Você também pode gostar

- Natural Gas - UpdateDocumento42 páginasNatural Gas - Updatesatish_xpAinda não há avaliações

- Gas Price Hike Impact Analysis 200510Documento5 páginasGas Price Hike Impact Analysis 200510vishi.segalAinda não há avaliações

- APC 3Q EPS Preview: Smooth Sailing in 3Q But 2019 Guidance Could Be The HighlightDocumento10 páginasAPC 3Q EPS Preview: Smooth Sailing in 3Q But 2019 Guidance Could Be The HighlightAshokAinda não há avaliações

- CMP: INR279 TP: INR320 Buy: Upstream Shared 32% in 1QFY13 V/s 40% in FY12Documento10 páginasCMP: INR279 TP: INR320 Buy: Upstream Shared 32% in 1QFY13 V/s 40% in FY12pmchotaliaAinda não há avaliações

- NTPC, 1Q Fy 2014Documento11 páginasNTPC, 1Q Fy 2014Angel BrokingAinda não há avaliações

- Gujarat Mineral Development Corporation LTD: Retail ResearchDocumento16 páginasGujarat Mineral Development Corporation LTD: Retail ResearchumaganAinda não há avaliações

- Upstream PSU Sector Report - Big Bang Reforms - Positive For Upstream PSUs - Nov 19, 2014Documento19 páginasUpstream PSU Sector Report - Big Bang Reforms - Positive For Upstream PSUs - Nov 19, 2014priyaranjanAinda não há avaliações

- KCCI E-Bulletin (Feb. 4, 2016)Documento1 páginaKCCI E-Bulletin (Feb. 4, 2016)ShahzadAinda não há avaliações

- India - Oil & Gas: Major Reforms Push, Oil Psus Key BeneficiariesDocumento9 páginasIndia - Oil & Gas: Major Reforms Push, Oil Psus Key BeneficiariesgirishrajsAinda não há avaliações

- No Respite: Cess On Domestically Produced Crude Changed From Rs 4,500/t (Specific) To 20% Ad ValoremDocumento8 páginasNo Respite: Cess On Domestically Produced Crude Changed From Rs 4,500/t (Specific) To 20% Ad ValoremAnonymous y3hYf50mTAinda não há avaliações

- Fertilisers - UpdateDocumento7 páginasFertilisers - Updatesatish_xpAinda não há avaliações

- Efert - FDSDocumento4 páginasEfert - FDSWaqas TayyabAinda não há avaliações

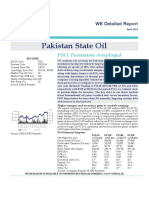

- PSO Detailed Report 2Documento9 páginasPSO Detailed Report 2Javaid IqbalAinda não há avaliações

- ONGC - Stock Update 240921Documento14 páginasONGC - Stock Update 240921Mohit MauryaAinda não há avaliações

- Financial Markets - Trading Report - 2Documento5 páginasFinancial Markets - Trading Report - 2Usman AhmadAinda não há avaliações

- It's Costing More To Find A Barrel.Documento2 páginasIt's Costing More To Find A Barrel.ghandatAinda não há avaliações

- MRF 2Q Sy 2013Documento12 páginasMRF 2Q Sy 2013Angel BrokingAinda não há avaliações

- Daily Agri Report, 28th January 2013Documento8 páginasDaily Agri Report, 28th January 2013Angel BrokingAinda não há avaliações

- Grms Improves On Back of Diesel Spreads: Oil and Gas MonthlyDocumento5 páginasGrms Improves On Back of Diesel Spreads: Oil and Gas MonthlynnsriniAinda não há avaliações

- Gujarat Gas: Performance HighlightsDocumento10 páginasGujarat Gas: Performance HighlightsAngel BrokingAinda não há avaliações

- Oil&Gas Sector 4 April'11 NewDocumento191 páginasOil&Gas Sector 4 April'11 NewthisisvbAinda não há avaliações

- EFL - IPO Fertilizer InformationDocumento4 páginasEFL - IPO Fertilizer InformationFaizan AhmedAinda não há avaliações

- KiritParekhCommitteeReport AngelDocumento5 páginasKiritParekhCommitteeReport AngelshshashankAinda não há avaliações

- Oil - Downstream - Update - Jan 15Documento37 páginasOil - Downstream - Update - Jan 15satish_xpAinda não há avaliações

- Gujarat Gas Result UpdatedDocumento10 páginasGujarat Gas Result UpdatedAngel BrokingAinda não há avaliações

- Castrol India LTDDocumento18 páginasCastrol India LTDSakshi BajajAinda não há avaliações

