Você também pode gostar

- Lecture TortsDocumento91 páginasLecture TortsBrianCarpioAinda não há avaliações

- UCPB Gen Insurance v. TelamarkDocumento3 páginasUCPB Gen Insurance v. TelamarkJoseph DimalantaAinda não há avaliações

- Conflict of LawsDocumento29 páginasConflict of LawsCLOROUTHEANGAinda não há avaliações

- Insurance (Tickler)Documento20 páginasInsurance (Tickler)Romena LucianoAinda não há avaliações

- Insurance Case DigestsDocumento134 páginasInsurance Case DigestsgraceAinda não há avaliações

- INSURANCE FINALsDocumento4 páginasINSURANCE FINALsNonoy D VolosoAinda não há avaliações

- Insurance Notes (Dizon)Documento38 páginasInsurance Notes (Dizon)Gianna PeñalosaAinda não há avaliações

- Finals-Insurance Week 5Documento19 páginasFinals-Insurance Week 5Ryan ChristianAinda não há avaliações

- Murillo, Paul Arman Succession-Quiz-August-25-2020Documento2 páginasMurillo, Paul Arman Succession-Quiz-August-25-2020Paul Arman MurilloAinda não há avaliações

- Insurance ReviewerDocumento27 páginasInsurance ReviewerBoogie San JuanAinda não há avaliações

- Bar Questions For Agency Trust and PartnDocumento4 páginasBar Questions For Agency Trust and PartnSahira Macaombao IbrahimAinda não há avaliações

- Spec Pro Digested CasesDocumento4 páginasSpec Pro Digested CasesQuiny BelleAinda não há avaliações

- Zenith Insurance Corporation Vs CADocumento6 páginasZenith Insurance Corporation Vs CAOscar E Valero100% (1)

- Montances, Bryan Ian L. Torts Monday 530 To 730pm Atty HiguitDocumento1 páginaMontances, Bryan Ian L. Torts Monday 530 To 730pm Atty HiguitJewel MP DayoAinda não há avaliações

- Insurance - Atty QuimsonDocumento102 páginasInsurance - Atty QuimsonJoseph Plazo, Ph.DAinda não há avaliações

- Codal Provisions For Insurance (Philippines)Documento23 páginasCodal Provisions For Insurance (Philippines)Camille AngelicaAinda não há avaliações

- (OC) Sales Q & ADocumento12 páginas(OC) Sales Q & ADeej JayAinda não há avaliações

- Tax 1 Midterms ReviewerDocumento52 páginasTax 1 Midterms ReviewerJackie CanlasAinda não há avaliações

- Credit Transactions ReviewerDocumento7 páginasCredit Transactions ReviewerJohn Dx LapidAinda não há avaliações

- Insurable Interest HandoutDocumento27 páginasInsurable Interest HandoutDyrene Rosario UngsodAinda não há avaliações

- Insurance Law of The PhilippinesDocumento24 páginasInsurance Law of The PhilippinesTherese Diane SudarioAinda não há avaliações

- What Is A Corporation?Documento28 páginasWhat Is A Corporation?Mark Ervin Abancia100% (1)

- Torts and Damages Case DigestDocumento42 páginasTorts and Damages Case DigestAnthea Louise RosinoAinda não há avaliações

- Memory Aid - 06 Special ProceedingsDocumento86 páginasMemory Aid - 06 Special Proceedingsamazed07Ainda não há avaliações

- Outline: Conflict of Law in Torts and Crimes A. TortsDocumento7 páginasOutline: Conflict of Law in Torts and Crimes A. TortsWillam MontalbanAinda não há avaliações

- Insular Life v. EbradoDocumento3 páginasInsular Life v. EbradoFrancis PunoAinda não há avaliações

- Insurance Reviewer Atty GapuzDocumento6 páginasInsurance Reviewer Atty GapuzJohn Soap Reznov MacTavishAinda não há avaliações

- Insurance Question & AnswerDocumento11 páginasInsurance Question & AnswerVinz G. VizAinda não há avaliações

- C2020 Insurance Case Digest CompilationDocumento168 páginasC2020 Insurance Case Digest CompilationHazel Vianca OrtegaAinda não há avaliações

- 01 Transpo DigestsDocumento33 páginas01 Transpo DigestsNicolo GarciaAinda não há avaliações

