Você também pode gostar

- Heidi Roizen - Case Study: MBA ZG515 - Consulting & People SkillsDocumento7 páginasHeidi Roizen - Case Study: MBA ZG515 - Consulting & People Skillsnihal agrawalAinda não há avaliações

- Cat FightDocumento2 páginasCat FightSwati AgrahariAinda não há avaliações

- Investment Analysis and Tri Star Lockheed - FULL FINALDocumento8 páginasInvestment Analysis and Tri Star Lockheed - FULL FINALCheytan Thakar100% (3)

- Toyota Motor Manufacturing USA., inDocumento5 páginasToyota Motor Manufacturing USA., inmudasserAinda não há avaliações

- Solutions To Chapters 7 and 8 Problem SetsDocumento21 páginasSolutions To Chapters 7 and 8 Problem SetsMuhammad Hasnain100% (1)

- Andreessen Horowitz FinalDocumento4 páginasAndreessen Horowitz FinalYuqin ChenAinda não há avaliações

- Planning Its Itinerary Into The FutureDocumento5 páginasPlanning Its Itinerary Into The FuturedhinuramAinda não há avaliações

- Project Management Analysis in The Internet Forecasting IndustryDocumento14 páginasProject Management Analysis in The Internet Forecasting IndustryNiranjan NidadavoluAinda não há avaliações

- Tristar Case Sol.Documento4 páginasTristar Case Sol.Niketa JaiswalAinda não há avaliações

- Decision Models and Optimization: Sample-Endterm-with SolutionsDocumento6 páginasDecision Models and Optimization: Sample-Endterm-with SolutionsYash NyatiAinda não há avaliações

- Chapter 6 Financial AssetsDocumento6 páginasChapter 6 Financial AssetsSteffany RoqueAinda não há avaliações

- Beta Management Company SummaryDocumento8 páginasBeta Management Company Summarysabohi83% (6)

- Case AnalysisDocumento5 páginasCase AnalysisShrijaSrivAinda não há avaliações

- Six Sigma Quality at Flyrock Tires: Prepared By: Trevor CantrellDocumento5 páginasSix Sigma Quality at Flyrock Tires: Prepared By: Trevor Cantrellsidharth dasAinda não há avaliações

- Jetblue Airways 609046-PDF-ENG - Case StudyDocumento9 páginasJetblue Airways 609046-PDF-ENG - Case StudyvikramAinda não há avaliações

- GEMS TDDocumento4 páginasGEMS TDMarissa BradleyAinda não há avaliações

- Annuity, Gradient, PerpetuityDocumento2 páginasAnnuity, Gradient, PerpetuityJsbebe jskdbsj100% (3)

- Law Officer Professional Knowledge Question PaperDocumento11 páginasLaw Officer Professional Knowledge Question Papernikunj joshiAinda não há avaliações

- Jetblue'S Decision To Add E190 To Its Fleet. Agree?: Advantages DisadvantagesDocumento1 páginaJetblue'S Decision To Add E190 To Its Fleet. Agree?: Advantages DisadvantagesAkhil Goutham KotiniAinda não há avaliações

- Lockheed Tristar Case Study 11020241041Documento19 páginasLockheed Tristar Case Study 11020241041R Harika Reddy100% (7)

- The Rich FoolDocumento26 páginasThe Rich FoolSTEVEN TULAAinda não há avaliações

- Written Analysis of Case: Alden Products, Inc. - European ManufacturingDocumento7 páginasWritten Analysis of Case: Alden Products, Inc. - European ManufacturingMalik Wasiq Mustafa100% (1)

- Investment Analysis - Lockheed Tri-StarDocumento2 páginasInvestment Analysis - Lockheed Tri-Staraclink88100% (1)

- Locheed Case Study Group 1Documento9 páginasLocheed Case Study Group 1Michael DevereauxAinda não há avaliações

- Lockheed Tristar Case SolutionDocumento3 páginasLockheed Tristar Case SolutionPrakash Nishtala100% (1)

- Sample Problems-DMOPDocumento5 páginasSample Problems-DMOPChakri MunagalaAinda não há avaliações

- How Does The Internal Market For Innovation at Nypro FunctionDocumento2 páginasHow Does The Internal Market For Innovation at Nypro Functionprerna004Ainda não há avaliações

- Sealed Air Corporation's Leveraged RecapitalizationDocumento7 páginasSealed Air Corporation's Leveraged RecapitalizationKumarAinda não há avaliações

- Lockheed Tristar Case Similar SolutionDocumento12 páginasLockheed Tristar Case Similar SolutionguruprasadkudvaAinda não há avaliações

- Classic Knitwear Case (Section-B Group-1)Documento5 páginasClassic Knitwear Case (Section-B Group-1)Swapnil Joardar100% (1)

