Você também pode gostar

- Income Statement Account Amount (DR/CR) Balance Sheet AccountDocumento20 páginasIncome Statement Account Amount (DR/CR) Balance Sheet Accountmanpreet0% (1)

- Form 11 Revised FormatDocumento3 páginasForm 11 Revised FormatParth UpadhyayAinda não há avaliações

- Form 11 Revised FormatDocumento3 páginasForm 11 Revised FormatParth UpadhyayAinda não há avaliações

- Guide To Accounting For Income Taxes (PWC - 2nd Edition 2015)Documento717 páginasGuide To Accounting For Income Taxes (PWC - 2nd Edition 2015)Piseth Chen100% (1)

- Oil and Gas Company ProfileDocumento4 páginasOil and Gas Company ProfileAhmed Ali Alsubaih0% (2)

- 1 Finance-Exam-1Documento22 páginas1 Finance-Exam-1ashish25% (4)

- Why Is The BSP The Main Government Agency Responsible For Promoting Price StabilityDocumento4 páginasWhy Is The BSP The Main Government Agency Responsible For Promoting Price StabilityMarielle CatiisAinda não há avaliações

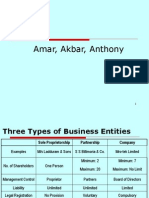

- Forms of Business EntityDocumento20 páginasForms of Business EntityMain Daiictian HuAinda não há avaliações

- KjjuDocumento237 páginasKjjuGuy Rider50% (2)

- Double Entry BookkeepingDocumento19 páginasDouble Entry BookkeepingCanduman NhsAinda não há avaliações

- EscrowDocumento1 páginaEscrowJason HenryAinda não há avaliações

- GAAP Accounting Rules For Expensing SamplesDocumento4 páginasGAAP Accounting Rules For Expensing SamplesNataraj ShanoboghAinda não há avaliações

- Master POA Sample Book PDFDocumento20 páginasMaster POA Sample Book PDFwjpodjoaspodjadAinda não há avaliações

- Terminology Balance SheetDocumento3 páginasTerminology Balance SheetMarcel Díaz AdriàAinda não há avaliações

- Accounting BasicsDocumento26 páginasAccounting BasicsAziz MalikAinda não há avaliações

- 10 Depreciation and Income TaxDocumento53 páginas10 Depreciation and Income TaxDyahKuntiSuryaAinda não há avaliações

- Full Deposition of The Soon To Be Infamous Cheryl Samons RE Deutsche Bank National Trust Company, As Trustee For Morgan Stanley ABS Capital Inc, Plaintiff, vs. Belourdes Pierre - 50 2008 CA 02855Documento138 páginasFull Deposition of The Soon To Be Infamous Cheryl Samons RE Deutsche Bank National Trust Company, As Trustee For Morgan Stanley ABS Capital Inc, Plaintiff, vs. Belourdes Pierre - 50 2008 CA 02855Foreclosure Fraud100% (1)

- Local Rules Master FileDocumento179 páginasLocal Rules Master FileAlex ProtivnakAinda não há avaliações

- Real AccountingDocumento22 páginasReal Accountingakbar2jAinda não há avaliações

- General Ledger: General Ledger 1. What Are The Key Functions Provided by GL?Documento9 páginasGeneral Ledger: General Ledger 1. What Are The Key Functions Provided by GL?1sacAinda não há avaliações

- 2.double-Entry Recording Process - CLCDocumento48 páginas2.double-Entry Recording Process - CLCTrang NguyenAinda não há avaliações

- c06 895867Documento34 páginasc06 895867api-246246921Ainda não há avaliações

- Book Keeping MaterialsDocumento64 páginasBook Keeping MaterialsAmanda Watson100% (1)

- ERP Financial Accounting Accelerator With SAP HANADocumento6 páginasERP Financial Accounting Accelerator With SAP HANAtekzAinda não há avaliações

- Diploma in Islamic Banking (Dib) : S/N TopicDocumento76 páginasDiploma in Islamic Banking (Dib) : S/N TopicRezaul AlamAinda não há avaliações

- Accounting Principles: Rapid ReviewDocumento3 páginasAccounting Principles: Rapid ReviewAhmedNiazAinda não há avaliações

- Accounting For Oracle Receivables: Flow of Accounting InformationDocumento10 páginasAccounting For Oracle Receivables: Flow of Accounting InformationAhmed Aljack SulimanAinda não há avaliações

- About The Canadian Banking IndustryDocumento6 páginasAbout The Canadian Banking IndustryChiChi ZhangAinda não há avaliações

- 8A. Role of AccountingDocumento11 páginas8A. Role of AccountingsymhoutAinda não há avaliações

