Você também pode gostar

- Entrepreneurship Development A4Documento44 páginasEntrepreneurship Development A4paroothiAinda não há avaliações

- STWS Business Model ArchetypesDocumento1 páginaSTWS Business Model ArchetypesManjit SinghAinda não há avaliações

- MOS PGPM Individual Assignment 2Documento1 páginaMOS PGPM Individual Assignment 2Sukanta JanaAinda não há avaliações

- Final Exam - GM 8 - BelsDocumento2 páginasFinal Exam - GM 8 - BelsR NaritaAinda não há avaliações

- Attitude Change Strategy - Syndicate 4Documento7 páginasAttitude Change Strategy - Syndicate 4Busyairi Alfan RamadhanAinda não há avaliações

- Ayustinagiusti - Developing Financial Insights - Using A Future Value (FV) and A Present Value (PV) ApproachDocumento10 páginasAyustinagiusti - Developing Financial Insights - Using A Future Value (FV) and A Present Value (PV) ApproachAyustina GiustiAinda não há avaliações

- Q1. What Inference Do You Draw From The Trends in The Free Cash Flow of The Company?Documento6 páginasQ1. What Inference Do You Draw From The Trends in The Free Cash Flow of The Company?sridhar607Ainda não há avaliações

- Question 8: P&G Has Developed A New Toothpaste That Provides Tooth and Gum Protection ForDocumento3 páginasQuestion 8: P&G Has Developed A New Toothpaste That Provides Tooth and Gum Protection ForNgọc Thảo NguyễnAinda não há avaliações

- TDC Case FinalDocumento3 páginasTDC Case Finalbjefferson21Ainda não há avaliações

- AnageneDocumento1 páginaAnagenevijai100% (1)

- SG 2 - GM 9 - The Financial DetectiveDocumento10 páginasSG 2 - GM 9 - The Financial DetectiveMuhammad Wildan FadlillahAinda não há avaliações

- Oligopoly Competition in The Market With Food ProductsDocumento9 páginasOligopoly Competition in The Market With Food ProductsAnonymous qwKaEs3BoUAinda não há avaliações

- Better World Books Case StudyDocumento8 páginasBetter World Books Case StudyAndyy 吳 NgAinda não há avaliações

- Financial Management E BookDocumento4 páginasFinancial Management E BookAnshul MishraAinda não há avaliações

- Homework 4Documento3 páginasHomework 4amisha25625850% (1)

- Robert Miller Individual CaseDocumento7 páginasRobert Miller Individual Casesmithars100% (1)

- Aleph Farms Case Analysis Highlights Company's Focus on SustainabilityDocumento7 páginasAleph Farms Case Analysis Highlights Company's Focus on SustainabilityOlivia HorvathAinda não há avaliações

- Economics of Strategy: Sixth EditionDocumento63 páginasEconomics of Strategy: Sixth EditionRichardNicoArdyantoAinda não há avaliações

- Analyzing Consumer PerceptionDocumento19 páginasAnalyzing Consumer PerceptionRAJSHEKAR RAMPELLIAinda não há avaliações

- KNOWLEDGE MANAGEMENT INITIATIVES AT RESERVE BANKDocumento5 páginasKNOWLEDGE MANAGEMENT INITIATIVES AT RESERVE BANKBianda Puspita SariAinda não há avaliações

- Michael Porters Model For Industry and Competitor AnalysisDocumento9 páginasMichael Porters Model For Industry and Competitor AnalysisbagumaAinda não há avaliações

- NintendoDocumento5 páginasNintendoafif12Ainda não há avaliações

- Case Study K9FUELBARDocumento2 páginasCase Study K9FUELBARAnonymous xH0aLu100% (1)

- Ruosheng ZhangDocumento14 páginasRuosheng Zhangrazi087Ainda não há avaliações

- Cashlet 4Documento3 páginasCashlet 4Vinay SharmaAinda não há avaliações

- Distributive Approach for MANNx-OTC Joint VentureDocumento19 páginasDistributive Approach for MANNx-OTC Joint VentureSimon ErickAinda não há avaliações

