Você também pode gostar

- The Offical DVSA Guide to Driving Goods Vehicles: DVSA Safe Driving for Life SeriesNo EverandThe Offical DVSA Guide to Driving Goods Vehicles: DVSA Safe Driving for Life SeriesNota: 5 de 5 estrelas5/5 (1)

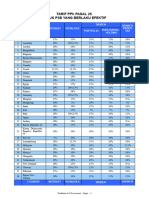

- Government Money Payments Chart - BirDocumento3 páginasGovernment Money Payments Chart - BirVan Caz89% (9)

- Tds Rates As Per DtaaDocumento3 páginasTds Rates As Per DtaamahiAinda não há avaliações

- Double Taxation - Rates of WithholdingDocumento6 páginasDouble Taxation - Rates of Withholdingunderstated1313100% (1)

- Tax TreatyDocumento54 páginasTax TreatyDevin WinataAinda não há avaliações

- Midterm Assignment No. 3Documento3 páginasMidterm Assignment No. 3XaxxyAinda não há avaliações

- Ringkasan Tarif P3B: Tax Learning: Tax Resume Ringkasan Tax TreatyDocumento2 páginasRingkasan Tarif P3B: Tax Learning: Tax Resume Ringkasan Tax TreatyAchmad MudaniAinda não há avaliações

- Fiscal Guide Mauritius PDFDocumento7 páginasFiscal Guide Mauritius PDFlito77Ainda não há avaliações

- Luxembourg - Treaty Withholding Rates DividendsDocumento4 páginasLuxembourg - Treaty Withholding Rates DividendscyrillekurzajAinda não há avaliações

- Tarif Pasal 26Documento2 páginasTarif Pasal 26lelaleria11Ainda não há avaliações

- Tax Notes Aug 10-11Documento15 páginasTax Notes Aug 10-11Reiner NuludAinda não há avaliações

- Botswana Withholding Tax RatesDocumento4 páginasBotswana Withholding Tax Ratesjiwon leeAinda não há avaliações

- Botswana Tax SummaryDocumento1 páginaBotswana Tax SummarydaveAinda não há avaliações

- Ghana Fiscal Guide 2015 2016Documento10 páginasGhana Fiscal Guide 2015 2016batuchemAinda não há avaliações

- TAXATION in INDIADocumento11 páginasTAXATION in INDIAChaitanya PatilAinda não há avaliações

- Ghana Double Taxation and Double Taxation TreatiesDocumento6 páginasGhana Double Taxation and Double Taxation Treatiesbr942vhj8xAinda não há avaliações

- Deloitte Tanzania GuideDocumento13 páginasDeloitte Tanzania GuideVenkatesh GorurAinda não há avaliações

- Myanmar Tax StructureDocumento20 páginasMyanmar Tax StructureYe PhoneAinda não há avaliações

- Tarif Tax TreatyDocumento2 páginasTarif Tax TreatyJokoWidodo0% (1)

- TX Text Control WordsDocumento2 páginasTX Text Control Wordsritter.sjdAinda não há avaliações

- Application of WHT Under The Double Taxation AgreementDocumento19 páginasApplication of WHT Under The Double Taxation Agreementrizzwan4uAinda não há avaliações

- Calculation of Risk in Case of Projects Being Executed by State Govt. Cost of Transferred RiskDocumento4 páginasCalculation of Risk in Case of Projects Being Executed by State Govt. Cost of Transferred RiskRajesh GoelAinda não há avaliações

- Taxation of Cross Border ActivitiesDocumento5 páginasTaxation of Cross Border ActivitiesTriila manillaAinda não há avaliações

- TDS & TCS Rates (F.Y-2011-12)Documento2 páginasTDS & TCS Rates (F.Y-2011-12)ca_atulAinda não há avaliações

- Epayments Import TemplateDocumento6 páginasEpayments Import TemplateMohammad MohsinAinda não há avaliações

- f6vnm 2015dec Q PDFDocumento16 páginasf6vnm 2015dec Q PDFSinhAinda não há avaliações

- Tax Codes (WHT)Documento1 páginaTax Codes (WHT)m.wamiqsuhailAinda não há avaliações

- Compliance HandBook FY 2015-16Documento32 páginasCompliance HandBook FY 2015-16sunru24Ainda não há avaliações

- Fit Income TaxDocumento8 páginasFit Income TaxadrianoedwardjosephAinda não há avaliações

- CAclubindia News - Income Tax Sections at A GlanceDocumento3 páginasCAclubindia News - Income Tax Sections at A GlanceSmiju SukumarAinda não há avaliações

- W14 Module 12withholding TaxesDocumento7 páginasW14 Module 12withholding Taxescamille ducutAinda não há avaliações

- Final TDS and Tax ExemptionsDocumento4 páginasFinal TDS and Tax Exemptionsdpak bhusalAinda não há avaliações