- CardinalStone Research - Forte Oil PLC - Higher Fuel Margins, Geregu Upgrade, A Plus For 2016 EarningsDocumento10 páginasCardinalStone Research - Forte Oil PLC - Higher Fuel Margins, Geregu Upgrade, A Plus For 2016 EarningsDhameloolah LawalAinda não há avaliações

- Ultratech Cement: CMP: INR4,009 TP: INR4,675 (+17%)Documento8 páginasUltratech Cement: CMP: INR4,009 TP: INR4,675 (+17%)sandeeptirukotiAinda não há avaliações

- Oil and Gas IndustryDocumento6 páginasOil and Gas IndustrySoubam LuxmibaiAinda não há avaliações

- Coal Mining: NeutralDocumento32 páginasCoal Mining: NeutralJohn SebastianAinda não há avaliações

- Scope of Tight Gas ReservoirDocumento26 páginasScope of Tight Gas ReservoirMuhammad Jahangir100% (1)

- Financial Analysis: Petronet LNG LTDDocumento19 páginasFinancial Analysis: Petronet LNG LTDVivek AntilAinda não há avaliações

- ONGC Result UpdatedDocumento11 páginasONGC Result UpdatedAngel BrokingAinda não há avaliações

- The Tanker MarketDocumento9 páginasThe Tanker Marketahujadeepti2581Ainda não há avaliações

- Inox Wind: Taxiing On The RunwayDocumento8 páginasInox Wind: Taxiing On The RunwayumaganAinda não há avaliações

- Petroleum StatisticsDocumento44 páginasPetroleum StatisticsIliasAinda não há avaliações

- IDirect IndiaCement CoUpdate Oct16Documento4 páginasIDirect IndiaCement CoUpdate Oct16umaganAinda não há avaliações

- Gujarat GAS, 22nd February, 2013Documento10 páginasGujarat GAS, 22nd February, 2013Angel BrokingAinda não há avaliações

- Ongc 1qfy2013ru 140812Documento11 páginasOngc 1qfy2013ru 140812Angel BrokingAinda não há avaliações

- Gujarat State Petronet, 1Q FY 2014Documento9 páginasGujarat State Petronet, 1Q FY 2014Angel BrokingAinda não há avaliações

- Ar09 10Documento156 páginasAr09 10Harry SidhuAinda não há avaliações

- Financial Position of Ultra Tech: Financials-Q4FY07Documento4 páginasFinancial Position of Ultra Tech: Financials-Q4FY07rahulpatel27Ainda não há avaliações

- Eni 2003Documento192 páginasEni 2003chesco67Ainda não há avaliações

- Cement Sector MOSTDocumento12 páginasCement Sector MOSTnikhilhslAinda não há avaliações

- 10.1 A Brief Analysis of Demand and Supply of The Product For The Post Five Years and The Projected Figures For The Next Five YearsDocumento8 páginas10.1 A Brief Analysis of Demand and Supply of The Product For The Post Five Years and The Projected Figures For The Next Five Yearssaur1Ainda não há avaliações

- Indian Oil Demand Slowdown - 131226Documento5 páginasIndian Oil Demand Slowdown - 131226sabri_hazarika1200Ainda não há avaliações

- Brief Analysis of Fertilizer Industry of PakistanDocumento10 páginasBrief Analysis of Fertilizer Industry of PakistanAli ShahidAinda não há avaliações

- Lucky Cement Limited Construction and Materials Strong Pricing To Drive GrowthDocumento10 páginasLucky Cement Limited Construction and Materials Strong Pricing To Drive GrowthZiaBilalAinda não há avaliações

- Daily Agri Report September 16 2013Documento9 páginasDaily Agri Report September 16 2013Angel BrokingAinda não há avaliações

- Chemicals and Fertilisers: 2QFY17E Results PreviewDocumento8 páginasChemicals and Fertilisers: 2QFY17E Results Previewarun_algoAinda não há avaliações

- EuropeLPGReport Sample02082013Documento5 páginasEuropeLPGReport Sample02082013Melody CottonAinda não há avaliações

- Ambuja Cements Result UpdatedDocumento11 páginasAmbuja Cements Result UpdatedAngel BrokingAinda não há avaliações

- Final Report On OIL and Gas INDUSTRYDocumento18 páginasFinal Report On OIL and Gas INDUSTRYShefali SalujaAinda não há avaliações

- KSL Ongc 29jul08Documento7 páginasKSL Ongc 29jul08srinivasan9Ainda não há avaliações

- Mopng PPT 14 09 2017Documento23 páginasMopng PPT 14 09 2017Lpg SectionAinda não há avaliações

- Oil & Gas, Chemical & Telecom Sector: On Growth TrajectoryDocumento12 páginasOil & Gas, Chemical & Telecom Sector: On Growth Trajectorylalit963Ainda não há avaliações

