Você também pode gostar

- Affidavit of No RentalDocumento2 páginasAffidavit of No RentalMalen Roque Saludes75% (12)

- CIR v. Isabela Cultural Corp.Documento4 páginasCIR v. Isabela Cultural Corp.kathrynmaydevezaAinda não há avaliações

- Mushak-9.1 VAT Return On 19.NOV.2020 PDFDocumento6 páginasMushak-9.1 VAT Return On 19.NOV.2020 PDFApexBD01Ainda não há avaliações

- Cir v. Cta and Petron CorporationDocumento2 páginasCir v. Cta and Petron CorporationLara YuloAinda não há avaliações

- Ruling - CIR V FilinvestDocumento1 páginaRuling - CIR V FilinvestryanmeinAinda não há avaliações

- CIR Vs de La SalleDocumento2 páginasCIR Vs de La SalleOlenFuerte100% (6)

- (SPIT) (CIR v. Benguet Corp.)Documento3 páginas(SPIT) (CIR v. Benguet Corp.)Matthew JohnsonAinda não há avaliações

- CIR vs. Raul Gonzales (Digest)Documento2 páginasCIR vs. Raul Gonzales (Digest)Bam Bathan100% (1)

- CIR vs. Pilipinas ShellDocumento3 páginasCIR vs. Pilipinas ShellArchie Torres88% (8)

- 17 CIR v. Tours SpecialistsDocumento3 páginas17 CIR v. Tours SpecialistsChedeng KumaAinda não há avaliações

- 3 Division: Taxation I Case Digest CompilationDocumento2 páginas3 Division: Taxation I Case Digest CompilationPraisah Marjorey Picot0% (1)

- Sworn Affidavit (Solo Parent) BlankDocumento1 páginaSworn Affidavit (Solo Parent) BlankAn Dinaga100% (4)

- Affidavit of Loss - Sim Card For GcashDocumento2 páginasAffidavit of Loss - Sim Card For GcashKayelyn LatAinda não há avaliações

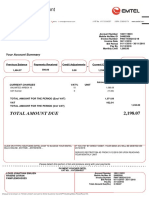

- Statement of Account VAT Invoice: Total Amount DueDocumento1 páginaStatement of Account VAT Invoice: Total Amount DueJonathan EmilienAinda não há avaliações

- Forms of escape from taxation through VAT exemptionsDocumento3 páginasForms of escape from taxation through VAT exemptionsKath Leen100% (1)

- 26 Contex Vs CIRDocumento2 páginas26 Contex Vs CIRIvan Romeo100% (1)

- (SPIT) (Contex Corp. v. CIR) (Francisco)Documento3 páginas(SPIT) (Contex Corp. v. CIR) (Francisco)gundam_rose_01100% (4)

- Medicard Phil Inc. vs. CIRDocumento2 páginasMedicard Phil Inc. vs. CIRhigoremso giensdksAinda não há avaliações

- Cir v. MeralcoDocumento2 páginasCir v. MeralcoKhaiye De Asis AggabaoAinda não há avaliações

- Exclusions from gross income; compensation incomeDocumento2 páginasExclusions from gross income; compensation incomeHomer SimpsonAinda não há avaliações

- Visayan Cebu Terminal Vs CirDocumento2 páginasVisayan Cebu Terminal Vs CirylaineAinda não há avaliações

- Contex Corp vs CIRDocumento2 páginasContex Corp vs CIRAudrey Deguzman67% (3)

- Bpi vs. Cir, GR No. 139736Documento11 páginasBpi vs. Cir, GR No. 139736Ronz RoganAinda não há avaliações

- CIR V BurmeisterDocumento1 páginaCIR V BurmeisterMark Wong delos ReyesAinda não há avaliações

- CIR vs Magsaysay Lines on VAT on sale of vesselsDocumento2 páginasCIR vs Magsaysay Lines on VAT on sale of vesselsmisscyu100% (1)