- F6PKN QPDocumento14 páginasF6PKN QPمحمد شمائل چیمہAinda não há avaliações

- FGFGDocumento13 páginasFGFGamir farooquiAinda não há avaliações

- Taxation System in TanzaniaDocumento9 páginasTaxation System in TanzaniaSadickAinda não há avaliações

- Final Income TaxationDocumento4 páginasFinal Income TaxationJean Diane Jovelo100% (1)

- %age Increase / (Decrease) Over Last Year Yr-1 Yr-2 Yr-3 Yr-4 Yr-5Documento6 páginas%age Increase / (Decrease) Over Last Year Yr-1 Yr-2 Yr-3 Yr-4 Yr-5Muhammad BilalAinda não há avaliações

- SUMMARYDocumento3 páginasSUMMARYShine SencilAinda não há avaliações

- Infographics - TaxDocumento12 páginasInfographics - TaxPablo InocencioAinda não há avaliações

- Fiscal Guide TanzaniaDocumento12 páginasFiscal Guide TanzaniaVenkatesh GorurAinda não há avaliações

- Direct Taxes Withholding Tax Rate Card - Tax Year 2014 & 2015Documento2 páginasDirect Taxes Withholding Tax Rate Card - Tax Year 2014 & 2015Riaz AhmedAinda não há avaliações

- New Payment Sections TemplateDocumento1 páginaNew Payment Sections Templateiaeste20078797Ainda não há avaliações

- F6PKN 2015 Jun QDocumento17 páginasF6PKN 2015 Jun QRihamAinda não há avaliações

- Shedule of ChargessDocumento13 páginasShedule of ChargessalirezaAinda não há avaliações

- List of Rates of Withholding Tax of Dividends, Interest and Royalties Under The Respective Tax TreatiesDocumento2 páginasList of Rates of Withholding Tax of Dividends, Interest and Royalties Under The Respective Tax TreatiesvictorchangAinda não há avaliações

- Tax Rates As Per IT Act Vis A Vis Tax TreatiesDocumento14 páginasTax Rates As Per IT Act Vis A Vis Tax TreatiesEswarReddyEegaAinda não há avaliações

- Another Fine Mess For African TelecomsDocumento8 páginasAnother Fine Mess For African TelecomsPNG networksAinda não há avaliações

- NO Nation Branch Profit Tax Dividends BPT Rate Exception For SPC Dividends PortfolioDocumento4 páginasNO Nation Branch Profit Tax Dividends BPT Rate Exception For SPC Dividends PortfolioSatrio YuliawanAinda não há avaliações

- Final Tax Lecture PDFDocumento7 páginasFinal Tax Lecture PDFMarlo Caluya ManuelAinda não há avaliações

- Final Tax LectureDocumento7 páginasFinal Tax LectureJefrey Jismen Ballesteros100% (1)

- Ghana - Corporate - Withholding TaxesDocumento3 páginasGhana - Corporate - Withholding TaxesFrancisAinda não há avaliações

- RateDocumento3 páginasRatemikamiiAinda não há avaliações

- Lataxnet MANAGING CORPORATE TAXATION IN LATIN AMERICA 2022 - FinalDocumento368 páginasLataxnet MANAGING CORPORATE TAXATION IN LATIN AMERICA 2022 - FinalMarcos RiveraAinda não há avaliações

- Withholding Taxes Learning ObjectivesDocumento8 páginasWithholding Taxes Learning ObjectivesAce AlquinAinda não há avaliações

- What Is TRAIN?: Tax ReformDocumento10 páginasWhat Is TRAIN?: Tax ReformZyki Zamora LacdaoAinda não há avaliações

- How Do You See It?: East Africa Quick Tax Guide 2012Documento11 páginasHow Do You See It?: East Africa Quick Tax Guide 2012Zimbo KigoAinda não há avaliações

- Quick Method Accounting RatesDocumento4 páginasQuick Method Accounting RatesRaviAinda não há avaliações

- Tds Rate Chart 13 14Documento4 páginasTds Rate Chart 13 14rockyrrAinda não há avaliações

- Tax and MSMEs in the Digital Age: Why Do We Need To Pay Taxes And What Are The Benefits For Us As MSME Entrepreneurs And How To Build Regulations That Are Empathetic And Proven To Encourage Tax Revenue In The Informal SectorNo EverandTax and MSMEs in the Digital Age: Why Do We Need To Pay Taxes And What Are The Benefits For Us As MSME Entrepreneurs And How To Build Regulations That Are Empathetic And Proven To Encourage Tax Revenue In The Informal SectorAinda não há avaliações

- CDL Study Guide: Complete manual from A to Z on everything you need to know to pass the commercial driver's license examNo EverandCDL Study Guide: Complete manual from A to Z on everything you need to know to pass the commercial driver's license examAinda não há avaliações

