Você também pode gostar

- Ajay Dond - Prognoz ResumeDocumento3 páginasAjay Dond - Prognoz ResumeMukesh ManwaniAinda não há avaliações

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Black BookDocumento16 páginasBlack BookMukesh ManwaniAinda não há avaliações

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5795)

- Blanck Format For Vender CreationDocumento3 páginasBlanck Format For Vender CreationMukesh ManwaniAinda não há avaliações

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- MadhuDocumento1 páginaMadhuMukesh ManwaniAinda não há avaliações

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- Irctcs E Ticketing Service Electronic Reservation Slip (Personal User)Documento2 páginasIrctcs E Ticketing Service Electronic Reservation Slip (Personal User)Mukesh ManwaniAinda não há avaliações

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- Complete Project Report - Organic Farm Performance in MinnesotaDocumento8 páginasComplete Project Report - Organic Farm Performance in MinnesotaMukesh ManwaniAinda não há avaliações

- Organic FarmingDocumento49 páginasOrganic FarmingMukesh ManwaniAinda não há avaliações

- Bhavesh Khatri CVDocumento1 páginaBhavesh Khatri CVMukesh ManwaniAinda não há avaliações

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Search Criteria Agent Id: MIG0081061: Recurring Deposit Installment ReportDocumento2 páginasSearch Criteria Agent Id: MIG0081061: Recurring Deposit Installment ReportMukesh ManwaniAinda não há avaliações

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- A) Height Height Relaxation: Candidates Falling in The Categories ofDocumento1 páginaA) Height Height Relaxation: Candidates Falling in The Categories ofMukesh ManwaniAinda não há avaliações

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- E TicketDocumento1 páginaE TicketMukesh ManwaniAinda não há avaliações

- A Study On Employee Satisfaction (With Special Reference To A.P.S.R.T.C Sangareddy Bus Depot)Documento9 páginasA Study On Employee Satisfaction (With Special Reference To A.P.S.R.T.C Sangareddy Bus Depot)Mukesh ManwaniAinda não há avaliações

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Pankaj DadlaniDocumento1 páginaPankaj DadlaniMukesh ManwaniAinda não há avaliações

- Hypothesis Test PaperDocumento3 páginasHypothesis Test PaperMukesh ManwaniAinda não há avaliações

- Primer On Goods and Services TaxDocumento50 páginasPrimer On Goods and Services TaxMukesh ManwaniAinda não há avaliações

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- Agreement of Leave and LicenceDocumento6 páginasAgreement of Leave and LicenceMukesh ManwaniAinda não há avaliações

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Food Truck PresentationDocumento11 páginasFood Truck Presentationapi-454000622Ainda não há avaliações

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Iibf ExamDocumento13 páginasIibf ExamRahul MondalAinda não há avaliações

- Investment Banking ProjectDocumento28 páginasInvestment Banking ProjectDilip Ahir0% (1)

- Exam MB7-701 Microsoft Dynamics NAV 2013 Core Setup and FinanceDocumento3 páginasExam MB7-701 Microsoft Dynamics NAV 2013 Core Setup and Financekashram2001Ainda não há avaliações

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- Research Blue Report AppDocumento280 páginasResearch Blue Report AppRudi UtomoAinda não há avaliações

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1091)

- Financial Accounting: Accounting Basics: Branches of AccountingDocumento7 páginasFinancial Accounting: Accounting Basics: Branches of AccountingLucky HartanAinda não há avaliações

- Start-Up Real Estate Business PlanDocumento29 páginasStart-Up Real Estate Business Plankalpesh86patel924675% (4)

- Channels - 5Documento17 páginasChannels - 5Mulugeta GirmaAinda não há avaliações

- Pravinn Mahajan CA FINAL SFM-NOV2011 Ques PaperDocumento9 páginasPravinn Mahajan CA FINAL SFM-NOV2011 Ques PaperPravinn_MahajanAinda não há avaliações