- NetflixDocumento10 páginasNetflixHenry WaribuhAinda não há avaliações

- Financial Insight - Syndicate 5Documento8 páginasFinancial Insight - Syndicate 5Yunia Apriliani KartikaAinda não há avaliações

- 2003 Edition: This Bibliography Contains Abstracts of The 100 Best-Selling Cases During 2002Documento30 páginas2003 Edition: This Bibliography Contains Abstracts of The 100 Best-Selling Cases During 2002Raghib AliAinda não há avaliações

- Chapter10 StudentworksheetDocumento45 páginasChapter10 StudentworksheetMohitAinda não há avaliações

- Initiation For Increasing Brand ValueDocumento4 páginasInitiation For Increasing Brand ValueKrishAinda não há avaliações

- Customer Relationship ManagementDocumento16 páginasCustomer Relationship ManagementUzma Hussain0% (1)

- Business Model Innovation Faculty: Prof. Srivastava, RajendraDocumento8 páginasBusiness Model Innovation Faculty: Prof. Srivastava, RajendraseawoodsAinda não há avaliações

- Rationale For Unrelated Product Diversification For Indian FirmsDocumento10 páginasRationale For Unrelated Product Diversification For Indian FirmsarcherselevatorsAinda não há avaliações

- An Appraisal of Dividend Policy of Meghna Cement Mills LimitedDocumento21 páginasAn Appraisal of Dividend Policy of Meghna Cement Mills LimitedMd. Mesbah Uddin100% (6)

- I. Case BackgroundDocumento7 páginasI. Case BackgroundHiya BhandariBD21070Ainda não há avaliações

- Business Intelligence Software at Sysco 1Documento5 páginasBusiness Intelligence Software at Sysco 1Dellendo FarquharsonAinda não há avaliações

- CM Strat YipDocumento9 páginasCM Strat Yipmeherey2kAinda não há avaliações

- SecA - Group5 - The Best of IntentionsDocumento8 páginasSecA - Group5 - The Best of IntentionsVijay KrishnanAinda não há avaliações

- Accounting & Information Management Kanthal Case StudyDocumento5 páginasAccounting & Information Management Kanthal Case StudyMuhammad Hafidz AkbarAinda não há avaliações

- Case: Better Sales Networks by Tuba Ustuner and David GodesDocumento16 páginasCase: Better Sales Networks by Tuba Ustuner and David GodesShailja JajodiaAinda não há avaliações

- Decision Models and Optimization: Indian School of Business Assignment 4Documento8 páginasDecision Models and Optimization: Indian School of Business Assignment 4NAAinda não há avaliações

- Swati Anand - FRMcaseDocumento5 páginasSwati Anand - FRMcaseBhavin MohiteAinda não há avaliações

- Tugas Finance Management Individu - MBA ITB - CCE58 2018 ExcelDocumento10 páginasTugas Finance Management Individu - MBA ITB - CCE58 2018 ExcelDenssAinda não há avaliações

- BSE Case StudyDocumento2 páginasBSE Case Studykowshik moyyaAinda não há avaliações

- Cambridge IGCSE: 0450/12 Business StudiesDocumento67 páginasCambridge IGCSE: 0450/12 Business StudiesZaidhamidAinda não há avaliações

- SCM - Managing Uncertainty in DemandDocumento27 páginasSCM - Managing Uncertainty in DemandHari Madhavan Krishna KumarAinda não há avaliações

- Bookbinders Book Club Case (Customer Choice)Documento3 páginasBookbinders Book Club Case (Customer Choice)Abhishek MishraAinda não há avaliações

- Nintendo's Disruptive Strategy: Implications For The Video Game IndustryDocumento68 páginasNintendo's Disruptive Strategy: Implications For The Video Game IndustryAdrian NewAinda não há avaliações