- IBM - E20-8058 Basic Accounting Concepts 1961Documento50 páginasIBM - E20-8058 Basic Accounting Concepts 1961shivanadhunichaitany100% (2)

- Accounting Crash CourseDocumento7 páginasAccounting Crash CourseschmooflaAinda não há avaliações

- Aicpa - New Cpa Exam ReportDocumento119 páginasAicpa - New Cpa Exam ReportLương Thế CườngAinda não há avaliações

- Chart of Accounts: Home BlogDocumento5 páginasChart of Accounts: Home BlogJose Luis Becerril BurgosAinda não há avaliações

- Principles of Book-Keeping: Accounting EntriesDocumento42 páginasPrinciples of Book-Keeping: Accounting EntriesJanine padronesAinda não há avaliações

- Medium Term Finance (Loan) Is Usually Provided FromDocumento19 páginasMedium Term Finance (Loan) Is Usually Provided FromAntora HoqueAinda não há avaliações

- Glencoe Accounting Chp26Documento28 páginasGlencoe Accounting Chp26louise carino100% (1)

- Cerdit TypesDocumento16 páginasCerdit TypesKarthigaiselvan ShanmuganathanAinda não há avaliações

- Bookkeeping To Trial Balance 9Documento17 páginasBookkeeping To Trial Balance 9elelwaniAinda não há avaliações

- Addendum To Real Estate Purchas and Sale Agreement PDFDocumento1 páginaAddendum To Real Estate Purchas and Sale Agreement PDFGabe CoyneAinda não há avaliações

- Accounts Receivable Process Diagnostic QuestionnaireDocumento13 páginasAccounts Receivable Process Diagnostic QuestionnaireRodney LabayAinda não há avaliações

- Bank of America, NT & SA, Petitioner, vs. COURT OF Appeals, Inter-Resin Industrial Corporation, Francisco Trajano, John Doe and Jane DOE, RespondentsDocumento29 páginasBank of America, NT & SA, Petitioner, vs. COURT OF Appeals, Inter-Resin Industrial Corporation, Francisco Trajano, John Doe and Jane DOE, Respondentseasa^belleAinda não há avaliações

- Triple-Entry AccountingDocumento3 páginasTriple-Entry AccountingPrateik Ryuki100% (1)

- Accounting Exercise: Part 1: Basic TransactionsDocumento7 páginasAccounting Exercise: Part 1: Basic TransactionsCahyani PrastutiAinda não há avaliações

- GAAP AccountingDocumento88 páginasGAAP AccountingArshit Mahajan100% (1)

- Accounting TermsDocumento5 páginasAccounting Termsalostguy1Ainda não há avaliações

- House Hearing, 112TH Congress - Oversight of The Federal Deposit Insurance Corporation's Structured Transaction ProgramDocumento260 páginasHouse Hearing, 112TH Congress - Oversight of The Federal Deposit Insurance Corporation's Structured Transaction ProgramScribd Government DocsAinda não há avaliações

- 4 Audit CycleDocumento30 páginas4 Audit CycleZindgiKiKhatirAinda não há avaliações

- Florida Real Estate ONLY Power of Attorney FormDocumento2 páginasFlorida Real Estate ONLY Power of Attorney FormjayAinda não há avaliações

- Investements AccountingDocumento9 páginasInvestements AccountingShiyas FazalAinda não há avaliações

- Grade 11 Accounting Exam BreakdownDocumento9 páginasGrade 11 Accounting Exam BreakdownAli SiddiquiAinda não há avaliações

- A Private Investor's Guide To GiltsDocumento36 páginasA Private Investor's Guide To GiltsFuzzy_Wood_PersonAinda não há avaliações

- International Tax: India Highlights 2019Documento8 páginasInternational Tax: India Highlights 2019AbcdAinda não há avaliações

- Itemized Deductions - Taxes Paid 2021Documento2 páginasItemized Deductions - Taxes Paid 2021Finn KevinAinda não há avaliações

- Accounting Entries For Remittances: DR Confirmation CR ReceivablesDocumento1 páginaAccounting Entries For Remittances: DR Confirmation CR Receivablest.hemant2007Ainda não há avaliações

- Banking Working Capital & Term Loan Water Case StudyDocumento2 páginasBanking Working Capital & Term Loan Water Case Studyanon_652192649Ainda não há avaliações

- Double Entry Book Keeping SystemDocumento14 páginasDouble Entry Book Keeping SystemVisakh Vignesh100% (1)

- Declaration of Abandonment of Declared Homestead: Recording Requested By: and When Recorded, Mail ToDocumento1 páginaDeclaration of Abandonment of Declared Homestead: Recording Requested By: and When Recorded, Mail TohramcorpAinda não há avaliações

