Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Food For ThoughtDocumento12 páginasFood For ThoughtcomputeraidAinda não há avaliações

- Financial Statements and Financial AnalysisDocumento17 páginasFinancial Statements and Financial AnalysisVaibhav MahajanAinda não há avaliações

- Chapter 12 Forecasting and Short - Term Financial PlanningDocumento33 páginasChapter 12 Forecasting and Short - Term Financial PlanningherrajohnAinda não há avaliações

- Cfap 1 Aafr PKDocumento336 páginasCfap 1 Aafr PKArslan Shafique Ch100% (1)

- Apples and OrangesDocumento12 páginasApples and OrangesKate GouldAinda não há avaliações

- ACCA exam key IAS/IFRS provisions Dec 2014 & Jun 2015Documento12 páginasACCA exam key IAS/IFRS provisions Dec 2014 & Jun 2015computeraidAinda não há avaliações

- ISA 230 Audit DocumentationDocumento10 páginasISA 230 Audit DocumentationCA Amit Kumar AfridiAinda não há avaliações

- Level 6 The MoonstoneDocumento58 páginasLevel 6 The Moonstonecomputeraid100% (1)

- ResumeDocumento42 páginasResumeMagdyAinda não há avaliações

- F8 Workbook Questions & Solutions 1.1 PDFDocumento182 páginasF8 Workbook Questions & Solutions 1.1 PDFViembre Tr33% (3)

- Cash Flow Without T AccountsDocumento4 páginasCash Flow Without T AccountscomputeraidAinda não há avaliações

- F8 - Audit ProcedureDocumento7 páginasF8 - Audit Procedurecomputeraid100% (2)

- Audit of Bank and CashDocumento4 páginasAudit of Bank and CashIftekhar IfteAinda não há avaliações

- Obtain Sufficient Appropriate Audit EvidenceDocumento10 páginasObtain Sufficient Appropriate Audit EvidencecomputeraidAinda não há avaliações

- ISA 230 Audit DocumentationDocumento10 páginasISA 230 Audit DocumentationCA Amit Kumar AfridiAinda não há avaliações

- Mighty DuckDocumento4 páginasMighty DuckcomputeraidAinda não há avaliações

- Guide To Understanding Financial Statements PDFDocumento96 páginasGuide To Understanding Financial Statements PDFyarokAinda não há avaliações

- Recruitment - Pack (1) - Nothinghill HousingDocumento15 páginasRecruitment - Pack (1) - Nothinghill HousingcomputeraidAinda não há avaliações

- Mighty DuckDocumento4 páginasMighty DuckcomputeraidAinda não há avaliações

- F8 Workbook Questions & Solutions 1.1 PDFDocumento182 páginasF8 Workbook Questions & Solutions 1.1 PDFViembre Tr33% (3)

- F8 Workbook Questions & Solutions 1.1 PDFDocumento182 páginasF8 Workbook Questions & Solutions 1.1 PDFViembre Tr33% (3)

- Review of Public Benefit SorpsDocumento45 páginasReview of Public Benefit SorpscomputeraidAinda não há avaliações

- Guide To Understanding Financial Statements PDFDocumento96 páginasGuide To Understanding Financial Statements PDFyarokAinda não há avaliações

- Review of Public Benefit SorpsDocumento45 páginasReview of Public Benefit SorpscomputeraidAinda não há avaliações

- F8 Workbook Questions & Solutions 1.1 PDFDocumento182 páginasF8 Workbook Questions & Solutions 1.1 PDFViembre Tr33% (3)

- Review of Public Benefit SorpsDocumento45 páginasReview of Public Benefit SorpscomputeraidAinda não há avaliações

- Review of Public Benefit SorpsDocumento45 páginasReview of Public Benefit SorpscomputeraidAinda não há avaliações

- Amalgamation of Partnership FirmDocumento14 páginasAmalgamation of Partnership FirmCopycat100% (1)

- Chapter 6 Accounting Information SystemDocumento11 páginasChapter 6 Accounting Information SystemRica de guzmanAinda não há avaliações

