Você também pode gostar

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (120)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Mortgage Loan BasicsDocumento7 páginasMortgage Loan BasicsJyoti SinghAinda não há avaliações

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- FORECLOSURE Response To JP Morgan Chase ForeclosureDocumento102 páginasFORECLOSURE Response To JP Morgan Chase ForeclosureLAUREN J TRATAR96% (23)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Simple Interest and Maturity ValueDocumento2 páginasSimple Interest and Maturity ValueMary100% (6)

- APC Ch6solDocumento22 páginasAPC Ch6solAnonymous LusWvy100% (8)

- Chap 11 Credit Risk Individual LoansDocumento116 páginasChap 11 Credit Risk Individual LoansAfnan100% (1)

- The Big ShortDocumento5 páginasThe Big ShortАлександр НефедовAinda não há avaliações

- Valuation and Hedging of Inv Floaters PDFDocumento4 páginasValuation and Hedging of Inv Floaters PDFtiwariaradAinda não há avaliações

- EAMCET - 2012 Toppers in Engineering: Page 3 of 4Documento2 páginasEAMCET - 2012 Toppers in Engineering: Page 3 of 445satishAinda não há avaliações

- Solution Manual For Accounting 8th Canadian Edition by HorngrenDocumento53 páginasSolution Manual For Accounting 8th Canadian Edition by Horngrena239005954100% (1)

- MarchDocumento3 páginasMarch45satishAinda não há avaliações

- Apeapcet 2023Documento1 páginaApeapcet 202345satishAinda não há avaliações

- TIMETABLE (March 2021term)Documento2 páginasTIMETABLE (March 2021term)45satishAinda não há avaliações

- TIMETABLE SEPT 2019 TermDocumento2 páginasTIMETABLE SEPT 2019 Term45satishAinda não há avaliações

- MarchDocumento3 páginasMarch45satishAinda não há avaliações

- 3) CommitteesDocumento8 páginas3) Committees45satishAinda não há avaliações

- Group-I Services SPORTS Category-28-2022 - 14072023Documento2 páginasGroup-I Services SPORTS Category-28-2022 - 1407202345satishAinda não há avaliações

- Andhra Pradesh Public Service Commission # Hyderabad Departmental Tests May, 2017 Session NOTIFICATION NO.06/2017Documento1 páginaAndhra Pradesh Public Service Commission # Hyderabad Departmental Tests May, 2017 Session NOTIFICATION NO.06/201745satishAinda não há avaliações

- TIMETABLE (March 2021term)Documento2 páginasTIMETABLE (March 2021term)45satishAinda não há avaliações

- Certificate of ResidenceDocumento1 páginaCertificate of ResidenceVenkatarao KankanalaAinda não há avaliações

- PaperCode 3 13 21 35 54 71Documento3 páginasPaperCode 3 13 21 35 54 7145satishAinda não há avaliações

- Feb First Week FullDocumento20 páginasFeb First Week FullNarendiran ChakravarthyAinda não há avaliações

- FisheriesDocumento1 páginaFisheries45satishAinda não há avaliações

- PC 2 12 20Documento3 páginasPC 2 12 2045satishAinda não há avaliações

- Notification Employees Provident Fund Organisation Assistant Posts PDFDocumento40 páginasNotification Employees Provident Fund Organisation Assistant Posts PDFMahesh PawarAinda não há avaliações

- DM (F©H$ Boim (Ddau: Mavr À (V Y (V Am¡A (D (Z Mos ©Documento52 páginasDM (F©H$ Boim (Ddau: Mavr À (V Y (V Am¡A (D (Z Mos ©45satishAinda não há avaliações

- Don'T Be Forced Don'T Be Misguided .:: WWW - Sebi.gov - inDocumento1 páginaDon'T Be Forced Don'T Be Misguided .:: WWW - Sebi.gov - in45satishAinda não há avaliações

- Office Order No. 33/5/2004 Subject:-Govt. of India Resolution On Public Interest Disclosures & Protection of InformerDocumento6 páginasOffice Order No. 33/5/2004 Subject:-Govt. of India Resolution On Public Interest Disclosures & Protection of Informer45satishAinda não há avaliações

- 1292926908940Documento82 páginas1292926908940ruchisinghnovAinda não há avaliações

- Final-Grade A and B - Recruitment Notification - 24dec2020Documento24 páginasFinal-Grade A and B - Recruitment Notification - 24dec2020Mohit KumarAinda não há avaliações

