda não há avaliações

- Major Changes of Finance ActDocumento5 páginasMajor Changes of Finance ActJulia RobertAinda não há avaliações

- RMC 47-2019Documento2 páginasRMC 47-2019RichardAinda não há avaliações

- Audit Under Fiscal Laws - NotesDocumento17 páginasAudit Under Fiscal Laws - NotesabhiAinda não há avaliações

- Circulars 2009 Onreturnforms Final 10062009Documento6 páginasCirculars 2009 Onreturnforms Final 10062009api-20002381Ainda não há avaliações

- Undetaking For Remittance For NRDocumento5 páginasUndetaking For Remittance For NRhds1979Ainda não há avaliações

- Rules For NonATPDocumento4 páginasRules For NonATPsmyns.bwAinda não há avaliações

- New Form 15G Form 15H PDFDocumento6 páginasNew Form 15G Form 15H PDFdevender143Ainda não há avaliações

- Assment Audit RulsDocumento3 páginasAssment Audit RulsGovind kalsangraAinda não há avaliações

- Taxation: 4. Other Percentage TaxDocumento6 páginasTaxation: 4. Other Percentage TaxMarkuAinda não há avaliações

- Section 137 To 146aDocumento11 páginasSection 137 To 146aSher DilAinda não há avaliações

- Instructions For Filling Out FORM ITR-2Documento8 páginasInstructions For Filling Out FORM ITR-2Ganesh KumarAinda não há avaliações

- Chapter 5Documento2 páginasChapter 5Fakhar QureshiAinda não há avaliações

- Draft Refund RulesDocumento7 páginasDraft Refund RulessridharanAinda não há avaliações

- Chapter - Composition Rules 1. Intimation For Composition LevyDocumento4 páginasChapter - Composition Rules 1. Intimation For Composition LevyGuru SankarAinda não há avaliações

- Provisions For Filing of Return of IncomeDocumento17 páginasProvisions For Filing of Return of IncomeJoseph SalidoAinda não há avaliações

- Taxation Review - Samar I Electric Cooperative Vs CIRDocumento3 páginasTaxation Review - Samar I Electric Cooperative Vs CIRMaestro LazaroAinda não há avaliações

- Refund of TaxDocumento4 páginasRefund of Taxdhaval bhalodiaAinda não há avaliações

- Refund of Tax-Section 54Documento4 páginasRefund of Tax-Section 54RajgopalAinda não há avaliações

- RDO in Case of Sale of Property Thru AuctionDocumento6 páginasRDO in Case of Sale of Property Thru AuctionJohn Carlo DizonAinda não há avaliações

- Refund Under GST Regime Up To Date 12-03-2021 Detailed AnalysisDocumento17 páginasRefund Under GST Regime Up To Date 12-03-2021 Detailed AnalysisChaithanya RajuAinda não há avaliações

- Form GST RFD-01: 1. Application For Refund of Tax, Interest, Penalty, Fees or Any Other AmountDocumento7 páginasForm GST RFD-01: 1. Application For Refund of Tax, Interest, Penalty, Fees or Any Other Amountpuran1234567890Ainda não há avaliações

- TDS Not DeductDocumento6 páginasTDS Not DeductAnil WayanadAinda não há avaliações

- Administrative Provisions SEC. 236. Registration Requirements.Documento6 páginasAdministrative Provisions SEC. 236. Registration Requirements.Blanca Louise Vali ValledorAinda não há avaliações

- Deduction of Tax at Source - BComDocumento8 páginasDeduction of Tax at Source - BComAniket AgrawalAinda não há avaliações

- 12 Chapter 5Documento99 páginas12 Chapter 5Pavan SAMEER KUMARAinda não há avaliações

- Instructions For Filling Out FORM ITR-2: Page 1 of 10Documento10 páginasInstructions For Filling Out FORM ITR-2: Page 1 of 10mehtakvijayAinda não há avaliações

- Income Tax ProjectDocumento22 páginasIncome Tax ProjectGargi UpadhyayaAinda não há avaliações

- Irc XiDocumento301 páginasIrc XihenrydpsinagaAinda não há avaliações

- Assesment Procedure: By: Smriti KhannaDocumento25 páginasAssesment Procedure: By: Smriti KhannaSmriti KhannaAinda não há avaliações

