Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- HZB-15S Service ManualDocumento20 páginasHZB-15S Service ManualJason Cravy100% (1)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Civil-Engineering-Final-Year-Project-Quarry Dust As A Substitute of River Sand in Concrete Mixes PDFDocumento75 páginasCivil-Engineering-Final-Year-Project-Quarry Dust As A Substitute of River Sand in Concrete Mixes PDFVEERKUMAR GNDEC100% (1)

- FY 18-19 Budget School Aid RunsDocumento15 páginasFY 18-19 Budget School Aid RunsMatthew HamiltonAinda não há avaliações

- 2018-19 Executive Budget Briefing BookDocumento161 páginas2018-19 Executive Budget Briefing BookMatthew Hamilton100% (1)

- 2018 State of The State BookDocumento374 páginas2018 State of The State BookMatthew HamiltonAinda não há avaliações

- DiNapoli Debt Impact Study 2017Documento30 páginasDiNapoli Debt Impact Study 2017Matthew HamiltonAinda não há avaliações

- New York State Plastic Bag Task Force ReportDocumento88 páginasNew York State Plastic Bag Task Force ReportMatthew Hamilton100% (1)

- 11-27-17 LetterDocumento5 páginas11-27-17 LetterNick ReismanAinda não há avaliações

- SNY0118 Crosstabs011518Documento3 páginasSNY0118 Crosstabs011518Matthew HamiltonAinda não há avaliações

- Joint Budget Schedule 2018 Release FINALDocumento1 páginaJoint Budget Schedule 2018 Release FINALMatthew HamiltonAinda não há avaliações

- SNY0118 Crosstabs011618Documento7 páginasSNY0118 Crosstabs011618Nick ReismanAinda não há avaliações

- IDC Leader Jeff Klein Legal Memo Re: Sexual Harassment Allegation.Documento3 páginasIDC Leader Jeff Klein Legal Memo Re: Sexual Harassment Allegation.liz_benjamin6490Ainda não há avaliações

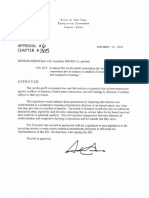

- Approval #64-66 of 2017Documento3 páginasApproval #64-66 of 2017Matthew HamiltonAinda não há avaliações

- State of The State BingoDocumento5 páginasState of The State BingoMatthew Hamilton100% (1)

- 11-29-17 Heastie Letter To McLaughlin Re: McLaughlin InvestigationDocumento2 páginas11-29-17 Heastie Letter To McLaughlin Re: McLaughlin InvestigationMatthew HamiltonAinda não há avaliações

- 6-21-17 Ethics Committee Letter To Heastie Re: McLaughlin InvestigationDocumento3 páginas6-21-17 Ethics Committee Letter To Heastie Re: McLaughlin InvestigationMatthew HamiltonAinda não há avaliações

- SNY1017 CrosstabsDocumento6 páginasSNY1017 CrosstabsNick ReismanAinda não há avaliações

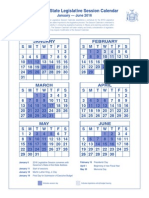

- 2016 Legislative Session CalendarDocumento1 página2016 Legislative Session CalendarMatthew HamiltonAinda não há avaliações

- Comptroller's Fiscal Update: State Fiscal Year 2017-18 Receipts and Disbursements Through The Mid-YearDocumento10 páginasComptroller's Fiscal Update: State Fiscal Year 2017-18 Receipts and Disbursements Through The Mid-YearMatthew HamiltonAinda não há avaliações

- 6-22-17 Heastie Letter To Ethics Committee Re: McLaughlin InvestigationDocumento1 página6-22-17 Heastie Letter To Ethics Committee Re: McLaughlin InvestigationMatthew HamiltonAinda não há avaliações

- DiNapoli Wall Street Profits Report 2017Documento8 páginasDiNapoli Wall Street Profits Report 2017Matthew HamiltonAinda não há avaliações

- OSC Municipal Water Systems ReportDocumento14 páginasOSC Municipal Water Systems ReportMatthew HamiltonAinda não há avaliações

- DiNapoli Federal Budget ReportDocumento36 páginasDiNapoli Federal Budget ReportMatthew HamiltonAinda não há avaliações

- Andrew Cuomo Letter To Jeff Bezos Re HQ2Documento2 páginasAndrew Cuomo Letter To Jeff Bezos Re HQ2Matthew HamiltonAinda não há avaliações

- Faso Scaffold Law BillDocumento4 páginasFaso Scaffold Law BillMatthew HamiltonAinda não há avaliações

- USA V Pigeon 100617Documento29 páginasUSA V Pigeon 100617Matthew HamiltonAinda não há avaliações

- Rockefeller Instittue 106 Ideas For A Constitutional ConventionDocumento17 páginasRockefeller Instittue 106 Ideas For A Constitutional ConventionMatthew HamiltonAinda não há avaliações

- Gov. Andrew Cuomo Law Approval Message #6 - 2017Documento1 páginaGov. Andrew Cuomo Law Approval Message #6 - 2017Matthew HamiltonAinda não há avaliações