- General Insurance Corporation of India: (A Government of India Company) Recruitment of Scale I OfficersDocumento34 páginasGeneral Insurance Corporation of India: (A Government of India Company) Recruitment of Scale I Officers45satishAinda não há avaliações

- Economic Survey 2020-21Documento81 páginasEconomic Survey 2020-2145satishAinda não há avaliações

- 1292926908940Documento82 páginas1292926908940ruchisinghnovAinda não há avaliações

- SebiDocumento1 páginaSebi45satishAinda não há avaliações

- Asian Development Bank Institute: ADBI Working Paper SeriesDocumento33 páginasAsian Development Bank Institute: ADBI Working Paper SeriesnareshkumaranAinda não há avaliações

- Asian Development Bank Institute: ADBI Working Paper SeriesDocumento33 páginasAsian Development Bank Institute: ADBI Working Paper SeriesnareshkumaranAinda não há avaliações

- Risk Management - 2Documento53 páginasRisk Management - 2Pravin LakudzodeAinda não há avaliações

- Financial Inclusion 4Documento6 páginasFinancial Inclusion 445satishAinda não há avaliações

- Financial Inclusion 4Documento6 páginasFinancial Inclusion 445satishAinda não há avaliações

- Comparative AnalysisDocumento6 páginasComparative AnalysisKathryn Bianca AcanceAinda não há avaliações

- 4.2 CompoundDocumento18 páginas4.2 CompoundSzchel Eariel VillarinAinda não há avaliações

- Acris CodesDocumento12 páginasAcris Codesbob dole100% (1)

- CXC Csec ExamsDocumento4 páginasCXC Csec ExamsCali Shane TaylorAinda não há avaliações

- Ia2 Ka & SolDocumento31 páginasIa2 Ka & SolCarlah Jeane BasinaAinda não há avaliações

- Val AplnoticeDocumento2 páginasVal AplnoticeHennyza FaisalAinda não há avaliações

- Student Loan Questionnaire 0809Documento2 páginasStudent Loan Questionnaire 0809bidyuttezuAinda não há avaliações

- United Malayan Banking Corp BHD V Ernest CheDocumento13 páginasUnited Malayan Banking Corp BHD V Ernest ChenestleomegasAinda não há avaliações

- Consumer Mathematics: Borrowing: Loans and Loan RepaymentDocumento22 páginasConsumer Mathematics: Borrowing: Loans and Loan RepaymentAlthea Noelfei QuisaganAinda não há avaliações

- Chapter - I, Ii, Iii, IvDocumento92 páginasChapter - I, Ii, Iii, IvHarichandran KarthikeyanAinda não há avaliações

- CDCSCWWDocumento11 páginasCDCSCWWdavidAinda não há avaliações

- Fixed Income Markets - Assignment: Symbiosis School of Banking and Finance (SSBF)Documento10 páginasFixed Income Markets - Assignment: Symbiosis School of Banking and Finance (SSBF)Abhilash NAinda não há avaliações

- Basic of Sarfaesi ActDocumento4 páginasBasic of Sarfaesi ActsrinivaspdfAinda não há avaliações

- Numbers and Statistics: Posted On April 22, 2008by LzhgladiatorDocumento3 páginasNumbers and Statistics: Posted On April 22, 2008by LzhgladiatorЮлияAinda não há avaliações

- Prudent ARC Ltd. v. Indu Techzone Pvt. Ltd.Documento3 páginasPrudent ARC Ltd. v. Indu Techzone Pvt. Ltd.Navneet BhatiaAinda não há avaliações

- LNS 2016 1 1198Documento30 páginasLNS 2016 1 1198T.r. OoiAinda não há avaliações

- Simple Interest - 2021-2022Documento23 páginasSimple Interest - 2021-2022racquel bagaAinda não há avaliações

- @@bond &bond Valuation-4!24!21Documento37 páginas@@bond &bond Valuation-4!24!21Mark LesterAinda não há avaliações

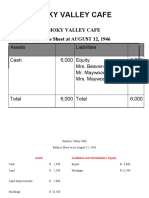

- Smoky Valley CafeDocumento3 páginasSmoky Valley CafeRajkumar KrishnamoorthyAinda não há avaliações

- BANKRUPTCY - Abdul Razak Senin-Appeal Ag BN - PublishDocumento12 páginasBANKRUPTCY - Abdul Razak Senin-Appeal Ag BN - Publishhafeez benignAinda não há avaliações

- Ecc Gen MathDocumento26 páginasEcc Gen MathloidaAinda não há avaliações

- MTGE CheatsheetDocumento2 páginasMTGE CheatsheetandrewzkyAinda não há avaliações