Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Bank Documents (3rd PT FABM2)Documento18 páginasBank Documents (3rd PT FABM2)Rose BaynaAinda não há avaliações

- Cabaroan Elementary School-Bacnotan, La Union: Statement of AccountDocumento4 páginasCabaroan Elementary School-Bacnotan, La Union: Statement of AccountDianneAinda não há avaliações

- CBM - Group 3 - Batch BDocumento20 páginasCBM - Group 3 - Batch BANEESH KHANNAAinda não há avaliações

- Industrial SicknessDocumento10 páginasIndustrial SicknessAditya0% (1)

- FixedDepositsDocumento1 páginaFixedDepositsTiso Blackstar GroupAinda não há avaliações

- HFO HomeworkDocumento2 páginasHFO HomeworkAna May Durante BaldelomarAinda não há avaliações

- "Customer Attitude Towards COMMERCIAL LOANDocumento58 páginas"Customer Attitude Towards COMMERCIAL LOANPulkit SachdevaAinda não há avaliações

- Barangay Kagawad: Hon. Mohamad Jimmy D. AmpatuanDocumento2 páginasBarangay Kagawad: Hon. Mohamad Jimmy D. AmpatuanNawaf A. BalatukayAinda não há avaliações

- Income Tax ReviewerDocumento99 páginasIncome Tax ReviewerKarlo Marco Cleto100% (1)

- TR 7. Garcia v. CADocumento2 páginasTR 7. Garcia v. CAJyrus CimatuAinda não há avaliações

- SP: PAYTM Self Enrolment Process: GTPL Hathway LimitedDocumento16 páginasSP: PAYTM Self Enrolment Process: GTPL Hathway LimitedAnonymous 2Ck3Oa6FAinda não há avaliações

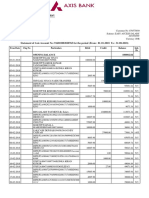

- Statement of Axis Account No:916010083028765 For The Period (From: 01-01-2018 To: 31-08-2018)Documento9 páginasStatement of Axis Account No:916010083028765 For The Period (From: 01-01-2018 To: 31-08-2018)Saran ManiAinda não há avaliações

- Loan Documentation PDFDocumento16 páginasLoan Documentation PDFMuhammad Akmal HossainAinda não há avaliações

- Robinsons Bank SpaDocumento1 páginaRobinsons Bank SpaMaricar Dasal BulandresAinda não há avaliações

- Banking Sector Reforms in IndiaDocumento43 páginasBanking Sector Reforms in IndiaChandini KambapuAinda não há avaliações

- Best of Mobile Pos 2014 PDFDocumento127 páginasBest of Mobile Pos 2014 PDFAndalynaAinda não há avaliações

- About Goldman SachsDocumento2 páginasAbout Goldman SachsanujAinda não há avaliações

- Global Bank of LiesDocumento1 páginaGlobal Bank of LiesDoctor MasonAinda não há avaliações

- CUTE Tutorial - Sample QuestionsDocumento72 páginasCUTE Tutorial - Sample QuestionsRamakrishnan Ramachandran100% (1)

- Assignment ON Merger of Centurian Bank of Punjab by HDFC BankDocumento10 páginasAssignment ON Merger of Centurian Bank of Punjab by HDFC BankAmardeep Singh SodhiAinda não há avaliações

- FAQs On Cheque Collection PolicyDocumento1 páginaFAQs On Cheque Collection PolicyPrasant PrasadAinda não há avaliações

- Banking SectorDocumento8 páginasBanking SectorSupreet KaurAinda não há avaliações

- Financial ReadinessDocumento101 páginasFinancial ReadinessMatthew Conboy100% (1)

- Transaction StatementDocumento10 páginasTransaction StatementChandan SripathiAinda não há avaliações

- Caprock Trade and Finance LLCDocumento3 páginasCaprock Trade and Finance LLCDaniel Reis NandovaAinda não há avaliações

- Banking Awareness EbookDocumento467 páginasBanking Awareness EbookSivaji Haldar50% (2)

- Chapter 24 - Working Capital Management - Current Assets and Current LiabilitiesDocumento44 páginasChapter 24 - Working Capital Management - Current Assets and Current LiabilitiesKashif Ahmed SaeedAinda não há avaliações

- Investing in Private Equity: UBS Alternative InvestmentsDocumento7 páginasInvesting in Private Equity: UBS Alternative InvestmentsAnonymous c7llQBcnAinda não há avaliações

- Building Economics and Sociology: Ix Semester, B.ArchDocumento138 páginasBuilding Economics and Sociology: Ix Semester, B.ArchVenkat KiranAinda não há avaliações

- CMA Part1EDocumento27 páginasCMA Part1EMaria100% (1)