- De Leon Insurance PointersDocumento9 páginasDe Leon Insurance PointersKarlo Gonzalo Guibone BatacAinda não há avaliações

- Insurance Case Digest: Heirs of Loreto C. Maramag V Maramag (2009)Documento16 páginasInsurance Case Digest: Heirs of Loreto C. Maramag V Maramag (2009)Francis MoraledaAinda não há avaliações

- Essentials of Insurance LawDocumento12 páginasEssentials of Insurance LawGerald KagaoanAinda não há avaliações

- Transportation Law CasesDocumento71 páginasTransportation Law CasesjayzeeAinda não há avaliações

- EGC Conflict of Laws Reviewer (COMPLETE)Documento72 páginasEGC Conflict of Laws Reviewer (COMPLETE)Ervin Gedmaire CaroAinda não há avaliações

- Ins Dec7Documento10 páginasIns Dec7Christine NarteaAinda não há avaliações

- Handout - Notice of LossDocumento3 páginasHandout - Notice of LossowenAinda não há avaliações

- Case DigestDocumento8 páginasCase DigestNurlailah AliAinda não há avaliações

- Aboitiz Shipping Corporation V Gaflac (1993)Documento2 páginasAboitiz Shipping Corporation V Gaflac (1993)Mary Grace CalaloAinda não há avaliações

- Insurance Case Digests Compendium PDFDocumento330 páginasInsurance Case Digests Compendium PDFKing100% (1)

- Shafer V JudgeDocumento2 páginasShafer V JudgeKenneth BuriAinda não há avaliações

- United States v. Richard J. Gordon, 655 F.2d 478, 2d Cir. (1981)Documento13 páginasUnited States v. Richard J. Gordon, 655 F.2d 478, 2d Cir. (1981)Scribd Government DocsAinda não há avaliações

- Outline of Philippine Insurance Code RA10607Documento9 páginasOutline of Philippine Insurance Code RA10607James CorroAinda não há avaliações

- Proof of Foreign Law and ExceptionsDocumento23 páginasProof of Foreign Law and ExceptionsJessa PuerinAinda não há avaliações

- Republic Act No. 10607 The Insurance Code: Business or Transacting An Insurance Business."Documento5 páginasRepublic Act No. 10607 The Insurance Code: Business or Transacting An Insurance Business."Czarina JaneAinda não há avaliações

- Petrophil Corp V CADocumento2 páginasPetrophil Corp V CAJerome AzarconAinda não há avaliações

- Manila Electric Vs YatcoDocumento6 páginasManila Electric Vs Yatcobraindead_91Ainda não há avaliações

- Cebu Salvage Corporation CaseDocumento1 páginaCebu Salvage Corporation CaseEim Balt MacmodAinda não há avaliações

- Insurance 2 - Ong - RCBC V CADocumento2 páginasInsurance 2 - Ong - RCBC V CADaniel OngAinda não há avaliações

- Malayan Insurance Co. Vs ArnaldoDocumento2 páginasMalayan Insurance Co. Vs ArnaldoRenz AmonAinda não há avaliações

- 89 Scra 543 356 Scra 307 GR No. 171379Documento3 páginas89 Scra 543 356 Scra 307 GR No. 171379Jester ConcepcionAinda não há avaliações

- 2011 NLRC Rules of ProcedureDocumento42 páginas2011 NLRC Rules of ProcedureAve ChaezaAinda não há avaliações

- Insurance Lecture Notes 1Documento5 páginasInsurance Lecture Notes 1Anthony Tamayosa Del AyreAinda não há avaliações

- Republic vs. Sunlife Assurance Company of Canada (GR No. 15805 OCTOBER 14, 2005)Documento9 páginasRepublic vs. Sunlife Assurance Company of Canada (GR No. 15805 OCTOBER 14, 2005)Don TiansayAinda não há avaliações

- Conflicts Review - Wills and SuccessionDocumento1 páginaConflicts Review - Wills and SuccessionEunice SerneoAinda não há avaliações

- Case Proceedings of Abdullahi vs. PfizerDocumento7 páginasCase Proceedings of Abdullahi vs. PfizerHazel OnahonAinda não há avaliações

- Sps. Cruz vs. Sun Holidays, Inc., G.R. No. 186312, June 29, 2010Documento1 páginaSps. Cruz vs. Sun Holidays, Inc., G.R. No. 186312, June 29, 2010MellyAinda não há avaliações