- Siena College October 2017 PollDocumento8 páginasSiena College October 2017 PollMatthew HamiltonAinda não há avaliações

- USA v. Skelos Appellate DecisionDocumento12 páginasUSA v. Skelos Appellate DecisionMatthew HamiltonAinda não há avaliações

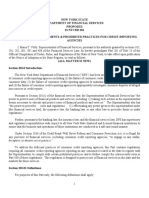

- NYS DFS Credit Reporting Agency RegulationsDocumento6 páginasNYS DFS Credit Reporting Agency RegulationsMatthew HamiltonAinda não há avaliações

- Gov. Andrew Immigration Status Executive OrderDocumento2 páginasGov. Andrew Immigration Status Executive OrderMatthew HamiltonAinda não há avaliações

- Book 1Documento100 páginasBook 1Devasyruc100% (1)

- Fuel Cell HandbookDocumento352 páginasFuel Cell HandbookHamza SuljicAinda não há avaliações

- Rendemen Dan Skrining Fitokimia Pada Ekstrak DaunDocumento6 páginasRendemen Dan Skrining Fitokimia Pada Ekstrak DaunArdya YusidhaAinda não há avaliações

- AMGG-S - 1 - Environmental Safeguard Monitoring - 25.03.2021Documento48 páginasAMGG-S - 1 - Environmental Safeguard Monitoring - 25.03.2021Mahidul Islam RatulAinda não há avaliações

- KPI and Supplier Performance Scorecard ToolDocumento7 páginasKPI and Supplier Performance Scorecard ToolJayant Kumar JhaAinda não há avaliações

- ESP Guidance For All Ships V13.7Documento53 páginasESP Guidance For All Ships V13.7Jayasankar GopalakrishnanAinda não há avaliações

- START-HERE Ch11 LectureDocumento84 páginasSTART-HERE Ch11 LecturePraveen VootlaAinda não há avaliações

- Common Safety Method GuidanceDocumento66 páginasCommon Safety Method GuidanceDiego UngerAinda não há avaliações

- GP Series Portable Generator: Owner's ManualDocumento48 páginasGP Series Portable Generator: Owner's ManualWilliam Medina CondorAinda não há avaliações

- Discover the flavors of Southwestern Luzon and Bicol RegionDocumento5 páginasDiscover the flavors of Southwestern Luzon and Bicol RegionGraceCayabyabNiduazaAinda não há avaliações

- Fermenting For Health - Pip MagazineDocumento2 páginasFermenting For Health - Pip MagazinePip MagazineAinda não há avaliações

- Cobb 500 PDFDocumento14 páginasCobb 500 PDFNeil Ryan100% (1)

- Work, Energy Power RevDocumento31 páginasWork, Energy Power RevRency Micaella CristobalAinda não há avaliações

- Case Digest 16Documento2 páginasCase Digest 16Mavic MoralesAinda não há avaliações

- A Text Book On Nursing Management AccordDocumento790 páginasA Text Book On Nursing Management AccordMohammed AfzalAinda não há avaliações

- 'S Outfits and Emergency Escape Breathing Devices (Eebd)Documento11 páginas'S Outfits and Emergency Escape Breathing Devices (Eebd)Thurdsuk NoinijAinda não há avaliações

- ZV Class Links @Medliferesuscitation-CopyDocumento31 páginasZV Class Links @Medliferesuscitation-CopyDebajyoti DasAinda não há avaliações

- Seizure Acute ManagementDocumento29 páginasSeizure Acute ManagementFridayana SekaiAinda não há avaliações

- Introduction To Iron Metallurgy PDFDocumento90 páginasIntroduction To Iron Metallurgy PDFDrTrinath TalapaneniAinda não há avaliações

- Amnesia With Focus On Post Traumatic AmnesiaDocumento27 páginasAmnesia With Focus On Post Traumatic AmnesiaWilliam ClemmonsAinda não há avaliações

- Transpo Printable Lecture4Documento10 páginasTranspo Printable Lecture4Jabin Sta. TeresaAinda não há avaliações

- Statistics of Design Error in The Process IndustriesDocumento13 páginasStatistics of Design Error in The Process IndustriesEmmanuel Osorno CaroAinda não há avaliações

- Fuel System D28Documento4 páginasFuel System D28Ian MuhammadAinda não há avaliações

- Gas Booster Systems Brochure r7Documento12 páginasGas Booster Systems Brochure r7ridwansaungnage_5580Ainda não há avaliações

- 2013 - Sara E. TraceDocumento35 páginas2013 - Sara E. TraceDewi WulandariAinda não há avaliações

- Chemistry Tshirt ProjectDocumento7 páginasChemistry Tshirt Projectapi-524483093Ainda não há avaliações

- SIDCSDocumento8 páginasSIDCSsakshi suranaAinda não há avaliações

- Neet Structural Organisation in Animals Important QuestionsDocumento18 páginasNeet Structural Organisation in Animals Important QuestionsARKA NEET BIOLOGYAinda não há avaliações