- Final Deepak Fertilizers Petrochemicals LTDDocumento9 páginasFinal Deepak Fertilizers Petrochemicals LTDbolinjkarvinitAinda não há avaliações

- Best Performing Stock Advice For Today - Neutral Rating On GAIL Stock With A Target Price of Rs.346Documento22 páginasBest Performing Stock Advice For Today - Neutral Rating On GAIL Stock With A Target Price of Rs.346Narnolia Securities LimitedAinda não há avaliações

- Basic Statistics On Indian Petroleum & Natural GasDocumento53 páginasBasic Statistics On Indian Petroleum & Natural GasAmit GuptaAinda não há avaliações

- Foundations of Natural Gas Price Formation: Misunderstandings Jeopardizing the Future of the IndustryNo EverandFoundations of Natural Gas Price Formation: Misunderstandings Jeopardizing the Future of the IndustryAinda não há avaliações

- Advertisement No 26-2018 PDFDocumento4 páginasAdvertisement No 26-2018 PDFnaeemakhtaracmaAinda não há avaliações

- P 244 PDFDocumento6 páginasP 244 PDFZohaib PervaizAinda não há avaliações

- Advertisement No 26-2018 PDFDocumento4 páginasAdvertisement No 26-2018 PDFnaeemakhtaracmaAinda não há avaliações

- National Holidays in Pakistan For The 2017Documento3 páginasNational Holidays in Pakistan For The 2017tessAinda não há avaliações

- Pakistan Stock Market Daily KSE-100: Upside LikelyDocumento3 páginasPakistan Stock Market Daily KSE-100: Upside LikelyZohaib PervaizAinda não há avaliações

- Dairy FarmDocumento21 páginasDairy FarmZaid NaeemAinda não há avaliações

- Breeding: Dairy Hub Training Booklets TitlesDocumento8 páginasBreeding: Dairy Hub Training Booklets TitlesZohaib PervaizAinda não há avaliações

- 7-Goat Fattening Feasibility Revised 17 FebDocumento15 páginas7-Goat Fattening Feasibility Revised 17 FebZohaib PervaizAinda não há avaliações

- National Testing Service Pakistan: JST Provisional Merit List (Pass Candidates)Documento3 páginasNational Testing Service Pakistan: JST Provisional Merit List (Pass Candidates)Zohaib PervaizAinda não há avaliações

- KSE Stock ReportDocumento3 páginasKSE Stock ReportZohaib PervaizAinda não há avaliações

- Sheep Fattening Farm PDFDocumento18 páginasSheep Fattening Farm PDFZohaib PervaizAinda não há avaliações

- As 595 Commondiseases PDFDocumento12 páginasAs 595 Commondiseases PDFZohaib PervaizAinda não há avaliações

- Abdullah Ibn MasDocumento4 páginasAbdullah Ibn MasZohaib PervaizAinda não há avaliações

- Goat Fattening FarmDocumento18 páginasGoat Fattening FarmZohaib Pervaiz100% (2)

- Education Part 2 - Sample QuestionDocumento2 páginasEducation Part 2 - Sample QuestionAlamesuAinda não há avaliações

- AKD TriggerShark 24 Sep 2014Documento2 páginasAKD TriggerShark 24 Sep 2014Zohaib PervaizAinda não há avaliações

- Css Geography Repeated QuestionsDocumento6 páginasCss Geography Repeated QuestionsMuhammad Ahmer ChaudhryAinda não há avaliações

- Dairy FarmDocumento21 páginasDairy FarmZaid NaeemAinda não há avaliações

- Geography Paper 1Documento5 páginasGeography Paper 1Zohaib PervaizAinda não há avaliações

- Solar SystemDocumento6 páginasSolar SystemZohaib PervaizAinda não há avaliações

- Islamic History Subjective, Paper-II-2014Documento1 páginaIslamic History Subjective, Paper-II-2014Zohaib PervaizAinda não há avaliações

- 01 Growth and InvestmentDocumento21 páginas01 Growth and InvestmentBilal HamidAinda não há avaliações

- 14.4 Imports and ExportssDocumento1 página14.4 Imports and ExportssZohaib PervaizAinda não há avaliações

- Statistics Subject Paper-2014Documento2 páginasStatistics Subject Paper-2014Zohaib PervaizAinda não há avaliações

- Applied Mathematics Paper I & II - 2014Documento4 páginasApplied Mathematics Paper I & II - 2014Zohaib PervaizAinda não há avaliações

- Css International Relations 2014Documento1 páginaCss International Relations 2014Syedah Maira ShahAinda não há avaliações

- CSS Essay 2014Documento1 páginaCSS Essay 2014Engr Hafiz UmairAinda não há avaliações