- CIR v. Fitness by DesignDocumento4 páginasCIR v. Fitness by DesignJesi CarlosAinda não há avaliações

- CIR Vs Bank of CommerceDocumento2 páginasCIR Vs Bank of CommerceAster Beane AranetaAinda não há avaliações

- CIR V Pilipinas ShellDocumento4 páginasCIR V Pilipinas ShellCedric Enriquez100% (2)

- Angeles City v. Angeles Electric CorporationDocumento4 páginasAngeles City v. Angeles Electric CorporationOmsimAinda não há avaliações

- City of Iriga vs. CamSurDocumento1 páginaCity of Iriga vs. CamSurxx_stripped52Ainda não há avaliações

- CIR vs. Asalus - DigestDocumento2 páginasCIR vs. Asalus - DigestGrandeureign Ortizo100% (3)

- RHOMBUS Vs CIRDocumento3 páginasRHOMBUS Vs CIRMarife MinorAinda não há avaliações

- ANPC v. BIR rules membership fees non-taxableDocumento2 páginasANPC v. BIR rules membership fees non-taxableDerek C. Egalla100% (2)

- Court Rules Tax Court Had Jurisdiction in Estate Tax CaseDocumento9 páginasCourt Rules Tax Court Had Jurisdiction in Estate Tax CaseKevin MatibagAinda não há avaliações

- CIR V StanleyDocumento15 páginasCIR V StanleyPatatas SayoteAinda não há avaliações

- CIR V Fitness by DesignDocumento3 páginasCIR V Fitness by Designsmtm06100% (3)

- Gibbs vs. CIR and CTA rules on prescription of tax claimsDocumento2 páginasGibbs vs. CIR and CTA rules on prescription of tax claimsIrish Asilo PinedaAinda não há avaliações

- CM Hoskins V CIRDocumento3 páginasCM Hoskins V CIRPaula Villarin100% (1)

- SYSTRA PHILIPPINES vs. CIR tax credit carryover rulingDocumento2 páginasSYSTRA PHILIPPINES vs. CIR tax credit carryover rulingArmstrong BosantogAinda não há avaliações

- Diageo Philippines Lacks StandingDocumento1 páginaDiageo Philippines Lacks StandingArmstrong BosantogAinda não há avaliações

- CIR Vs Next MobileDocumento2 páginasCIR Vs Next Mobilegeorge almeda100% (1)

- CTA upholds prescription defense for STI tax assessmentsDocumento2 páginasCTA upholds prescription defense for STI tax assessmentsJoshua Erik Madria100% (1)

- CIR vs UCSFA-MPC VAT ExemptionDocumento2 páginasCIR vs UCSFA-MPC VAT ExemptionJeffrey Magada100% (2)

- Fort Bonifacio vs. CIRDocumento3 páginasFort Bonifacio vs. CIRDNAAAinda não há avaliações

- Fernandez vs. FernandezDocumento1 páginaFernandez vs. FernandezKitchie San PedroAinda não há avaliações

- TaxDocumento7 páginasTaxArvi April NarzabalAinda não há avaliações

- Cir v. GoodrichDocumento7 páginasCir v. GoodrichClaudine Ann ManaloAinda não há avaliações

- RCBC Vs CIR, GR No. 168498, April 24, 2007Documento1 páginaRCBC Vs CIR, GR No. 168498, April 24, 2007Vel June De LeonAinda não há avaliações

- Lascona Land Vs CIRDocumento2 páginasLascona Land Vs CIRJOHN SPARKSAinda não há avaliações

- Cir V Pascor RealtyDocumento3 páginasCir V Pascor RealtyCharmaine MejiaAinda não há avaliações

- 157 CIR V Meralco GAMDocumento2 páginas157 CIR V Meralco GAMGreghvon MatolAinda não há avaliações

- CIR v. Univation, GR 231581, 10 Apr 2019Documento4 páginasCIR v. Univation, GR 231581, 10 Apr 2019Dan Millado100% (2)

