Você também pode gostar

- Apelo - SPADocumento2 páginasApelo - SPAPau JoyosaAinda não há avaliações

- SHPEEDocumento1 páginaSHPEEPau JoyosaAinda não há avaliações

- Motion To WithdrawDocumento3 páginasMotion To WithdrawPau JoyosaAinda não há avaliações

- Affidavit of LossDocumento1 páginaAffidavit of LossPau JoyosaAinda não há avaliações

- Sworn Affidavit of No RelativesDocumento1 páginaSworn Affidavit of No RelativesPau JoyosaAinda não há avaliações

- Gmail - LBCEXPRESS IPP OnlineDocumento1 páginaGmail - LBCEXPRESS IPP OnlinePau JoyosaAinda não há avaliações

- DOAS - AmbasDocumento2 páginasDOAS - AmbasPau JoyosaAinda não há avaliações

- Abigail V Joyosa - CV (Updated)Documento2 páginasAbigail V Joyosa - CV (Updated)Pau JoyosaAinda não há avaliações

- Spa - MallareDocumento1 páginaSpa - MallarePau JoyosaAinda não há avaliações

- Letter To PeoplesDocumento1 páginaLetter To PeoplesPau JoyosaAinda não há avaliações

- Provisional remedies principal actionsDocumento19 páginasProvisional remedies principal actionsPau JoyosaAinda não há avaliações

- Aff - OneandTheSame - MercadoErispeDocumento1 páginaAff - OneandTheSame - MercadoErispePau JoyosaAinda não há avaliações

- SPA - PatapatDocumento2 páginasSPA - PatapatPau JoyosaAinda não há avaliações

- Affidavit of LossDocumento1 páginaAffidavit of LossPau JoyosaAinda não há avaliações

- Zarak Demand Letter For Payment FinalDocumento2 páginasZarak Demand Letter For Payment FinalPau JoyosaAinda não há avaliações

- Affidavit of Solo ParentDocumento2 páginasAffidavit of Solo ParentPau JoyosaAinda não há avaliações

- Contract of Lease: Block 5 Lot 9 Melbourne St. Margarita HMS, San Antonio, Biñan City, LagunaDocumento4 páginasContract of Lease: Block 5 Lot 9 Melbourne St. Margarita HMS, San Antonio, Biñan City, LagunaPau JoyosaAinda não há avaliações

- NLRC Reconsiders Dismissal of Illegal Dismissal CaseDocumento8 páginasNLRC Reconsiders Dismissal of Illegal Dismissal CasePau JoyosaAinda não há avaliações

- RR NO. 9A - CaBaMiRo Zonal Values NoticeDocumento1.774 páginasRR NO. 9A - CaBaMiRo Zonal Values NoticeFaty Bercasio90% (20)

- Deed of Sale WITH RIGHT OF REPURCHASEDocumento2 páginasDeed of Sale WITH RIGHT OF REPURCHASEPau Joyosa100% (4)

- Demand Letter - Anabel LunaDocumento1 páginaDemand Letter - Anabel LunaPau JoyosaAinda não há avaliações

- Special Power of Attorney: Glady V. JoyosaDocumento2 páginasSpecial Power of Attorney: Glady V. JoyosaPau JoyosaAinda não há avaliações

- Extra-Judicial Settlement and Waiver of RightsDocumento3 páginasExtra-Judicial Settlement and Waiver of RightsPau JoyosaAinda não há avaliações

- Joint Affidavit of Disinterested PersonsDocumento1 páginaJoint Affidavit of Disinterested PersonsPau JoyosaAinda não há avaliações

- ExhibitsDocumento1 páginaExhibitsPau JoyosaAinda não há avaliações

- Obtaining certified documentsDocumento2 páginasObtaining certified documentsPau JoyosaAinda não há avaliações

- Settlement of Gracita Bautista EstateDocumento4 páginasSettlement of Gracita Bautista EstatePau JoyosaAinda não há avaliações

- SP Case No. SP-16-0158Documento6 páginasSP Case No. SP-16-0158Pau JoyosaAinda não há avaliações

- Affidavit of Solo ParentDocumento2 páginasAffidavit of Solo ParentPau JoyosaAinda não há avaliações

- Demand Letter - Anabel LunaDocumento1 páginaDemand Letter - Anabel LunaPau JoyosaAinda não há avaliações

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5784)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (119)