- RR 5-2000 & 14-2011 ISSUANCE OF TCCs 2020 iBOOK VersionDocumento5 páginasRR 5-2000 & 14-2011 ISSUANCE OF TCCs 2020 iBOOK VersionQuinciano MorilloAinda não há avaliações

- Income Tax AsgmentDocumento9 páginasIncome Tax AsgmentPARVATHA VARTHINIAinda não há avaliações

- Section 139Documento9 páginasSection 139Mkv Downloader2Ainda não há avaliações

- Samar-I Electric Coop V CIR (2014) DigestDocumento2 páginasSamar-I Electric Coop V CIR (2014) Digestviktoriavillo67% (3)

- Form GST RFD-01: 1. Application For Refund of Tax, Interest, Penalty, Fees or Any Other AmountDocumento7 páginasForm GST RFD-01: 1. Application For Refund of Tax, Interest, Penalty, Fees or Any Other AmountSarinAinda não há avaliações

- Registration of Charges March 13 2021Documento23 páginasRegistration of Charges March 13 202125Oct 20Ainda não há avaliações

- "SEC. 52. Corporation Returns. - (C) Return of Corporation Contemplating Dissolution or Reorganization. - Every Corporation Shall, Within Thirty (30) Days After The Adoption by TheDocumento2 páginas"SEC. 52. Corporation Returns. - (C) Return of Corporation Contemplating Dissolution or Reorganization. - Every Corporation Shall, Within Thirty (30) Days After The Adoption by TheStephanie SerapioAinda não há avaliações

- 3 TdsDocumento14 páginas3 TdssugasenthilAinda não há avaliações

- PART IV Income TaxDocumento9 páginasPART IV Income TaxRahil SattarAinda não há avaliações

- BPT Regulation EnglishDocumento30 páginasBPT Regulation EnglishsamaanAinda não há avaliações

- RETURNS Under GST - Types, Applicability, Annual Returns, Matching, Final Returns With Rules CA. V.Vijay AnandDocumento8 páginasRETURNS Under GST - Types, Applicability, Annual Returns, Matching, Final Returns With Rules CA. V.Vijay Anandshahista786Ainda não há avaliações

- Restriction Imposed On Revising Wealth StatementDocumento9 páginasRestriction Imposed On Revising Wealth StatementAbid BashirAinda não há avaliações

- Samar I Electric Coop V CIR 2014 Digest 2Documento5 páginasSamar I Electric Coop V CIR 2014 Digest 2freak200% (1)

- GST-Assessment and Audit RulesDocumento4 páginasGST-Assessment and Audit RulesvishalankitAinda não há avaliações

- The Sales Tax Rules, 2006 Chapter-12Documento6 páginasThe Sales Tax Rules, 2006 Chapter-12basit_efulifeAinda não há avaliações

- 51 CI Entry RulesDocumento17 páginas51 CI Entry RulesreddyAinda não há avaliações

- Theoretical Aspects: Registration (Section 69 & Rule 4 of The Service Tax Rules, 1994)Documento54 páginasTheoretical Aspects: Registration (Section 69 & Rule 4 of The Service Tax Rules, 1994)Manish HarlalkaAinda não há avaliações

- 'Section 39 of CGST Act PDFDocumento2 páginas'Section 39 of CGST Act PDFThane GST PreventiveAinda não há avaliações

- TopicsDocumento40 páginasTopicsDa Yani ChristeeneAinda não há avaliações

- Instructions For Filling Out FORM ITR-2Documento7 páginasInstructions For Filling Out FORM ITR-2Harminder Singh DhamAinda não há avaliações

- Taxpayer'S Obligations and Privileges: I. General Audit Procedures and DocumentationDocumento4 páginasTaxpayer'S Obligations and Privileges: I. General Audit Procedures and DocumentationKristen StewartAinda não há avaliações

- 2020 08 28 Annual Procurement Plan 2020 21Documento4 páginas2020 08 28 Annual Procurement Plan 2020 21Fakhar QureshiAinda não há avaliações

- Housing Finance Prudential RegulationsDocumento14 páginasHousing Finance Prudential RegulationsFakhar QureshiAinda não há avaliações

- Jubilee General Insurance (Unit 3)Documento1 páginaJubilee General Insurance (Unit 3)Fakhar QureshiAinda não há avaliações