- Countries Capital, Language, CurrencyDocumento6 páginasCountries Capital, Language, CurrencyZohaib PervaizAinda não há avaliações

- 1 TauheedDocumento3 páginas1 TauheedZohaib PervaizAinda não há avaliações

- Project Presentation (142311004) FinalDocumento60 páginasProject Presentation (142311004) FinalSaad AhammadAinda não há avaliações

- A Study of Cognitive Human Factors in Mascot DesignDocumento16 páginasA Study of Cognitive Human Factors in Mascot DesignAhmadAinda não há avaliações

- Bikini Body: Eating GuideDocumento12 páginasBikini Body: Eating GuideAdela M BudAinda não há avaliações

- Ingo Plag Et AlDocumento7 páginasIngo Plag Et AlDinha GorgisAinda não há avaliações

- PLM V6R2011x System RequirementsDocumento46 páginasPLM V6R2011x System RequirementsAnthonio MJAinda não há avaliações

- New Norms of Upper Limb Fat and Muscle Areas For Assessment of Nutritional StatusDocumento6 páginasNew Norms of Upper Limb Fat and Muscle Areas For Assessment of Nutritional StatusDani Bah ViAinda não há avaliações

- 4-String Cigar Box Guitar Chord Book (Brent Robitaille) (Z-Library)Documento172 páginas4-String Cigar Box Guitar Chord Book (Brent Robitaille) (Z-Library)gregory berlemontAinda não há avaliações

- Education-and-Life-in-Europe - Life and Works of RizalDocumento3 páginasEducation-and-Life-in-Europe - Life and Works of Rizal202202345Ainda não há avaliações

- Lista Destinatari Tema IDocumento4 páginasLista Destinatari Tema INicola IlieAinda não há avaliações

- Business Communication EnglishDocumento191 páginasBusiness Communication EnglishkamaleshvaranAinda não há avaliações

- The Apollo Parachute Landing SystemDocumento28 páginasThe Apollo Parachute Landing SystemBob Andrepont100% (2)

- Assessment Guidelines For Processing Operations Hydrocarbons VQDocumento47 páginasAssessment Guidelines For Processing Operations Hydrocarbons VQMatthewAinda não há avaliações

- F4-Geography Pre-Mock Exam 18.08.2021Documento6 páginasF4-Geography Pre-Mock Exam 18.08.2021JOHNAinda não há avaliações

- English8 q1 Mod5 Emotive Words v1Documento21 páginasEnglish8 q1 Mod5 Emotive Words v1Jimson GastaAinda não há avaliações

- Drimaren - Dark - Blue HF-CDDocumento17 páginasDrimaren - Dark - Blue HF-CDrajasajjad0% (1)

- Elevex ENDocumento4 páginasElevex ENMirko Mejias SotoAinda não há avaliações

- Intel Corporation Analysis: Strategical Management - Tengiz TaktakishviliDocumento12 páginasIntel Corporation Analysis: Strategical Management - Tengiz TaktakishviliSandro ChanturidzeAinda não há avaliações

- Member, National Gender Resource Pool Philippine Commission On WomenDocumento66 páginasMember, National Gender Resource Pool Philippine Commission On WomenMonika LangngagAinda não há avaliações

- Hallux Valgus SXDocumento569 páginasHallux Valgus SXandi100% (2)

- Palma vs. Fortich PDFDocumento3 páginasPalma vs. Fortich PDFKristine VillanuevaAinda não há avaliações

- MAraguinot V Viva Films DigestDocumento2 páginasMAraguinot V Viva Films DigestcattaczAinda não há avaliações

- Chapter 4Documento20 páginasChapter 4Alyssa Grace CamposAinda não há avaliações

- Highway MidtermsDocumento108 páginasHighway MidtermsAnghelo AlyenaAinda não há avaliações

- SSoA Resilience Proceedings 27mbDocumento704 páginasSSoA Resilience Proceedings 27mbdon_h_manzano100% (1)

- MANILA HOTEL CORP. vs. NLRCDocumento5 páginasMANILA HOTEL CORP. vs. NLRCHilary MostajoAinda não há avaliações

- Art CriticismDocumento3 páginasArt CriticismVallerie ServanoAinda não há avaliações

- WHO SOPs Terms DefinitionsDocumento3 páginasWHO SOPs Terms DefinitionsNaseem AkhtarAinda não há avaliações

- I Wanted To Fly Like A ButterflyDocumento12 páginasI Wanted To Fly Like A ButterflyJorge VazquezAinda não há avaliações

- Thesis ClarinetDocumento8 páginasThesis Clarinetmeganjoneshuntsville100% (2)

- SSD Term 3Documento52 páginasSSD Term 3anne_barltropAinda não há avaliações