- Pex 03 02Documento5 páginasPex 03 02aexillis0% (1)

- Anilkumar Surendran 3-AdDocumento4 páginasAnilkumar Surendran 3-AdAnil AmbalapuzhaAinda não há avaliações

- 9.LearnEnglish Writing A2 Instructions For A Colleague PDFDocumento5 páginas9.LearnEnglish Writing A2 Instructions For A Colleague PDFوديع القباطيAinda não há avaliações

- HGP Year End Report 2021-2022 NewDocumento169 páginasHGP Year End Report 2021-2022 Newangelica sungaAinda não há avaliações

- SAP HR and Payroll Wage TypesDocumento3 páginasSAP HR and Payroll Wage TypesBharathk Kld0% (1)

- Ekoplastik PPR Catalogue of ProductsDocumento36 páginasEkoplastik PPR Catalogue of ProductsFlorin Maria ChirilaAinda não há avaliações

- Board of DirectorsDocumento2 páginasBoard of DirectorsjonahsalvadorAinda não há avaliações

- The Messenger 190Documento76 páginasThe Messenger 190European Southern ObservatoryAinda não há avaliações

- Barclays Personal Savings AccountsDocumento10 páginasBarclays Personal Savings AccountsTHAinda não há avaliações

- 3500 Ha027988 7Documento384 páginas3500 Ha027988 7Gigi ZitoAinda não há avaliações

- EWC 662 English Writing Critical Group Work Portfolio: Submitted ToDocumento31 páginasEWC 662 English Writing Critical Group Work Portfolio: Submitted ToNurul Nadia MuhamadAinda não há avaliações

- Ben ChanDocumento2 páginasBen ChanAlibabaAinda não há avaliações

- Review Women With Moustaches and Men Without Beards - Gender and Sexual Anxieties of Iranian Modernity PDFDocumento3 páginasReview Women With Moustaches and Men Without Beards - Gender and Sexual Anxieties of Iranian Modernity PDFBilal SalaamAinda não há avaliações

- Slides 5 - Disposal and AppraisalDocumento77 páginasSlides 5 - Disposal and AppraisalRave OcampoAinda não há avaliações

- Vocabulary: ExileDocumento5 páginasVocabulary: ExileWael MadyAinda não há avaliações

- 16.3 - Precipitation and The Solubility Product - Chemistry LibreTextsDocumento14 páginas16.3 - Precipitation and The Solubility Product - Chemistry LibreTextsThereAinda não há avaliações

- WP Seagull Open Source Tool For IMS TestingDocumento7 páginasWP Seagull Open Source Tool For IMS Testingsourchhabs25Ainda não há avaliações

- Sri Anjaneya Cotton Mills LimitedDocumento63 páginasSri Anjaneya Cotton Mills LimitedPrashanth PB50% (2)

- Unit 6 - ListeningDocumento11 páginasUnit 6 - Listeningtoannv8187Ainda não há avaliações

- Osssc JR Clerk Odia Paper 2015 - 20171207 - 0001Documento7 páginasOsssc JR Clerk Odia Paper 2015 - 20171207 - 0001songspk100Ainda não há avaliações

- Micron Serial NOR Flash Memory: 3V, Multiple I/O, 4KB Sector Erase N25Q256A FeaturesDocumento92 páginasMicron Serial NOR Flash Memory: 3V, Multiple I/O, 4KB Sector Erase N25Q256A FeaturesAEAinda não há avaliações

- Technik: RefraDocumento54 páginasTechnik: Reframustaf100% (1)

- Pre-Colonial Philippine ArtDocumento5 páginasPre-Colonial Philippine Artpaulinavera100% (5)

- Datasheet - Ewon Cosy 131Documento3 páginasDatasheet - Ewon Cosy 131Omar AzzainAinda não há avaliações

- Admission Prospectus2022 1 PDFDocumento10 páginasAdmission Prospectus2022 1 PDFstudymba2024Ainda não há avaliações

- TV ExplorerDocumento2 páginasTV Explorerdan r.Ainda não há avaliações

- The USP AdvantageDocumento30 páginasThe USP AdvantageGabriel A. RamírezAinda não há avaliações

- Netflix Annual Report 2010Documento76 páginasNetflix Annual Report 2010Arman AliAinda não há avaliações

- Flexure Hinge Mechanisms Modeled by Nonlinear Euler-Bernoulli-BeamsDocumento2 páginasFlexure Hinge Mechanisms Modeled by Nonlinear Euler-Bernoulli-BeamsMobile SunAinda não há avaliações

- 08 BQ - PADSB - Elect - P2 - R2 (Subcon Empty BQ)Documento89 páginas08 BQ - PADSB - Elect - P2 - R2 (Subcon Empty BQ)Middle EastAinda não há avaliações