- Ola BillDocumento3 páginasOla BillMohit TanwarAinda não há avaliações

- Account STMTDocumento6 páginasAccount STMTNaveenchdrAinda não há avaliações

- Form# 037 Merchant Processing Application Tell Us ...Documento9 páginasForm# 037 Merchant Processing Application Tell Us ...David Paul Henson67% (3)

- Final Reviewer For TAX 2Documento45 páginasFinal Reviewer For TAX 2Mosarah AltAinda não há avaliações

- Muhammad Fahmy Bin KamalizamDocumento1 páginaMuhammad Fahmy Bin KamalizamtotokAinda não há avaliações

- TCS On Sale of Goods: Padmanathan K V, Chartered AccountantDocumento20 páginasTCS On Sale of Goods: Padmanathan K V, Chartered AccountantSainaath RAinda não há avaliações

- Introduction To Customs DutyDocumento34 páginasIntroduction To Customs DutyKunal Thakor67% (3)

- Miss Juliet September Statement... 2022Documento6 páginasMiss Juliet September Statement... 2022adilAinda não há avaliações

- KPLC Prepaid Meters User GuideDocumento12 páginasKPLC Prepaid Meters User GuidezanguvitabuAinda não há avaliações

- KoinX-Complete Tax Report - OptionsDocumento13 páginasKoinX-Complete Tax Report - OptionsBhavsmeetforeverAinda não há avaliações

- Poonawalla TowersDocumento3 páginasPoonawalla TowersezycredAinda não há avaliações

- Order FL0187768315: Mode of Payment: NONCODDocumento1 páginaOrder FL0187768315: Mode of Payment: NONCODRavi ChopraAinda não há avaliações

- The Individual Master File (IMF) Report, Form #09.056Documento123 páginasThe Individual Master File (IMF) Report, Form #09.056Sovereignty Education and Defense Ministry (SEDM)89% (9)

- Resume of MichellequimbyDocumento2 páginasResume of Michellequimbyapi-30093031Ainda não há avaliações

- Contoh Laporan Laba Rugi KoinWorksDocumento1 páginaContoh Laporan Laba Rugi KoinWorksDiftya Twas Galih AtyasaAinda não há avaliações

- Salary income tax solutionsDocumento76 páginasSalary income tax solutionsvinayak ShedgeAinda não há avaliações

- Bank Fees and Charges Guide for Peso TransactionsDocumento9 páginasBank Fees and Charges Guide for Peso TransactionsRod LaquintaAinda não há avaliações

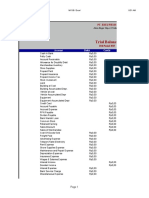

- Trial Balance - Melvino YDocumento4 páginasTrial Balance - Melvino YTrainingDigital Marketing BandungAinda não há avaliações

- Fee Notification For The Academic Year 2023-24Documento15 páginasFee Notification For The Academic Year 2023-24Makrand DeouskarAinda não há avaliações

- Kashato Shirts: General JournalDocumento34 páginasKashato Shirts: General JournalJade Cruz100% (1)

- CTA Decision on Systra Philippines Tax Refund ClaimDocumento13 páginasCTA Decision on Systra Philippines Tax Refund ClaimRuther Marc P. NarcidaAinda não há avaliações

- m1050 Credit Card Debt ProjectDocumento5 páginasm1050 Credit Card Debt Projectapi-302403854Ainda não há avaliações

- Taxation Review on Property TransactionsDocumento4 páginasTaxation Review on Property TransactionsTrisha Sargento EncinaresAinda não há avaliações

- Tax Invoice: Booking DetailsDocumento2 páginasTax Invoice: Booking DetailsRajiv SinghAinda não há avaliações

- e-StatementBRImo 346401034434533 Aug2023 20231026 215241Documento3 páginase-StatementBRImo 346401034434533 Aug2023 20231026 215241Noviyanti 008Ainda não há avaliações

- 2024 Full Time FeesDocumento1 página2024 Full Time Fees8r6cqx7fv6Ainda não há avaliações

- Ibe Steve Godspower 0071436323 20221018071544Documento102 páginasIbe Steve Godspower 0071436323 20221018071544IK Steve ChinedumAinda não há avaliações

- Correction of ErrorDocumento3 páginasCorrection of ErrorAna Rosario OnidaAinda não há avaliações

- Next Gen Pharma: (Original For Recipient) Sold byDocumento2 páginasNext Gen Pharma: (Original For Recipient) Sold bydarpajAinda não há avaliações

- f1040s1 PDFDocumento1 páginaf1040s1 PDFCarlosAinda não há avaliações