Você também pode gostar

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- Reviewer Labor RelDocumento5 páginasReviewer Labor RelMaricrisAinda não há avaliações

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Regional Trial Court Branch 51: Rtc2sor051@judiciary - Gov.phDocumento4 páginasRegional Trial Court Branch 51: Rtc2sor051@judiciary - Gov.phMaricrisAinda não há avaliações

- Donors TaxDocumento6 páginasDonors TaxMaricrisAinda não há avaliações

- OCA Circular No. 51-2021Documento2 páginasOCA Circular No. 51-2021MaricrisAinda não há avaliações

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Affidavit of Desistance: Regional Trial CourtDocumento1 páginaAffidavit of Desistance: Regional Trial CourtMaricrisAinda não há avaliações

- OCA Circular No. 209-2020Documento31 páginasOCA Circular No. 209-2020MaricrisAinda não há avaliações

- Special Power of AttorneyDocumento1 páginaSpecial Power of AttorneyMaricrisAinda não há avaliações

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

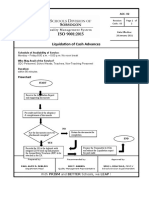

- ACC 02 PROCESS MANUAL Liquidation of Cash AdvancesDocumento2 páginasACC 02 PROCESS MANUAL Liquidation of Cash AdvancesMaricrisAinda não há avaliações

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- ACC 03 PROCESS MANUAL Lddap Ada FacilityDocumento2 páginasACC 03 PROCESS MANUAL Lddap Ada FacilityMaricrisAinda não há avaliações

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- OCA Circular No. 60-2021Documento3 páginasOCA Circular No. 60-2021MaricrisAinda não há avaliações

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

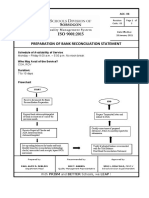

- ACC 06 PROCESS MANUAL Bank ReconDocumento7 páginasACC 06 PROCESS MANUAL Bank ReconMaricrisAinda não há avaliações

- Republic of The Philippines: (Revised As of April 1992)Documento1 páginaRepublic of The Philippines: (Revised As of April 1992)MaricrisAinda não há avaliações

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Handout No. 14Documento22 páginasHandout No. 14MaricrisAinda não há avaliações

- Bir Form 1601E - Schedule I Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of March, 2018Documento10 páginasBir Form 1601E - Schedule I Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of March, 2018MaricrisAinda não há avaliações

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- Labor Repair (Office Equipment) Labor Repair (Office Equipment)Documento7 páginasLabor Repair (Office Equipment) Labor Repair (Office Equipment)MaricrisAinda não há avaliações

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- Acc 01 Process Manual Mooe DownloadingDocumento2 páginasAcc 01 Process Manual Mooe DownloadingMaricrisAinda não há avaliações

- Bir Form 1601E - Schedule I Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of May, 2018Documento5 páginasBir Form 1601E - Schedule I Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of May, 2018MaricrisAinda não há avaliações

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- Bir Form 1601E - Schedule I Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of June, 2018Documento5 páginasBir Form 1601E - Schedule I Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of June, 2018MaricrisAinda não há avaliações

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Bir Form 1601E - Schedule I Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of January, 2018Documento5 páginasBir Form 1601E - Schedule I Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of January, 2018MaricrisAinda não há avaliações

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Bir Form 1601E - Schedule I Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of August, 2018Documento10 páginasBir Form 1601E - Schedule I Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of August, 2018MaricrisAinda não há avaliações

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Willy and Sons Corporation - Sorsogon: Concepcion Carrier Product Specialist 09460098500/ 09277777854Documento1 páginaWilly and Sons Corporation - Sorsogon: Concepcion Carrier Product Specialist 09460098500/ 09277777854MaricrisAinda não há avaliações

- Bulletin 05Documento4 páginasBulletin 05Allan YdiaAinda não há avaliações

- 2017 Cashier's ReportDocumento21 páginas2017 Cashier's ReportMaricrisAinda não há avaliações

- Crim Law Reviewer 2Documento82 páginasCrim Law Reviewer 2MaricrisAinda não há avaliações

- The Real Life Tara Mohr PDFDocumento13 páginasThe Real Life Tara Mohr PDFMaricrisAinda não há avaliações

- Remedial Law (Civil Procedure) - San Beda 2011 PDFDocumento123 páginasRemedial Law (Civil Procedure) - San Beda 2011 PDFRuby SantillanaAinda não há avaliações

- MARSHALL 3RD BOOK - Tragics MistakesDocumento55 páginasMARSHALL 3RD BOOK - Tragics MistakesChris Pearson100% (3)