- INSURANCE Case DoctrinesDocumento5 páginasINSURANCE Case DoctrinesMikee Baliguat TanAinda não há avaliações

- Insurance Case 1 11 and 15Documento7 páginasInsurance Case 1 11 and 15Jeru SagaoinitAinda não há avaliações

- 2 - Formation of Insurance ContractDocumento21 páginas2 - Formation of Insurance Contractchong huisinAinda não há avaliações

- Bayanihan To Heal As One Enrolled Bill PDFDocumento8 páginasBayanihan To Heal As One Enrolled Bill PDFWorstWitch TalaAinda não há avaliações

- How To Deal With Border Issues: A Diplomat-Practitioner's PerspectiveDocumento12 páginasHow To Deal With Border Issues: A Diplomat-Practitioner's PerspectiveWorstWitch TalaAinda não há avaliações

- State Responsibility in Disputed Areas On Land and at SeaDocumento54 páginasState Responsibility in Disputed Areas On Land and at SeaWorstWitch TalaAinda não há avaliações

- Office of Legal Affairs Extremely Urgent Memorandum For The Assistant Secretary, UnioDocumento3 páginasOffice of Legal Affairs Extremely Urgent Memorandum For The Assistant Secretary, UnioWorstWitch TalaAinda não há avaliações

- Judge Hisashi Owada CVDocumento2 páginasJudge Hisashi Owada CVWorstWitch TalaAinda não há avaliações

- Construction Quality ManagementDocumento4 páginasConstruction Quality ManagementWorstWitch TalaAinda não há avaliações

- Assignment No. 1 - CM 654 FINALDocumento6 páginasAssignment No. 1 - CM 654 FINALWorstWitch TalaAinda não há avaliações

- Campa CaseDocumento15 páginasCampa CaseWorstWitch TalaAinda não há avaliações

- Contract of Security Services 2015 (Example)Documento14 páginasContract of Security Services 2015 (Example)WorstWitch Tala100% (1)

- Imperial vs. ArmesDocumento17 páginasImperial vs. ArmesWorstWitch TalaAinda não há avaliações

- Guillermo V Uson DigestDocumento2 páginasGuillermo V Uson DigestWorstWitch Tala100% (1)

- Imperial vs. ArmesDocumento17 páginasImperial vs. ArmesWorstWitch Tala0% (1)

- De Castro vs. CADocumento2 páginasDe Castro vs. CAWorstWitch Tala67% (3)

- Guillermo V Uson DigestDocumento2 páginasGuillermo V Uson DigestWorstWitch Tala100% (1)

- Bar Notes - Civil ProcedureDocumento12 páginasBar Notes - Civil ProcedureWorstWitch TalaAinda não há avaliações

- CMTA Disputing Assessment or ClassificationDocumento1 páginaCMTA Disputing Assessment or ClassificationWorstWitch TalaAinda não há avaliações

- UP Legal Ethics Pre WeekDocumento16 páginasUP Legal Ethics Pre WeekWorstWitch TalaAinda não há avaliações

- (GM FM DPW) : Summary of Benefits Payable To Piece-Rate WorkersDocumento3 páginas(GM FM DPW) : Summary of Benefits Payable To Piece-Rate WorkersWorstWitch TalaAinda não há avaliações

- AM No. 07-9-12-SCDocumento4 páginasAM No. 07-9-12-SCWorstWitch TalaAinda não há avaliações

- Roxas Vs Macapagal-Arroyo DigestDocumento3 páginasRoxas Vs Macapagal-Arroyo DigestWorstWitch TalaAinda não há avaliações

- RA No.1059 IRRDocumento55 páginasRA No.1059 IRRWorstWitch TalaAinda não há avaliações

- AM No. 08-1-16-SCDocumento4 páginasAM No. 08-1-16-SCWorstWitch TalaAinda não há avaliações

- Ra No. 10353Documento5 páginasRa No. 10353WorstWitch TalaAinda não há avaliações

- Project WBS DronetechDocumento1 páginaProject WBS DronetechFunny Huh100% (2)

- Karnataka Current Affairs 2017 by AffairsCloudDocumento13 páginasKarnataka Current Affairs 2017 by AffairsCloudSinivas ParthaAinda não há avaliações

- 2013 Interview SheetDocumento3 páginas2013 Interview SheetIsabel Luchie GuimaryAinda não há avaliações