- Green Book Complete ,,,,,, GREEN BOOKDocumento153 páginasGreen Book Complete ,,,,,, GREEN BOOKSaguay MarcosAinda não há avaliações

- Tally Accounting Package Shortcut KeysDocumento40 páginasTally Accounting Package Shortcut KeysRaja Vishnudas100% (1)

- Bankruptcy - Louisiana TIPS SpeechDocumento68 páginasBankruptcy - Louisiana TIPS SpeechRicharnellia-RichieRichBattiest-CollinsAinda não há avaliações

- Handbook 5.12 Federal Tax Liens HandbookDocumento41 páginasHandbook 5.12 Federal Tax Liens HandbookPaulStaplesAinda não há avaliações

- Accounting BasicsDocumento42 páginasAccounting Basicssowmithra4uAinda não há avaliações

- Generally Accepted Auditing Standards A Complete Guide - 2020 EditionNo EverandGenerally Accepted Auditing Standards A Complete Guide - 2020 EditionAinda não há avaliações

- Electronic funds transfer A Clear and Concise ReferenceNo EverandElectronic funds transfer A Clear and Concise ReferenceAinda não há avaliações

- You Are My Servant and I Have Chosen You: What It Means to Be Called, Chosen, Prepared and Ordained by God for MinistryNo EverandYou Are My Servant and I Have Chosen You: What It Means to Be Called, Chosen, Prepared and Ordained by God for MinistryAinda não há avaliações

- Rina Mocha Kam NG Alas To TramDocumento2 páginasRina Mocha Kam NG Alas To TramParth UpadhyayAinda não há avaliações

- Credit Risk Estimation TechniquesDocumento31 páginasCredit Risk Estimation TechniquesHanumantha Rao Turlapati0% (1)

- Chapter 5 Depreciation Accounting PDFDocumento42 páginasChapter 5 Depreciation Accounting PDFravibhartia197888% (8)

- NewjobDocumento35 páginasNewjobParth UpadhyayAinda não há avaliações

- Tarpana SanskritDocumento9 páginasTarpana SanskritnavinnaithaniAinda não há avaliações

- 12thFYP ObjectivesDocumento3 páginas12thFYP ObjectivesParth UpadhyayAinda não há avaliações

- Current Affairs of Feb16Documento12 páginasCurrent Affairs of Feb16Parth UpadhyayAinda não há avaliações

- Bhairava Homam Sanskrit PDFDocumento36 páginasBhairava Homam Sanskrit PDFshalumutha3Ainda não há avaliações

- 2016 Books AuthorsDocumento2 páginas2016 Books AuthorsParth UpadhyayAinda não há avaliações

- Fiscal Policy 2015Documento11 páginasFiscal Policy 2015Parth UpadhyayAinda não há avaliações

- Appointments 2016Documento4 páginasAppointments 2016Parth UpadhyayAinda não há avaliações

- Current Affairs Pocket PDF - January 2016 by AffairsCloud - FinalDocumento25 páginasCurrent Affairs Pocket PDF - January 2016 by AffairsCloud - FinalRAGHUBALAN DURAIRAJUAinda não há avaliações

- Current Affairs FebruaryDocumento29 páginasCurrent Affairs FebruaryParth UpadhyayAinda não há avaliações

- Basic Uses of The English Tenses PDFDocumento4 páginasBasic Uses of The English Tenses PDFSreeAinda não há avaliações

- Week 10 Current Affairs 2016 PDFDocumento16 páginasWeek 10 Current Affairs 2016 PDFParth UpadhyayAinda não há avaliações

- Week 41 - 4 Oct-10 OctDocumento15 páginasWeek 41 - 4 Oct-10 OctParth UpadhyayAinda não há avaliações

- Current Affairs Pocket PDF - December 2015 by AffairsCloudDocumento22 páginasCurrent Affairs Pocket PDF - December 2015 by AffairsCloudRakesh RanjanAinda não há avaliações

- Current Affairs - 5 WeekDocumento16 páginasCurrent Affairs - 5 WeekParth UpadhyayAinda não há avaliações

- Current Affairs - Week 36 BankingDocumento10 páginasCurrent Affairs - Week 36 BankingParth UpadhyayAinda não há avaliações

- Fab Current Affair 2016Documento25 páginasFab Current Affair 2016Parth UpadhyayAinda não há avaliações

- Current Affairs - Week 35 Banking: Bandhan BankDocumento12 páginasCurrent Affairs - Week 35 Banking: Bandhan BankParth UpadhyayAinda não há avaliações

- Week SeptDocumento16 páginasWeek SeptParth UpadhyayAinda não há avaliações

- Week 41 - 4 Oct-10 OctDocumento15 páginasWeek 41 - 4 Oct-10 OctParth UpadhyayAinda não há avaliações