- Diageo Philippines, Inc. V. Commissioner of Internal RevenueDocumento2 páginasDiageo Philippines, Inc. V. Commissioner of Internal RevenueDrave Mont100% (1)

- San Juan v. CastroDocumento1 páginaSan Juan v. CastroJechel TanAinda não há avaliações

- Lascona Land Co., Inc. v. CIRDocumento2 páginasLascona Land Co., Inc. v. CIRAron Lobo100% (1)

- Fishwealth Canning v. CIRDocumento1 páginaFishwealth Canning v. CIRRia Kriselle Francia PabaleAinda não há avaliações

- Philippine Airlines V CIRDocumento5 páginasPhilippine Airlines V CIRBettina Rayos del SolAinda não há avaliações

- Estate Tax Assessment Notice DisputeDocumento1 páginaEstate Tax Assessment Notice DisputeRaquel Doquenia100% (1)

- Cir Vs United Salvage and Towage Case DigestDocumento1 páginaCir Vs United Salvage and Towage Case DigestjovifactorAinda não há avaliações

- Camp John Hay vs. CBAADocumento2 páginasCamp John Hay vs. CBAAGeorgina100% (1)

- Cir V CA ComasercoDocumento2 páginasCir V CA ComasercoJoel G. AyonAinda não há avaliações

- CIR vs. CTA and Smith Kline & French Overseas Co. (Philippine branch) deductibility of head office overhead expensesDocumento1 páginaCIR vs. CTA and Smith Kline & French Overseas Co. (Philippine branch) deductibility of head office overhead expensesscartoneros_1Ainda não há avaliações

- CIR Vs Stanley PHDocumento2 páginasCIR Vs Stanley PHAnneAinda não há avaliações

- Vat Case DigestsDocumento38 páginasVat Case DigestsWestleyAinda não há avaliações

- Contex Corporation vs. Commissioner of Internal Revenue DIGESTDocumento4 páginasContex Corporation vs. Commissioner of Internal Revenue DIGESTJohnRouenTorresMarzoAinda não há avaliações

- Signature PageDocumento1 páginaSignature PageKayelyn LatAinda não há avaliações

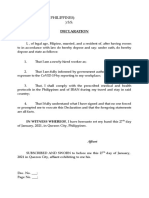

- DeclarationDocumento2 páginasDeclarationKayelyn LatAinda não há avaliações

- Deeco Paper Products Secretary's Certificate Appointing Robert DeeDocumento1 páginaDeeco Paper Products Secretary's Certificate Appointing Robert DeeMaria Lourdes SantiagoAinda não há avaliações

- Formal Entry of AppearanceDocumento1 páginaFormal Entry of AppearanceKayelyn LatAinda não há avaliações

- Memorandum of AgreementDocumento3 páginasMemorandum of AgreementKayelyn LatAinda não há avaliações

- Motion For Execution of JudgmentDocumento2 páginasMotion For Execution of JudgmentKayelyn LatAinda não há avaliações

- Affidavit of Self-Accident - 2Documento2 páginasAffidavit of Self-Accident - 2Kayelyn LatAinda não há avaliações

- Affidavit of Two Disinterested PersonsDocumento1 páginaAffidavit of Two Disinterested PersonsKayelyn LatAinda não há avaliações

- AcknowledgmentDocumento1 páginaAcknowledgmentKayelyn LatAinda não há avaliações

- Affidavit of DiscrepancyDocumento2 páginasAffidavit of DiscrepancyKayelyn LatAinda não há avaliações

- Affidavit of Loss: IN WITNESS WHEREOF, I Have Hereunto Set My Hand This - Day ofDocumento1 páginaAffidavit of Loss: IN WITNESS WHEREOF, I Have Hereunto Set My Hand This - Day ofKayelyn LatAinda não há avaliações

- Letter RequestDocumento1 páginaLetter RequestKayelyn LatAinda não há avaliações

- Petition For Renewal of NCDocumento3 páginasPetition For Renewal of NCKayelyn LatAinda não há avaliações