- RetailDocumento19 páginasRetailarathi_bhatAinda não há avaliações

- Profitability: The Star Logo, and South-Western Are Trademarks Used Herein Under LicenseDocumento19 páginasProfitability: The Star Logo, and South-Western Are Trademarks Used Herein Under LicensesoniaAinda não há avaliações

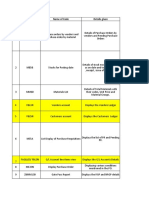

- S No. T Code Name of Code Details GivenDocumento17 páginasS No. T Code Name of Code Details GivenPravesh PangeniAinda não há avaliações

- Ajanta Pharma LTD.: Net Fixed AssetsDocumento4 páginasAjanta Pharma LTD.: Net Fixed AssetsDeepak DashAinda não há avaliações

- Reaction Paper Estate Tax Valencia, Reginald GDocumento2 páginasReaction Paper Estate Tax Valencia, Reginald GReginald ValenciaAinda não há avaliações

- Partnership AppDocumento22 páginasPartnership AppPeter AkramAinda não há avaliações

- Name of Company Worksheet for the period endedDocumento11 páginasName of Company Worksheet for the period endedRaymond RocoAinda não há avaliações

- Luxasia Pte. Ltd. and Its Subsidiaries Directors' Statement and Financial Statements Year Ended December 31, 2018Documento73 páginasLuxasia Pte. Ltd. and Its Subsidiaries Directors' Statement and Financial Statements Year Ended December 31, 2018Joyce ChongAinda não há avaliações

- Solution Manual For Financial Accounting 10th Edition by HarrisonDocumento55 páginasSolution Manual For Financial Accounting 10th Edition by HarrisonAdo BerikelashviliAinda não há avaliações

- Strategy Management and Financial Analysis of HULDocumento7 páginasStrategy Management and Financial Analysis of HULAAYUSH SHARMA 1927501Ainda não há avaliações

- PresentationDocumento12 páginasPresentationJoachim Dip GomesAinda não há avaliações

- IFRS 9 Financial Instruments - F7Documento39 páginasIFRS 9 Financial Instruments - F7TD2 from Henry HarvinAinda não há avaliações

- Authorisation Object ListDocumento70 páginasAuthorisation Object Listsamirjoshi73Ainda não há avaliações

- Financial Statements Analysis GuideDocumento14 páginasFinancial Statements Analysis GuideCommunity Institute of Management StudiesAinda não há avaliações

- KTQTE2Documento172 páginasKTQTE2Ly Võ KhánhAinda não há avaliações

- Cash Flow SumDocumento5 páginasCash Flow Sumbalaje99 kAinda não há avaliações

- LAS-11-BESR-Q4-Las 5-6Documento4 páginasLAS-11-BESR-Q4-Las 5-6Mary Bernadette SandigAinda não há avaliações

- Chapter 4: Provision (Contingent Liability)Documento2 páginasChapter 4: Provision (Contingent Liability)Jen Bernadette CiegoAinda não há avaliações

- Initial Measurement at Cost.: Property, Plant and EquipmentDocumento5 páginasInitial Measurement at Cost.: Property, Plant and EquipmentCarms St ClaireAinda não há avaliações

- Due Dilegence ReportDocumento6 páginasDue Dilegence ReportIML2016Ainda não há avaliações

- Advanced Accounts EXAM J21Documento26 páginasAdvanced Accounts EXAM J21Harshwardhan PatilAinda não há avaliações

- Role of Human Resource Accounting in TheDocumento9 páginasRole of Human Resource Accounting in TheApurva SharmaAinda não há avaliações

- Financial Model of Infosys: Revenue Ebitda Net IncomeDocumento32 páginasFinancial Model of Infosys: Revenue Ebitda Net IncomePrabhdeep Dadyal100% (1)

- Smeda Oil Distillaiton UnitDocumento21 páginasSmeda Oil Distillaiton UnitHaseeb A ChaudhryAinda não há avaliações