- Sara's Options AnalysisDocumento14 páginasSara's Options AnalysisGaurav ThakurAinda não há avaliações

- The Financial Detective, 2005Documento10 páginasThe Financial Detective, 2005Kara BelesAinda não há avaliações

- IB SummaryDocumento7 páginasIB SummaryrronakrjainAinda não há avaliações

- Casestudy Nego 1Documento3 páginasCasestudy Nego 1Claire0% (1)

- CaseDocumento1 páginaCaseSaad AhmedAinda não há avaliações

- Answers To CtbankDocumento18 páginasAnswers To CtbankshubhamAinda não há avaliações

- The Future of Workforce at _VOISDocumento7 páginasThe Future of Workforce at _VOISAnu SahithiAinda não há avaliações

- CiscoDocumento80 páginasCiscoAnonymous fEViTz3v6Ainda não há avaliações

- Flashion Case Questions PDFDocumento1 páginaFlashion Case Questions PDFAnkitAinda não há avaliações

- Operation ManagementDocumento8 páginasOperation ManagementBhaavyn SutariaAinda não há avaliações

- Capital Budgeting Decisions A Clear and Concise ReferenceNo EverandCapital Budgeting Decisions A Clear and Concise ReferenceAinda não há avaliações

- 10-Item Sim Score GradingDocumento19 páginas10-Item Sim Score GradingKyan WongAinda não há avaliações

- McClellan-Product vs. CommodityDocumento4 páginasMcClellan-Product vs. CommodityDeepan BaalanAinda não há avaliações

- McClellan-Product vs. CommodityDocumento4 páginasMcClellan-Product vs. CommodityDeepan BaalanAinda não há avaliações

- Financial Market Efficienecy Case StudyDocumento12 páginasFinancial Market Efficienecy Case StudyDeepan BaalanAinda não há avaliações

- Business Model of FacebookDocumento7 páginasBusiness Model of Facebookabhinav pandeyAinda não há avaliações

- Ambarish GuptaDocumento3 páginasAmbarish GuptaMahesh Uma MallikondlaAinda não há avaliações

- 42 Rules of Product Management (2nd Edition)Documento22 páginas42 Rules of Product Management (2nd Edition)HappyAbout100% (1)

- Whitepaper Indian RetailDocumento51 páginasWhitepaper Indian RetailDeepan BaalanAinda não há avaliações

- ABCWear Digital Marketing PlanDocumento13 páginasABCWear Digital Marketing PlanDeepan BaalanAinda não há avaliações

- MLA University TP Case Study 03feb15 2 PagesDocumento2 páginasMLA University TP Case Study 03feb15 2 PagesDeepan BaalanAinda não há avaliações

- McKaskill Ultimate Growth StrategiesDocumento162 páginasMcKaskill Ultimate Growth StrategiesRobert GronbeckAinda não há avaliações

- Managing Radical ChangeDocumento30 páginasManaging Radical ChangeDeepan BaalanAinda não há avaliações

- Airline TOC Case StudyDocumento126 páginasAirline TOC Case StudyDeepan BaalanAinda não há avaliações

- Best Housing Loan for Alya AqilahDocumento20 páginasBest Housing Loan for Alya AqilahSHARIFAH NUR AFIQAH BINTI SYED HISAN SABRYAinda não há avaliações

- CSC Practice QS PDFDocumento304 páginasCSC Practice QS PDFDavid Young0% (1)

- Capital Budgeting-Theory and NumericalsDocumento47 páginasCapital Budgeting-Theory and Numericalssaadsaaid50% (2)

- Garuda Indonesia Case AnalysisDocumento8 páginasGaruda Indonesia Case AnalysisPatDabz67% (3)

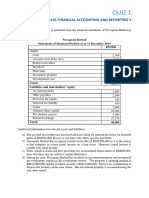

- Lecture Notes Lectures 1 9 Advanced Financial AccountingDocumento22 páginasLecture Notes Lectures 1 9 Advanced Financial Accountingsir sahb100% (1)

