Você também pode gostar

- SR - No. Od/Cc Account No Name of The Party Date &sanc. Amt (Rs. in Lakhs)Documento14 páginasSR - No. Od/Cc Account No Name of The Party Date &sanc. Amt (Rs. in Lakhs)Rupesh MoreAinda não há avaliações

- Cash Management PolicyDocumento4 páginasCash Management PolicyRupesh More100% (1)

- Name of The Person Being RelievedDocumento1 páginaName of The Person Being RelievedRupesh MoreAinda não há avaliações

- Handover NoteDocumento3 páginasHandover NoteRupesh MoreAinda não há avaliações

- Cash ManagementDocumento44 páginasCash ManagementRupesh MoreAinda não há avaliações

- Planning of Financial AuditDocumento43 páginasPlanning of Financial AuditRupesh MoreAinda não há avaliações

- Balance of PaymentDocumento35 páginasBalance of PaymentRupesh MoreAinda não há avaliações

- A Study On Human Resource Management Strategies IN: (Standard Chartered Bank)Documento56 páginasA Study On Human Resource Management Strategies IN: (Standard Chartered Bank)Vikash GovindAinda não há avaliações

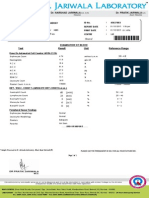

- Examination of Blood Result Unit Reference Range Test: GeneralDocumento1 páginaExamination of Blood Result Unit Reference Range Test: GeneralRupesh MoreAinda não há avaliações

- MDP Nomination Form: Management Development Program Is A One Day Executive WorkshopDocumento2 páginasMDP Nomination Form: Management Development Program Is A One Day Executive WorkshopRupesh MoreAinda não há avaliações

- MDP Nomination Form: Management Development ProgramDocumento2 páginasMDP Nomination Form: Management Development ProgramRupesh MoreAinda não há avaliações

- Msepolciy DocumentDocumento27 páginasMsepolciy DocumentRupesh MoreAinda não há avaliações

- MDP - Technical Analysis - Web Brochure - Sep - 2015Documento8 páginasMDP - Technical Analysis - Web Brochure - Sep - 2015Rupesh MoreAinda não há avaliações

- Operational Risk Management-Need For Adequate Systems and ControlsDocumento35 páginasOperational Risk Management-Need For Adequate Systems and ControlsRupesh MoreAinda não há avaliações

- Effects of Management Accounting Practices On Financial Performance of Manufacturing Companies in Kenya PeterDocumento74 páginasEffects of Management Accounting Practices On Financial Performance of Manufacturing Companies in Kenya PeterRupesh More100% (1)

- Review Investment PolicyDocumento33 páginasReview Investment PolicyRupesh MoreAinda não há avaliações

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Chapter One 1.1 Background of The StudyDocumento34 páginasChapter One 1.1 Background of The StudyChidi EmmanuelAinda não há avaliações

- Budgeting and FinancingDocumento3 páginasBudgeting and FinancingMondrei TVAinda não há avaliações

- Red Clay School District - Special Investigations ReportDocumento26 páginasRed Clay School District - Special Investigations ReportJohn AllisonAinda não há avaliações

- Nestle Finance International LTD Fullyear Financial Report 2021 enDocumento37 páginasNestle Finance International LTD Fullyear Financial Report 2021 enT.k.e.dAinda não há avaliações

- AUDITINGDocumento4 páginasAUDITINGAnna Dela CruzAinda não há avaliações

- Ke Toan Quoc Te Excel Bai TapDocumento115 páginasKe Toan Quoc Te Excel Bai TapLê NaAinda não há avaliações

- Bengal & Assam CompanyDocumento64 páginasBengal & Assam Companyvishal_patil_3Ainda não há avaliações

- D1-02-01 - Att 2 - Project Execution Plan R03 PDFDocumento164 páginasD1-02-01 - Att 2 - Project Execution Plan R03 PDFUyavie ObonnaAinda não há avaliações

- F2 Past Paper - Question12-2005Documento13 páginasF2 Past Paper - Question12-2005ArsalanACCA100% (1)

- Created by Excel My LifeDocumento4 páginasCreated by Excel My LifeBhuwan SharmaAinda não há avaliações

- GFR and Advances: Made ObjectiveDocumento48 páginasGFR and Advances: Made ObjectiveSurendra Sharma78% (27)

- 320 (April 2013) PDFDocumento19 páginas320 (April 2013) PDFChanzey ɢғxAinda não há avaliações

- Types of DirectorsDocumento4 páginasTypes of DirectorskrishAinda não há avaliações

- 1 Year PGDRMDocumento36 páginas1 Year PGDRMVishak H PillaiAinda não há avaliações

- Special JournalsDocumento14 páginasSpecial JournalsMarlou Danieles100% (1)

- Article CritiqueDocumento5 páginasArticle CritiqueFauzi Al nassarAinda não há avaliações

- Assignment 2Documento2 páginasAssignment 2Sidharth ChughAinda não há avaliações

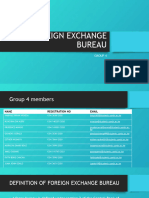

- Foreign Exchange BureauDocumento48 páginasForeign Exchange BureauevakairigoAinda não há avaliações

- BTEC National Business Unit 3 MCQ Revision Pack Vol 1 SampleDocumento6 páginasBTEC National Business Unit 3 MCQ Revision Pack Vol 1 SampleAnonymous BNnIEKkNtAinda não há avaliações

- Qa Technic Customer Audit Report-9001 (Qa Technic LTD) - Awh International Logistics Sdn. Bhd.Documento5 páginasQa Technic Customer Audit Report-9001 (Qa Technic LTD) - Awh International Logistics Sdn. Bhd.Harits As SiddiqAinda não há avaliações

- Unit 03 The Financial Statement AuditDocumento31 páginasUnit 03 The Financial Statement AuditYeobo DarlingAinda não há avaliações

- Chapter 3 - Ethics, Fraud and Internal ControlDocumento8 páginasChapter 3 - Ethics, Fraud and Internal ControlHads LunaAinda não há avaliações

- CAS 706 Emphasis of MatterDocumento10 páginasCAS 706 Emphasis of MatterzelcomeiaukAinda não há avaliações

- 2 Notes Lecture Audit of Cash 2021Documento1 página2 Notes Lecture Audit of Cash 2021JoyluxxiAinda não há avaliações

- Minutes SampleDocumento2 páginasMinutes SampleKitty MeatiiAinda não há avaliações

- OPMAN - Chapter 10 (ISO 9000 - Quality Management System)Documento28 páginasOPMAN - Chapter 10 (ISO 9000 - Quality Management System)polxrixAinda não há avaliações

- Column Fields Field: Additional Navigational AttributesDocumento25 páginasColumn Fields Field: Additional Navigational AttributesSajanAndyAinda não há avaliações

- 11e Ch3 Mini Case Planning MemoDocumento10 páginas11e Ch3 Mini Case Planning MemoHao Cui0% (1)

- Ctolibas Ac550 Assignment1 Unit1Documento4 páginasCtolibas Ac550 Assignment1 Unit1May-AnnJoyRedoñaAinda não há avaliações

- Planet Payment Inc.Documento50 páginasPlanet Payment Inc.ArvinLedesmaChiongAinda não há avaliações