- Us153 Exmeption Jan-Jun'2016 (F)Documento8 páginasUs153 Exmeption Jan-Jun'2016 (F)Fakhar QureshiAinda não há avaliações

- Housing Finance Prudential RegulationsDocumento14 páginasHousing Finance Prudential RegulationsFakhar QureshiAinda não há avaliações

- 2020 08 28 Annual Procurement Plan 2020 21Documento4 páginas2020 08 28 Annual Procurement Plan 2020 21Fakhar QureshiAinda não há avaliações

- Jubilee General Insurance (Unit 3)Documento1 páginaJubilee General Insurance (Unit 3)Fakhar QureshiAinda não há avaliações

- Training Nomination (Engine)Documento1 páginaTraining Nomination (Engine)Fakhar QureshiAinda não há avaliações

- Financial Management Process 03 22 2012Documento9 páginasFinancial Management Process 03 22 2012Talayeh GhofraniAinda não há avaliações

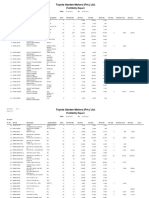

- Profitiblityreport 1Documento17 páginasProfitiblityreport 1Fakhar QureshiAinda não há avaliações

- Document PDFDocumento1 páginaDocument PDFFakhar QureshiAinda não há avaliações

- Toyota Garden Motors (PVT) LTD.: Form 17Documento2 páginasToyota Garden Motors (PVT) LTD.: Form 17Fakhar QureshiAinda não há avaliações

- Role and Responsibilities HR Executive in A Company: 1. RecruitmentDocumento3 páginasRole and Responsibilities HR Executive in A Company: 1. RecruitmentAkhil B SinghAinda não há avaliações

- TempDocumento2 páginasTempFakhar QureshiAinda não há avaliações

- System of Financail Control & Budgeting 2006Documento47 páginasSystem of Financail Control & Budgeting 2006jamilkiani70% (10)

- Essentials of A More Secure Retirement: Get Started Keep It Going Invest Wisely Retire WellDocumento5 páginasEssentials of A More Secure Retirement: Get Started Keep It Going Invest Wisely Retire WellFakhar QureshiAinda não há avaliações

- Dealership Agreement Autos AskariDocumento9 páginasDealership Agreement Autos AskariFakhar QureshiAinda não há avaliações

- Bio Data Form CiviliansDocumento1 páginaBio Data Form CiviliansSadatullah LodhiAinda não há avaliações

- Withholdingtaxes RatescardDocumento18 páginasWithholdingtaxes RatescardTauqeer AhmedAinda não há avaliações

- ProfitiblityreportDocumento19 páginasProfitiblityreportFakhar QureshiAinda não há avaliações

- 11-Withholding Rules 2012Documento5 páginas11-Withholding Rules 2012Imran MemonAinda não há avaliações

- 9-Adjudication and AppealsDocumento6 páginas9-Adjudication and AppealsFakhar QureshiAinda não há avaliações

- System of Financail Control & Budgeting 2006Documento47 páginasSystem of Financail Control & Budgeting 2006jamilkiani70% (10)

- 6 Computerized SystemDocumento4 páginas6 Computerized SystemImran MemonAinda não há avaliações

- Chapter 11Documento6 páginasChapter 11Fakhar QureshiAinda não há avaliações

- Chapter12 PRADocumento6 páginasChapter12 PRAFakhar QureshiAinda não há avaliações

- 3-Filing of ReturnsDocumento8 páginas3-Filing of ReturnsImran MemonAinda não há avaliações

- Chapter 5Documento2 páginasChapter 5Fakhar QureshiAinda não há avaliações

- Noon Sugar Annual Report 2013Documento53 páginasNoon Sugar Annual Report 2013Fakhar QureshiAinda não há avaliações

- BHU Registration Form Con 2Documento2 páginasBHU Registration Form Con 2kullsAinda não há avaliações

- Payments Can Be Made Using Visa, Mastercard and Discover: Credit Card Payment FormDocumento1 páginaPayments Can Be Made Using Visa, Mastercard and Discover: Credit Card Payment FormLionel BoopathiAinda não há avaliações

- IMPS Process FlowDocumento12 páginasIMPS Process FlowThamil Inian100% (1)