- EC2101 Practice Problems 8 SolutionDocumento3 páginasEC2101 Practice Problems 8 Solutiongravity_coreAinda não há avaliações

- Print OutDocumento17 páginasPrint OutRobin BishwajeetAinda não há avaliações

- Corp Gov Group1 - Sealed AirDocumento5 páginasCorp Gov Group1 - Sealed Airdmathur1234Ainda não há avaliações

- Nitesh Kumar Singh TOSDocumento4 páginasNitesh Kumar Singh TOSNitesh KumarAinda não há avaliações

- Gillette Dry IdeaDocumento5 páginasGillette Dry IdeaAnirudh PrasadAinda não há avaliações

- Case Study: Dreamworld Amusement Park Dreamworld: Initial Years of OperationDocumento3 páginasCase Study: Dreamworld Amusement Park Dreamworld: Initial Years of OperationArnav MittalAinda não há avaliações

- "The New Science of Salesforce Productivity": Reading SummaryDocumento2 páginas"The New Science of Salesforce Productivity": Reading SummarypratyakshmalviAinda não há avaliações

- A Note On Leveraged RecapitalizationDocumento5 páginasA Note On Leveraged Recapitalizationkuch bhiAinda não há avaliações

- Precise Software Solutions Case StudyDocumento3 páginasPrecise Software Solutions Case StudyKrishnaprasad ChenniyangirinathanAinda não há avaliações

- Analyse The Structure of The Personal Computer Industry Over The Last 15 YearsDocumento7 páginasAnalyse The Structure of The Personal Computer Industry Over The Last 15 Yearsdbleyzer100% (1)

- Sealed Air Corporation's Leveraged Recapitalization (A)Documento7 páginasSealed Air Corporation's Leveraged Recapitalization (A)Jyoti GuptaAinda não há avaliações

- Lockheed Case SolutionDocumento3 páginasLockheed Case SolutionKashish SrivastavaAinda não há avaliações

- Dividend Policy at FPL GroupDocumento20 páginasDividend Policy at FPL Groupczx88Ainda não há avaliações

- Marriott CorporationDocumento8 páginasMarriott CorporationtarunAinda não há avaliações

- Barilla Spa (Hbs 9-694-046) - Case Study Submission: Executive SummaryDocumento3 páginasBarilla Spa (Hbs 9-694-046) - Case Study Submission: Executive SummaryRichaAinda não há avaliações

- Case: Calpine Corporation: The Evolution From Project To Corporate FinanceDocumento7 páginasCase: Calpine Corporation: The Evolution From Project To Corporate FinanceKshitishAinda não há avaliações

- World Class ManufacturingDocumento6 páginasWorld Class ManufacturingAdlin Kaushal Dsouza 19008Ainda não há avaliações

- WAC-P16052 Dhruvkumar-West Lake Case AnalysisDocumento7 páginasWAC-P16052 Dhruvkumar-West Lake Case AnalysisDHRUV SONAGARAAinda não há avaliações

- Wilkins, A Zurn Company: Demand Forecasting: Submitted By: Group-8 Section-CDocumento6 páginasWilkins, A Zurn Company: Demand Forecasting: Submitted By: Group-8 Section-CHEM BANSALAinda não há avaliações

- Bellaire (B) CaseDocumento2 páginasBellaire (B) CaseNirali Shah100% (2)

- Case Questions WilkinsDocumento1 páginaCase Questions Wilkinsvimal_prajapatiAinda não há avaliações

- The Company: Strength WeaknessDocumento10 páginasThe Company: Strength Weaknessvky2929Ainda não há avaliações

- Mgmt489 Kraft ADocumento6 páginasMgmt489 Kraft Arooba24Ainda não há avaliações

- PGP12101 B Akula Padma Priya DADocumento20 páginasPGP12101 B Akula Padma Priya DApadma priya akulaAinda não há avaliações

- Trend Analysis of Ultratech Cement - Aditya Birla Group.Documento9 páginasTrend Analysis of Ultratech Cement - Aditya Birla Group.Kanhay VishariaAinda não há avaliações

- Assignment: Individual Assignment 4 - Philips: Lighting Up Eden GardensDocumento5 páginasAssignment: Individual Assignment 4 - Philips: Lighting Up Eden GardensVinayAinda não há avaliações

- QMDocumento87 páginasQMjyotisagar talukdarAinda não há avaliações

- Exercise 1 SolnDocumento2 páginasExercise 1 Solndarinjohson0% (2)

- Question-Set 2: How Did You Handle The Ambiguity in Your Decision-Making? What WasDocumento6 páginasQuestion-Set 2: How Did You Handle The Ambiguity in Your Decision-Making? What WasishaAinda não há avaliações