- Nonfiction Book Proposal One SheetDocumento1 páginaNonfiction Book Proposal One SheetGreenleaf Book Group100% (1)

- Annual Report of Pakistan Oilfield Limited (POL)Documento22 páginasAnnual Report of Pakistan Oilfield Limited (POL)Kehkashan AnsariAinda não há avaliações

- HRM Project Report On Performance Appraisal System at BSNL, Performance Appraisal System Project Report MBA BBA, HRM Project Report, HR Project ReportDocumento4 páginasHRM Project Report On Performance Appraisal System at BSNL, Performance Appraisal System Project Report MBA BBA, HRM Project Report, HR Project ReportDeepti SinghAinda não há avaliações

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Game TheoryDocumento32 páginasGame TheoryMemoona AmbreenAinda não há avaliações

- Obtaining Technology - PlanningDocumento37 páginasObtaining Technology - PlanningputerimatunAinda não há avaliações

- Loan Functions of BanksDocumento6 páginasLoan Functions of BanksMark AmistosoAinda não há avaliações

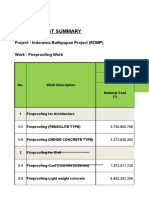

- Skp. 187 Pt. Eti - Revisi Fireproofing Tahap 1 Material CarbolineDocumento157 páginasSkp. 187 Pt. Eti - Revisi Fireproofing Tahap 1 Material CarbolineRiesky Firdyan100% (1)

- (MIDTERM) AAP - Module 5 PSA-315-320-330-450Documento6 páginas(MIDTERM) AAP - Module 5 PSA-315-320-330-45025 CUNTAPAY, FRENCHIE VENICE B.Ainda não há avaliações

- Construction Procurement and Contract Management: Week 1-2: Chapter I: IntroductionDocumento4 páginasConstruction Procurement and Contract Management: Week 1-2: Chapter I: IntroductionRenalyn AnogAinda não há avaliações

- CompensationDocumento17 páginasCompensationConie BabierraAinda não há avaliações

- Assessing New Product Development Success Factors in The Thai Food IndustryDocumento23 páginasAssessing New Product Development Success Factors in The Thai Food IndustryNuttoShinAinda não há avaliações

- 28th Annual Report 2013-2014 SunfflagDocumento71 páginas28th Annual Report 2013-2014 SunfflagSiddharth ShekharAinda não há avaliações

- Audit Plan and ProgramDocumento35 páginasAudit Plan and ProgramReginald ValenciaAinda não há avaliações

- Unpaid Leave in UAE During Coronavirus All You Need To KnowDocumento5 páginasUnpaid Leave in UAE During Coronavirus All You Need To KnowSithick MohamedAinda não há avaliações

- Ch04 - Recruitment and Selection - Potocnik Et Al. (2014)Documento45 páginasCh04 - Recruitment and Selection - Potocnik Et Al. (2014)Erica ReedAinda não há avaliações

- Contracts NovationDocumento10 páginasContracts Novationkimberly.chiuhAinda não há avaliações

- Chap 1Documento5 páginasChap 1Lệ Mẫn TrầnAinda não há avaliações

- Everest Group Global in House Center GIC Landscape Annual Report 2018 CA 1Documento9 páginasEverest Group Global in House Center GIC Landscape Annual Report 2018 CA 1Parthurnax RevengeAinda não há avaliações

- Virgin Mobile USA: Pricing For The Very First Time: International Master in Business Administration (IMB) 2014/2015Documento5 páginasVirgin Mobile USA: Pricing For The Very First Time: International Master in Business Administration (IMB) 2014/2015shagun khandelwalAinda não há avaliações

- Revised Pharmaceutical Supply Transformation Plan 2018-2020Documento76 páginasRevised Pharmaceutical Supply Transformation Plan 2018-2020Demis TeshomeAinda não há avaliações

- 2 - Revenue, Costs and Break EvenDocumento4 páginas2 - Revenue, Costs and Break EvenHadeel DossaAinda não há avaliações

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamNo EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamAinda não há avaliações