- BB0019-IncomeTax Valuation PerquisitesDocumento314 páginasBB0019-IncomeTax Valuation PerquisitesMohammed Abu ObaidahAinda não há avaliações

- Yatra Bill Format 26-03-2021Documento1 páginaYatra Bill Format 26-03-2021RiteshAinda não há avaliações

- Which of The Following Is The Correct Tax Implication of The Foregoing Data With Respect To Payment of Income Tax?Documento3 páginasWhich of The Following Is The Correct Tax Implication of The Foregoing Data With Respect To Payment of Income Tax?ROSEMARIE CRUZAinda não há avaliações

- October 2010 Business Law & Taxation Final Pre-BoardDocumento11 páginasOctober 2010 Business Law & Taxation Final Pre-BoardPatrick ArazoAinda não há avaliações

- Hero 22734BD23V227Documento2 páginasHero 22734BD23V227hariAinda não há avaliações

- RR No. 1-2022Documento3 páginasRR No. 1-2022try saguilotAinda não há avaliações

- Yuktha101Documento199 páginasYuktha101yukthaAinda não há avaliações

- MeralcoDocumento2 páginasMeralcoTheo Amadeus100% (4)

- Partner's Instructions For Schedule K-1 (Form 1065) : Internal Revenue ServiceDocumento10 páginasPartner's Instructions For Schedule K-1 (Form 1065) : Internal Revenue ServiceIRSAinda não há avaliações

- SPHM - Cashier HandbookDocumento14 páginasSPHM - Cashier HandbookSPHM HospitalityAinda não há avaliações

- StatementsDocumento2 páginasStatementsFIRST FIRSAinda não há avaliações

- Letter of Intent - DIQ ProgramDocumento1 páginaLetter of Intent - DIQ ProgramrajaAinda não há avaliações

- Income TaxationDocumento13 páginasIncome TaxationJpagAinda não há avaliações

- International Tax EnvironmentDocumento14 páginasInternational Tax EnvironmentAnonymous VstguMKrb50% (2)

- Concise Selina Solutions For Class 9 Maths Chapter 3 Compound Interest Using FormulaDocumento42 páginasConcise Selina Solutions For Class 9 Maths Chapter 3 Compound Interest Using FormulaNarayanamurthy AmirapuAinda não há avaliações

- AmazonDocumento1 páginaAmazonArijit NagAinda não há avaliações

- Section 10 (34) Dividend ExemptionDocumento2 páginasSection 10 (34) Dividend ExemptionNarender MOdiAinda não há avaliações

- BIR Form No. 0605 (2021)Documento1 páginaBIR Form No. 0605 (2021)Nathan Veracruz100% (1)

- Appendix 32 BrgyDocumento4 páginasAppendix 32 BrgyJovelyn SeseAinda não há avaliações

- Purchase GST Nagarajan GodownDocumento4 páginasPurchase GST Nagarajan GodownsamaadhuAinda não há avaliações

- Point of Sale PoSDocumento21 páginasPoint of Sale PoSBenhur LeoAinda não há avaliações

- Summary of Cooper Tire & Rubber Company's Financial and Operating Performance, 2009$2013 (Dollar Amounts in Millions, Except Per Share Data)Documento4 páginasSummary of Cooper Tire & Rubber Company's Financial and Operating Performance, 2009$2013 (Dollar Amounts in Millions, Except Per Share Data)Sanjaya WijesekareAinda não há avaliações

- Fractional Share FormulaDocumento1 páginaFractional Share FormulainboxnewsAinda não há avaliações

- Wahab UpdateDocumento1 páginaWahab UpdateSumairAinda não há avaliações

- Dollar Rate Pkistan - Google SearchDocumento1 páginaDollar Rate Pkistan - Google SearchMubashir Mubashir AhmedAinda não há avaliações

- Quezon City v. ABS CBNDocumento4 páginasQuezon City v. ABS CBNJunmer OrtizAinda não há avaliações

- Tax Invoice: Excitel Broadband Pvt. LTDDocumento1 páginaTax Invoice: Excitel Broadband Pvt. LTDSeema BhagatAinda não há avaliações

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesAinda não há avaliações

- Lower Your Taxes - BIG TIME! 2023-2024: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderNo EverandLower Your Taxes - BIG TIME! 2023-2024: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderAinda não há avaliações