- Week 40 - 27 Sep - 3 OctDocumento12 páginasWeek 40 - 27 Sep - 3 OctParth UpadhyayAinda não há avaliações

- Week 4 GKDocumento9 páginasWeek 4 GKParth UpadhyayAinda não há avaliações

- Nov GKDocumento16 páginasNov GKParth UpadhyayAinda não há avaliações

- Current Affairs - Week 51Documento22 páginasCurrent Affairs - Week 51Parth UpadhyayAinda não há avaliações

- Week 43-11 Oct - 25 Oct Weekly PDFDocumento46 páginasWeek 43-11 Oct - 25 Oct Weekly PDFParth UpadhyayAinda não há avaliações

- Presentation On Liabilities Under Securities Law 28.11.2011Documento51 páginasPresentation On Liabilities Under Securities Law 28.11.2011Vidya AdsuleAinda não há avaliações

- Changing Work Culture in Indian Banking SectorDocumento16 páginasChanging Work Culture in Indian Banking SectorrupinderkangAinda não há avaliações

- Business Line - Columns - Thomas K Thomas - Telenor Exploring Strategic Alliance With Tata TeleservicesDocumento2 páginasBusiness Line - Columns - Thomas K Thomas - Telenor Exploring Strategic Alliance With Tata TeleservicesNadeem BadarAinda não há avaliações

- Money and BankingDocumento57 páginasMoney and BankingMohammed RaihanAinda não há avaliações

- China Pakistan Economic Corridor (CPEC) and Small Medium Enterprises (SMEs) of PakistanDocumento12 páginasChina Pakistan Economic Corridor (CPEC) and Small Medium Enterprises (SMEs) of PakistanTayyaub khalidAinda não há avaliações

- Mutual FundsDocumento36 páginasMutual FundsRavindra BabuAinda não há avaliações

- MemoDocumento3 páginasMemopeppermintlatteAinda não há avaliações

- F6uk 2010 Dec Q PDFDocumento10 páginasF6uk 2010 Dec Q PDFInsia AhmedAinda não há avaliações

- RRE FA - Interview With Lecturers & StudentsDocumento2 páginasRRE FA - Interview With Lecturers & StudentsSaifullizan Abd JamilAinda não há avaliações

- Strong Vs Repide Case DigestDocumento3 páginasStrong Vs Repide Case DigestHariette Kim TiongsonAinda não há avaliações

- Smart FinancialsDocumento49 páginasSmart FinancialsDebasmita NandyAinda não há avaliações

- Srilanka Position PaperDocumento6 páginasSrilanka Position PaperSibiya Zaman AdibaAinda não há avaliações

- Cmt3 QuestionsDocumento41 páginasCmt3 QuestionsUpdatest news0% (2)

- Borrowing Costs CVDocumento34 páginasBorrowing Costs CVRigine Pobe Morgadez100% (1)

- Business Environment and Policy: Dr. V L Rao Professor Dr. Radha Raghuramapatruni Assistant ProfessorDocumento41 páginasBusiness Environment and Policy: Dr. V L Rao Professor Dr. Radha Raghuramapatruni Assistant ProfessorRajeshwari RosyAinda não há avaliações

- Salem Abraham - Bloomberg Markets Mag Article - Mar09Documento8 páginasSalem Abraham - Bloomberg Markets Mag Article - Mar09jk_rentzkeAinda não há avaliações

- Project Report On Indian Capital Market and Trading TechniquesDocumento52 páginasProject Report On Indian Capital Market and Trading TechniquesViplav Ambastha0% (2)

- As Level Accounting Topic 1 OddDocumento45 páginasAs Level Accounting Topic 1 OddShoaib AslamAinda não há avaliações

- Regional Rural Banks Previous Papers - Gurgaon Gramin BankDocumento35 páginasRegional Rural Banks Previous Papers - Gurgaon Gramin BankShiv Ram Krishna100% (2)

- Diversification Strategy KennyDocumento5 páginasDiversification Strategy KennyThanh Tu NguyenAinda não há avaliações

- 0 - Project 1 FINAL PDFDocumento53 páginas0 - Project 1 FINAL PDFShree ShaAinda não há avaliações

- Role of Fdi in Banking Sector Towards Stimulating Green BankingDocumento12 páginasRole of Fdi in Banking Sector Towards Stimulating Green Bankingapi-33150260Ainda não há avaliações

- ABD MCQsDocumento40 páginasABD MCQsShruti NaikAinda não há avaliações

- When To Use The Momentum Entry TechniqueDocumento4 páginasWhen To Use The Momentum Entry Techniqueartus14Ainda não há avaliações

- Easyjet - 3-Statement Case StudyDocumento10 páginasEasyjet - 3-Statement Case StudykautiAinda não há avaliações