- Affidavit of Loss: IN WITNESS WHEREOF, I Have Hereunto Set My Hand This - Day ofDocumento1 páginaAffidavit of Loss: IN WITNESS WHEREOF, I Have Hereunto Set My Hand This - Day ofKayelyn LatAinda não há avaliações

- Affidavit of Closure: IN WITNESS WHEREOF, I Have Hereunto Set My Hand This - Day ofDocumento2 páginasAffidavit of Closure: IN WITNESS WHEREOF, I Have Hereunto Set My Hand This - Day ofKayelyn LatAinda não há avaliações

- Affidavit of Loss - Wallet and IDsDocumento2 páginasAffidavit of Loss - Wallet and IDsKayelyn LatAinda não há avaliações

- SPA - InsuranceDocumento1 páginaSPA - InsuranceKayelyn LatAinda não há avaliações

- Affidavit of Loss: IN WITNESS WHEREOF, I Have Hereunto Set My Hand This - Day ofDocumento2 páginasAffidavit of Loss: IN WITNESS WHEREOF, I Have Hereunto Set My Hand This - Day ofKayelyn LatAinda não há avaliações

- Urgent Motion To Reset Hearing: ReliefDocumento2 páginasUrgent Motion To Reset Hearing: ReliefKayelyn LatAinda não há avaliações

- Compromise Agreement: Witnesseth: WHEREAS, The Parties Herein Are The Litigants in The CriminalDocumento4 páginasCompromise Agreement: Witnesseth: WHEREAS, The Parties Herein Are The Litigants in The CriminalKayelyn LatAinda não há avaliações

- Affidavit of Desistance: IN WITNESS WHEREOF, I Have Hereunto Set My Hand ThisDocumento1 páginaAffidavit of Desistance: IN WITNESS WHEREOF, I Have Hereunto Set My Hand ThisKayelyn LatAinda não há avaliações

- Urgent Motion To Reset Hearing: ReliefDocumento2 páginasUrgent Motion To Reset Hearing: ReliefKayelyn LatAinda não há avaliações

- List of Occs and Bccs With Microsoft Office 365 Accounts As of May 15, 2020 Court/Station Account Type Email AddressDocumento53 páginasList of Occs and Bccs With Microsoft Office 365 Accounts As of May 15, 2020 Court/Station Account Type Email AddressJacci Rocha100% (1)

- Affidavit of Change of Body Type of MotorcycleDocumento2 páginasAffidavit of Change of Body Type of MotorcycleKayelyn LatAinda não há avaliações

- Special Power of Attorney: Certiorari, Prohibition, Mandamus, and The Power To Do The FollowingDocumento2 páginasSpecial Power of Attorney: Certiorari, Prohibition, Mandamus, and The Power To Do The FollowingKayelyn LatAinda não há avaliações

- Affidavit of DesistanceDocumento2 páginasAffidavit of DesistanceKayelyn LatAinda não há avaliações

- Special Power of Attorney: NOW LL EN Y Hese ResentsDocumento2 páginasSpecial Power of Attorney: NOW LL EN Y Hese ResentsKayelyn LatAinda não há avaliações

- 032 Portugal LPDocumento26 páginas032 Portugal LPyisaboc539Ainda não há avaliações

- En Bookcore Your-Booking Cb7d3krbg1 Print Lang enDocumento2 páginasEn Bookcore Your-Booking Cb7d3krbg1 Print Lang enneethu1995georgeAinda não há avaliações

- Jumbo East Realty v. CIR, CTA Case No. 8380, March 16, 2015Documento31 páginasJumbo East Realty v. CIR, CTA Case No. 8380, March 16, 2015SGAinda não há avaliações

- Erasmus+CBHE Final Reports Oct2022Documento59 páginasErasmus+CBHE Final Reports Oct2022Fouad MihoubAinda não há avaliações

- Building A Successful Construction Company - The Practical GuideDocumento504 páginasBuilding A Successful Construction Company - The Practical Guideengr_caesar5162100% (2)