- ACE Consultancy AgreementDocumento0 páginaACE Consultancy AgreementjonchkAinda não há avaliações

- Dokumenti/ Këshilli I Europës Tregon Pse U Refuzuan Kandidatët e Qeverisë Shqiptare Për Gjyqtar Në StrasburgDocumento4 páginasDokumenti/ Këshilli I Europës Tregon Pse U Refuzuan Kandidatët e Qeverisë Shqiptare Për Gjyqtar Në StrasburgAnonymous pPe9isQYcSAinda não há avaliações

- Powerpoint - The Use of Animals in FightingDocumento18 páginasPowerpoint - The Use of Animals in Fightingcyc5326Ainda não há avaliações

- ASME Steam Table PDFDocumento32 páginasASME Steam Table PDFIsabel Pachucho100% (2)

- Recruiting in Europe: A Guide For EmployersDocumento12 páginasRecruiting in Europe: A Guide For EmployersLate ArtistAinda não há avaliações

- Quality Manual.4Documento53 páginasQuality Manual.4dcol13100% (1)

- Sample of Notarial WillDocumento3 páginasSample of Notarial WillJF Dan100% (1)

- Chinese OCW Conversational Chinese WorkbookDocumento283 páginasChinese OCW Conversational Chinese Workbookhnikol3945Ainda não há avaliações

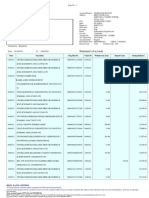

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocumento3 páginasStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceHiten AhirAinda não há avaliações

- Famous Slogan PDFDocumento16 páginasFamous Slogan PDFtarinisethy970Ainda não há avaliações

- PS Form 6387 Rural Money Order TransactionDocumento1 páginaPS Form 6387 Rural Money Order TransactionRoberto MonterrosaAinda não há avaliações

- Necrowarcasters Cards PDFDocumento157 páginasNecrowarcasters Cards PDFFrancisco Dolhabaratz100% (2)

- Icici Marketing Strategy of Icici BankDocumento68 páginasIcici Marketing Strategy of Icici BankShilpi KumariAinda não há avaliações

- Daily Technical Report 15.03.2013Documento4 páginasDaily Technical Report 15.03.2013Angel BrokingAinda não há avaliações

- Waf Rosary Group Leaflet - June 2018Documento2 páginasWaf Rosary Group Leaflet - June 2018Johnarie CardinalAinda não há avaliações

- Mas 2 Departmental ExamzDocumento8 páginasMas 2 Departmental ExamzjediiikAinda não há avaliações

- MOTION FOR SUMMARY JUDGMENT (Telegram)Documento59 páginasMOTION FOR SUMMARY JUDGMENT (Telegram)ForkLogAinda não há avaliações

- Tyrone Wilson StatementDocumento2 páginasTyrone Wilson StatementDaily FreemanAinda não há avaliações

- SAN JUAN ES. Moncada North Plantilla 1Documento1 páginaSAN JUAN ES. Moncada North Plantilla 1Jasmine Faye Gamotea - CabayaAinda não há avaliações

- Housing LawsDocumento114 páginasHousing LawsAlvin Clari100% (2)

- KEPITAL-POM - KEPITAL F20-03 LOF - en - RoHSDocumento8 páginasKEPITAL-POM - KEPITAL F20-03 LOF - en - RoHSEnzo AscañoAinda não há avaliações

- Shay Eshel - The Concept of The Elect Nation in Byzantium (2018, Brill) PDFDocumento234 páginasShay Eshel - The Concept of The Elect Nation in Byzantium (2018, Brill) PDFMarko DabicAinda não há avaliações

- Tabang vs. National Labor Relations CommissionDocumento6 páginasTabang vs. National Labor Relations CommissionRMC PropertyLawAinda não há avaliações

- E10726 PDFDocumento950 páginasE10726 PDFAhmad Zidny Azis TanjungAinda não há avaliações

- Bill Overview: Jlb96Kutpxdgxfivcivc Ykpfi9R9Ukywilxmvbj5Wpccvgaqc7FDocumento5 páginasBill Overview: Jlb96Kutpxdgxfivcivc Ykpfi9R9Ukywilxmvbj5Wpccvgaqc7FMani KalpanaAinda não há avaliações

- Facebook Expose Part 1 of WitnessesDocumento5 páginasFacebook Expose Part 1 of WitnessesByronHubbardAinda não há avaliações