- Luxury Motor Home Sales & CostsDocumento6 páginasLuxury Motor Home Sales & CostsUmer AhmadAinda não há avaliações

- Chapter 03 - How Securities Are TradedDocumento8 páginasChapter 03 - How Securities Are TradedSarahAinda não há avaliações

- Bill of Sale of Motor Vehicle or Automobile Without Warranty WWW Gazhoo ComDocumento5 páginasBill of Sale of Motor Vehicle or Automobile Without Warranty WWW Gazhoo ComEddy clayAinda não há avaliações

- Novogratz Berhad 2014 Financials and Tax CalculationDocumento3 páginasNovogratz Berhad 2014 Financials and Tax CalculationMohd NuuranAinda não há avaliações

- Trust Receipts CasesDocumento44 páginasTrust Receipts CasesKarlo Marco CletoAinda não há avaliações

- Objection To Ptfs Ex Parte M4Substitution of Party PlaintiffDocumento8 páginasObjection To Ptfs Ex Parte M4Substitution of Party PlaintiffzonelizzardAinda não há avaliações

- Slide 3 - Retail Banking OperationsDocumento73 páginasSlide 3 - Retail Banking OperationsRashi JainAinda não há avaliações

- Account Management and Loss Allowance Guidance Checklist Pub CH A CCL Acct MGMT Loss Allowance ChecklistDocumento5 páginasAccount Management and Loss Allowance Guidance Checklist Pub CH A CCL Acct MGMT Loss Allowance ChecklistHelpin HandAinda não há avaliações

- Creative Accounting Full EditDocumento11 páginasCreative Accounting Full EditHabib MohdAinda não há avaliações

- Solidbank V Gateway April 2008Documento26 páginasSolidbank V Gateway April 2008BAROPSAinda não há avaliações

- Lesson+09 Simple+and+Compound+Interest DetailedDocumento23 páginasLesson+09 Simple+and+Compound+Interest DetailedCedrick Nicolas ValeraAinda não há avaliações

- Sample of Memorandum of AgreementDocumento2 páginasSample of Memorandum of AgreementJuris PoetAinda não há avaliações

- Sale of GoodsDocumento27 páginasSale of GoodsPavel Shibanov100% (3)

- PAS 1 With Notes - Pres of FS PDFDocumento75 páginasPAS 1 With Notes - Pres of FS PDFFatima Ann GuevarraAinda não há avaliações

- Legal Obligations and Contract RequirementsDocumento29 páginasLegal Obligations and Contract RequirementskulsoomalamAinda não há avaliações

- TPA9Documento58 páginasTPA9Dr. Dharmender Patial50% (2)

- Sales - Quote Service LoopDocumento2 páginasSales - Quote Service LoopIng Rebeca C Sayago FerrerAinda não há avaliações

- What Are The Various Streams of AccountingDocumento13 páginasWhat Are The Various Streams of AccountingvijaybhaskarreddymeeAinda não há avaliações

- Acknowledging Support for Banking ReportDocumento35 páginasAcknowledging Support for Banking Reportpriya.sahaAinda não há avaliações

- Contact MERALCO for Electric Bill InquiriesDocumento2 páginasContact MERALCO for Electric Bill InquirieslrbbAinda não há avaliações

- 08 Superlines Transportation Company, Inc. vs. ICC Leasing & Financing CorporationDocumento19 páginas08 Superlines Transportation Company, Inc. vs. ICC Leasing & Financing CorporationJerelleen RodriguezAinda não há avaliações

- Credit Transactions NotesDocumento12 páginasCredit Transactions Notesmicah badilloAinda não há avaliações

- Advanced Financial Management by ICPAP PDFDocumento265 páginasAdvanced Financial Management by ICPAP PDFjj0% (1)

- PO BFN 2044 Bank - Management April 2015Documento9 páginasPO BFN 2044 Bank - Management April 2015Qatadah IsmailAinda não há avaliações