- Release Notes BUSY 21Documento26 páginasRelease Notes BUSY 21Ppradip BbhandariAinda não há avaliações

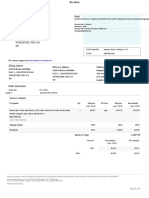

- Tax Invoice/Credit Note: Mobile Number Bill Issue Date Account ID Bill Period Bill NumberDocumento5 páginasTax Invoice/Credit Note: Mobile Number Bill Issue Date Account ID Bill Period Bill Numbern4hpx4cyjzAinda não há avaliações

- Tax Ii CasesDocumento4 páginasTax Ii CasesBae Irene100% (2)

- Kanakia AFS Tower A PDFDocumento79 páginasKanakia AFS Tower A PDFRohan BagadiyaAinda não há avaliações

- Drop Ileana Andreea Flat 1, 5 Droitwich Road Worcester, Wr3 7Lg GBDocumento1 páginaDrop Ileana Andreea Flat 1, 5 Droitwich Road Worcester, Wr3 7Lg GBIleana Andreea DropAinda não há avaliações

- Revenue Mobilization and Current Tax Issues: The Case of The PhilippinesDocumento22 páginasRevenue Mobilization and Current Tax Issues: The Case of The PhilippinesAdrian PanganibanAinda não há avaliações

- Justice Dimaampao Cases On VAT and RemediesDocumento87 páginasJustice Dimaampao Cases On VAT and Remediesching113Ainda não há avaliações

- Fsuipc4 User GuideDocumento59 páginasFsuipc4 User GuidemelihmiracAinda não há avaliações

- FNSBKG404 5Documento4 páginasFNSBKG404 5natty100% (1)

- RR 1-95Documento9 páginasRR 1-95matinikki0% (1)

- 1 - Lmi CHPDocumento162 páginas1 - Lmi CHPAnonymous 9kzuGaYAinda não há avaliações

- Kapatiran NG Mga Naglilingkod Sa Pamahalaan NG Pilipinas, Inc. vs. Tan, 163 SCRA 371 (1988)Documento16 páginasKapatiran NG Mga Naglilingkod Sa Pamahalaan NG Pilipinas, Inc. vs. Tan, 163 SCRA 371 (1988)Jillian BatacAinda não há avaliações

- Zara Terms and Conditions en ME 20220919Documento12 páginasZara Terms and Conditions en ME 20220919Таня ШикинаAinda não há avaliações

- F6zwe 2015 Dec ADocumento8 páginasF6zwe 2015 Dec APhebieon MukwenhaAinda não há avaliações

- Name of The Business-Rainbow Blooms LLC. Executive SummaryDocumento17 páginasName of The Business-Rainbow Blooms LLC. Executive SummaryAhamed AliAinda não há avaliações

- Bangalore Bail Case Final OrderDocumento19 páginasBangalore Bail Case Final OrderSURANA1973Ainda não há avaliações

- Tax - Case DigestsDocumento13 páginasTax - Case DigestsSkylee SoAinda não há avaliações

- BORJANDocumento8 páginasBORJANSana AmbreenAinda não há avaliações

- Tax Invoice Stripe FeesDocumento1 páginaTax Invoice Stripe FeesRafa CAinda não há avaliações

- Aerosus TrainingDocumento101 páginasAerosus TrainingMladen RadojevicAinda não há avaliações

- Foundations in Taxation FTX (UK) Jun-Dec 20 - FinalDocumento19 páginasFoundations in Taxation FTX (UK) Jun-Dec 20 - FinalBurhanMTHAinda não há avaliações

- Rajasthan MSME Policy 2015: PreambleDocumento17 páginasRajasthan MSME Policy 2015: PreambleAmitAinda não há avaliações

- All 59 E-Business Quizzes As On DateDocumento74 páginasAll 59 E-Business Quizzes As On Datepoojadixit1090Ainda não há avaliações