- Louw 3Documento27 páginasLouw 3ZeabMariaAinda não há avaliações

- Tutorial - Chapter 11 - Monetary Policy - QuestionsDocumento4 páginasTutorial - Chapter 11 - Monetary Policy - QuestionsNandiieAinda não há avaliações

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Bill Ackman Value Investing Congress 100112Documento103 páginasBill Ackman Value Investing Congress 100112abc_dAinda não há avaliações

- MBA (E) 2021-23, 3rd Semester All Subjects SyllabusDocumento40 páginasMBA (E) 2021-23, 3rd Semester All Subjects SyllabusANISHA DUTTAAinda não há avaliações

- Ticks Hunter Bot GuideDocumento7 páginasTicks Hunter Bot GuideKingtayAinda não há avaliações

- Mirae Factsheet April2017Documento16 páginasMirae Factsheet April2017Dashang G. MakwanaAinda não há avaliações

- Government of PunjabDocumento1 páginaGovernment of PunjabPunjab Drainage Department0% (1)

- Introduction To AccountingDocumento57 páginasIntroduction To AccountingJustine MaravillaAinda não há avaliações

- IBT MCQ and Essay QuestionsDocumento9 páginasIBT MCQ and Essay QuestionsCristine BilocuraAinda não há avaliações

- Unit 5 Iapm CapmDocumento11 páginasUnit 5 Iapm Capmshubham JaiswalAinda não há avaliações

- Foreign Exchange Management Act - WikipediaDocumento29 páginasForeign Exchange Management Act - WikipediaMoon SandAinda não há avaliações

- 11.25.2017 Accounting For Income TaxDocumento5 páginas11.25.2017 Accounting For Income TaxPatOcampo0% (1)

- Your Guide To Perfect CreditDocumento168 páginasYour Guide To Perfect Creditwhistjenn100% (5)

- Miga Professionals Program PDFDocumento2 páginasMiga Professionals Program PDFPaul Ivan Beppe a Yombo Paul IvanAinda não há avaliações

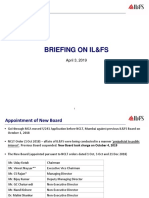

- ILFS Briefing (April 2019)Documento15 páginasILFS Briefing (April 2019)Richard DierdreAinda não há avaliações

- Sample Contract To SellDocumento3 páginasSample Contract To SellCandice Tongco-Cruz100% (4)

- Pi IPSAS Is Cash Still King v5Documento50 páginasPi IPSAS Is Cash Still King v5Grecia Dalina Vizcarra VAinda não há avaliações

- 11 Actividad #4 Crucigrama Contabilidad VDocumento3 páginas11 Actividad #4 Crucigrama Contabilidad VMaria F OrtizAinda não há avaliações

- Rangkuman TaDocumento19 páginasRangkuman Tamutia rasyaAinda não há avaliações

- Index For Capital Gains TaxDocumento15 páginasIndex For Capital Gains TaxWilma P.Ainda não há avaliações

- 1 Introduction To BankingDocumento8 páginas1 Introduction To BankingGurnihalAinda não há avaliações

- CV 1Documento3 páginasCV 1suherlanAinda não há avaliações

- Manufacturing Accounts FormatDocumento7 páginasManufacturing Accounts Formatlaguda babajide100% (10)

- Audit of Property, Plant and Equipment: Auditing ProblemsDocumento5 páginasAudit of Property, Plant and Equipment: Auditing ProblemsLei PangilinanAinda não há avaliações

- Stanley F. Allen F.C.A. (Aust.) - The Pirates of Finance (1947)Documento69 páginasStanley F. Allen F.C.A. (Aust.) - The Pirates of Finance (1947)bookbenderAinda não há avaliações

- Iblr220800068978 PDFDocumento1 páginaIblr220800068978 PDFMURALI HNAinda não há avaliações

- In The United States Bankruptcy Court For The District of Delaware in Re:) Chapter 11 Pacific Energy Resources LTD., Et Al.,') Case No. 09-10785 (KJC) ) (Jointly Administered) Debtor.)Documento67 páginasIn The United States Bankruptcy Court For The District of Delaware in Re:) Chapter 11 Pacific Energy Resources LTD., Et Al.,') Case No. 09-10785 (KJC) ) (Jointly Administered) Debtor.)Chapter 11 DocketsAinda não há avaliações

- Non Face To Face Form With AMB Declaration PDFDocumento10 páginasNon Face To Face Form With AMB Declaration PDFrohit.godhani9724Ainda não há avaliações

- Co Operative SocietyDocumento101 páginasCo Operative SocietyRaghu Ck100% (2)

- Tax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProNo EverandTax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProNota: 4.5 de 5 estrelas4.5/5 (43)

- Small Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyNo EverandSmall Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyAinda não há avaliações

- The Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyNo EverandThe Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyNota: 4 de 5 estrelas4/5 (52)