- Founding Finance: How Debt, Speculation, Foreclosures, Protests, and Crackdowns Made Us a NationNo EverandFounding Finance: How Debt, Speculation, Foreclosures, Protests, and Crackdowns Made Us a NationAinda não há avaliações

- Tax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProNo EverandTax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProNota: 4.5 de 5 estrelas4.5/5 (43)

- How to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsNo EverandHow to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsAinda não há avaliações

- Small Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyNo EverandSmall Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyAinda não há avaliações

- What Your CPA Isn't Telling You: Life-Changing Tax StrategiesNo EverandWhat Your CPA Isn't Telling You: Life-Changing Tax StrategiesNota: 4 de 5 estrelas4/5 (9)

- The Tax and Legal Playbook: Game-Changing Solutions To Your Small Business Questions 2nd EditionNo EverandThe Tax and Legal Playbook: Game-Changing Solutions To Your Small Business Questions 2nd EditionNota: 5 de 5 estrelas5/5 (27)

- The Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyNo EverandThe Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyNota: 4 de 5 estrelas4/5 (52)

- Taxes for Small Business: The Ultimate Guide to Small Business Taxes Including LLC Taxes, Payroll Taxes, and Self-Employed Taxes as a Sole ProprietorshipNo EverandTaxes for Small Business: The Ultimate Guide to Small Business Taxes Including LLC Taxes, Payroll Taxes, and Self-Employed Taxes as a Sole ProprietorshipAinda não há avaliações

- Lower Your Taxes - BIG TIME! 2019-2020: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderNo EverandLower Your Taxes - BIG TIME! 2019-2020: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderNota: 5 de 5 estrelas5/5 (4)

- Decrypting Crypto Taxes: The Complete Guide to Cryptocurrency and NFT TaxationNo EverandDecrypting Crypto Taxes: The Complete Guide to Cryptocurrency and NFT TaxationAinda não há avaliações

- The Hidden Wealth of Nations: The Scourge of Tax HavensNo EverandThe Hidden Wealth of Nations: The Scourge of Tax HavensNota: 4 de 5 estrelas4/5 (11)

- Taxes Have Consequences: An Income Tax History of the United StatesNo EverandTaxes Have Consequences: An Income Tax History of the United StatesAinda não há avaliações

- Public Finance: Legal Aspects: Collective monographNo EverandPublic Finance: Legal Aspects: Collective monographAinda não há avaliações

- Bookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessNo EverandBookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessNota: 5 de 5 estrelas5/5 (5)

- Taxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingNo EverandTaxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingNota: 5 de 5 estrelas5/5 (3)

- Beat Estate Tax Forever: The Unprecedented $5 Million Opportunity in 2012No EverandBeat Estate Tax Forever: The Unprecedented $5 Million Opportunity in 2012Ainda não há avaliações

- The Great Multinational Tax Rort: how we’re all being robbedNo EverandThe Great Multinational Tax Rort: how we’re all being robbedAinda não há avaliações

- Make Sure It's Deductible: Little-Known Tax Tips for Your Canadian Small Business, Fifth EditionNo EverandMake Sure It's Deductible: Little-Known Tax Tips for Your Canadian Small Business, Fifth EditionAinda não há avaliações

- U.S. Taxes for Worldly Americans: The Traveling Expat's Guide to Living, Working, and Staying Tax Compliant AbroadNo EverandU.S. Taxes for Worldly Americans: The Traveling Expat's Guide to Living, Working, and Staying Tax Compliant AbroadAinda não há avaliações

- Bookkeeping for Small Business: The Most Complete and Updated Guide with Tips and Tricks to Track Income & Expenses and Prepare for TaxesNo EverandBookkeeping for Small Business: The Most Complete and Updated Guide with Tips and Tricks to Track Income & Expenses and Prepare for TaxesAinda não há avaliações

- Canadian International Taxation: Income Tax Rules for ResidentsNo EverandCanadian International Taxation: Income Tax Rules for ResidentsAinda não há avaliações

- The Tax and Legal Playbook: Game-Changing Solutions To Your Small Business QuestionsNo EverandThe Tax and Legal Playbook: Game-Changing Solutions To Your Small Business QuestionsNota: 3.5 de 5 estrelas3.5/5 (9)