- Ingersoll Rand Sec B Group 1Documento8 páginasIngersoll Rand Sec B Group 1biakAinda não há avaliações

- Case 2 & 3 - Cashing Our & Indian Sugar IndustryDocumento8 páginasCase 2 & 3 - Cashing Our & Indian Sugar Industrymohitrameshagrawal100% (2)

- Lockheed Tri Star and Capital Budgeting Case Analysis: ProfessorDocumento8 páginasLockheed Tri Star and Capital Budgeting Case Analysis: ProfessorlicservernoidaAinda não há avaliações

- Management Advisory ServicesDocumento28 páginasManagement Advisory ServicesAnnaliza DonqueAinda não há avaliações

- Stephanie Ott Advanced Corporate Finance Midterm The Boeing 777Documento11 páginasStephanie Ott Advanced Corporate Finance Midterm The Boeing 777Steph OttAinda não há avaliações

- Unit 1Documento10 páginasUnit 1AlfatihahAinda não há avaliações

- Combine Client Wise Summary ReportDocumento1 páginaCombine Client Wise Summary Reportakshat tvAinda não há avaliações

- Types of Dividend PolicyDocumento7 páginasTypes of Dividend PolicyRakibul Islam JonyAinda não há avaliações

- B40Documento7 páginasB40ambujg0% (1)

- AUDIT PROBS-2nd MONTHLY ASSESSMENTDocumento7 páginasAUDIT PROBS-2nd MONTHLY ASSESSMENTGRACELYN SOJORAinda não há avaliações

- Merchandising - Review Materials (Problems)Documento65 páginasMerchandising - Review Materials (Problems)julsAinda não há avaliações

- Customer Welcome ChecklistDocumento4 páginasCustomer Welcome Checklistjupiter stationeryAinda não há avaliações

- Solution Practice 9 Business Combinations and ImpairmentDocumento8 páginasSolution Practice 9 Business Combinations and ImpairmentGuinevereAinda não há avaliações

- Assurance VieDocumento4 páginasAssurance Vievincent.reynaud.74Ainda não há avaliações

- Wacc AssignmentDocumento3 páginasWacc AssignmentSaboorAinda não há avaliações

- The Yamuna Syndicate Limited: Ratings Upgraded Summary of Rating ActionDocumento8 páginasThe Yamuna Syndicate Limited: Ratings Upgraded Summary of Rating ActionSandy SanAinda não há avaliações

- AuditingDocumento9 páginasAuditingRenAinda não há avaliações

- Askari Bank LTDDocumento3 páginasAskari Bank LTDNayab AliAinda não há avaliações

- 9 IS-LM Model and Policy EffectivenessDocumento21 páginas9 IS-LM Model and Policy EffectivenessShajeer HamAinda não há avaliações

- Petty CashDocumento8 páginasPetty Cashevy sabacajanAinda não há avaliações

- IC Property Management Rent Receipt TemplateDocumento2 páginasIC Property Management Rent Receipt Templatelaundromat360Ainda não há avaliações

- Digital Revolution in International TradeDocumento18 páginasDigital Revolution in International Tradedepan belakangAinda não há avaliações

- A Post Keynesian Framework of Exchange Rate Determination A Minskyan ApproachDocumento24 páginasA Post Keynesian Framework of Exchange Rate Determination A Minskyan ApproachFelipe RomeroAinda não há avaliações

- Practical Accounting 2 First Pre-Board ExaminationDocumento15 páginasPractical Accounting 2 First Pre-Board ExaminationKaren Eloisse89% (9)

- @csupdates Chapter 21 CIRP, Liquidation Wining Up SBECDocumento29 páginas@csupdates Chapter 21 CIRP, Liquidation Wining Up SBECthevinayakshuklaaAinda não há avaliações

- Unit 4 Cash Flow StatementDocumento26 páginasUnit 4 Cash Flow Statementjatin4verma-2Ainda não há avaliações

- Accounting P1 May-June 2023 EngDocumento12 páginasAccounting P1 May-June 2023 EngKaren ErasmusAinda não há avaliações

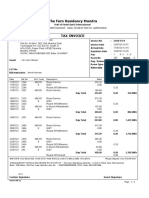

- The Fern Residency Mundra: MR - Yash VithalaniDocumento2 páginasThe Fern Residency Mundra: MR - Yash VithalaniPREM KUMAR KUSHAWAHAAinda não há avaliações

- CH 03Documento61 páginasCH 03Muhammad RamzanAinda não há avaliações

- Mahindra FinanaceDocumento14 páginasMahindra FinanaceIshita BhagatAinda não há avaliações

- RECORDING BUSINESS TRANSACTIONS PostingDocumento76 páginasRECORDING BUSINESS TRANSACTIONS PostingThriztan Andrei BaluyutAinda não há avaliações