Você também pode gostar

- The Science Behind Reading Genius - 3-10-06Documento35 páginasThe Science Behind Reading Genius - 3-10-06Deanna Jones100% (10)

- Stata Excel SpreadsheetDocumento43 páginasStata Excel SpreadsheetAliAinda não há avaliações

- AP Microeconomics TestDocumento13 páginasAP Microeconomics TestGriffin Greco100% (1)

- 4 CF PresentDocumento20 páginas4 CF PresentFaisal AfzalAinda não há avaliações

- An AnalysisDocumento33 páginasAn AnalysisDonales Alnur100% (1)

- KotlerDocumento9 páginasKotlerGitanjali BaggaAinda não há avaliações

- PILMICO v. CIRDocumento2 páginasPILMICO v. CIRPat EspinozaAinda não há avaliações

- A Literature Review and A Case Study of Sustainable Supply Chians With A Focus On MetricsDocumento14 páginasA Literature Review and A Case Study of Sustainable Supply Chians With A Focus On MetricsKarthikkumar Baskaran100% (1)

- Master Services Agreement: Appen Butler Hill Pty, LTDDocumento14 páginasMaster Services Agreement: Appen Butler Hill Pty, LTDHappy manansalaAinda não há avaliações

- Economics of Strategy: Sixth EditionDocumento63 páginasEconomics of Strategy: Sixth EditionRichardNicoArdyantoAinda não há avaliações

- Case 3 OasisDocumento17 páginasCase 3 OasisGinanjarSaputraAinda não há avaliações

- GBE SukamartDocumento25 páginasGBE SukamartDwitya AribawaAinda não há avaliações

- First Do No Harm Mar 2012 Tcm9-106817Documento31 páginasFirst Do No Harm Mar 2012 Tcm9-106817nazAinda não há avaliações

- The Walt Disney Company: Its Diversification Strategy in 2012Documento19 páginasThe Walt Disney Company: Its Diversification Strategy in 2012Hesty SaniaAinda não há avaliações

- Lamudi - White Paper 2015 PresentationDocumento19 páginasLamudi - White Paper 2015 PresentationRobert 'Bob' ReyesAinda não há avaliações

- Business Strategy and Enterprise: Chapter 6: Corporate Level StrategyDocumento5 páginasBusiness Strategy and Enterprise: Chapter 6: Corporate Level StrategyageAinda não há avaliações

- Ikea Group Yearly Summary Fy14Documento43 páginasIkea Group Yearly Summary Fy14ArraAinda não há avaliações

- (MM5012) 29111328 Individual Assignment EditDocumento6 páginas(MM5012) 29111328 Individual Assignment EdithendrawinataAinda não há avaliações

- Porter Five Forces AnalysisDocumento6 páginasPorter Five Forces Analysisnaseeb_kakar_3Ainda não há avaliações

- Business and Initiatives Update 1st Feb 2021 - Key Highlights, Store Closures, Covid ResponseDocumento13 páginasBusiness and Initiatives Update 1st Feb 2021 - Key Highlights, Store Closures, Covid ResponseDaniel PradityaAinda não há avaliações

- SlaytonDocumento3 páginasSlaytonTubagus FadillahAinda não há avaliações

- Financial Detective CaseDocumento11 páginasFinancial Detective CaseHenni RahmanAinda não há avaliações

- Analyzing Cash Flow Projects and Capital Budgeting DecisionsDocumento3 páginasAnalyzing Cash Flow Projects and Capital Budgeting DecisionsAlthea LandichoAinda não há avaliações

- Strategic Management 9 Pepsi CoDocumento3 páginasStrategic Management 9 Pepsi CoFauzan Al AsyiqAinda não há avaliações

- Contoh Five Forces AnalysisDocumento17 páginasContoh Five Forces AnalysisChaeMJAinda não há avaliações

- Syndicate 1 Nike Cost of Capital FinalDocumento2 páginasSyndicate 1 Nike Cost of Capital FinalirfanmuafiAinda não há avaliações

- IPO Listings: Why Some Choose Nasdaq Over NYSEDocumento22 páginasIPO Listings: Why Some Choose Nasdaq Over NYSEMikkoAinda não há avaliações

- Attitude Change Strategy - Syndicate 4Documento7 páginasAttitude Change Strategy - Syndicate 4Busyairi Alfan RamadhanAinda não há avaliações

- Ayustinagiusti - Developing Financial Insights - Using A Future Value (FV) and A Present Value (PV) ApproachDocumento10 páginasAyustinagiusti - Developing Financial Insights - Using A Future Value (FV) and A Present Value (PV) ApproachAyustina GiustiAinda não há avaliações

- Political Risk: Prof Mahesh Kumar Amity Business SchoolDocumento41 páginasPolitical Risk: Prof Mahesh Kumar Amity Business SchoolasifanisAinda não há avaliações

- Aligning People Strategies With Customer Value31Documento8 páginasAligning People Strategies With Customer Value31Zafrid HussainAinda não há avaliações

- Portfolio Analysis Tools for Strategic Decision MakingDocumento19 páginasPortfolio Analysis Tools for Strategic Decision MakingReshma GoudaAinda não há avaliações

- Analysis of The Effect of Financial Ratio On Stock Returns of Non Cyclicals Consumer Companies Listed On IDX 2015-2020Documento11 páginasAnalysis of The Effect of Financial Ratio On Stock Returns of Non Cyclicals Consumer Companies Listed On IDX 2015-2020International Journal of Innovative Science and Research TechnologyAinda não há avaliações

- Capital Structure and LeverageDocumento23 páginasCapital Structure and Leveragequeen montanoAinda não há avaliações

- Tugas Manajemen Operasi Stroller Case Kelompok 1 PDFDocumento4 páginasTugas Manajemen Operasi Stroller Case Kelompok 1 PDFDwi Permana100% (1)

- Paper Economics For Business by Group 2 MMB28BDocumento15 páginasPaper Economics For Business by Group 2 MMB28BLesmanaBotaxxIndraAinda não há avaliações

- Star Alliance A Global NetworkDocumento6 páginasStar Alliance A Global NetworkSwati NimjeAinda não há avaliações

- Siemens: Building A Structure To Drive Performance and Responsibility - CaseDocumento6 páginasSiemens: Building A Structure To Drive Performance and Responsibility - CaseBitopan SonowalAinda não há avaliações

- Case 8 PaperDocumento6 páginasCase 8 PaperKarina Permata Sari33% (3)

- 2013 - SULI - SULI - Annual Report - 2013 PDFDocumento46 páginas2013 - SULI - SULI - Annual Report - 2013 PDFulfadwimustika0% (1)

- Determinant of ROE, CR, EPS, DER, PBV On Share Price On Mining Sector Companies Registered in IDX in 2014 - 2017Documento7 páginasDeterminant of ROE, CR, EPS, DER, PBV On Share Price On Mining Sector Companies Registered in IDX in 2014 - 2017Anonymous izrFWiQAinda não há avaliações

- Summary Chapter 7 Overcome Key Organizational HurdlesDocumento4 páginasSummary Chapter 7 Overcome Key Organizational Hurdlesabd.mirza2627Ainda não há avaliações

- Corporate Strategy DiversificationDocumento24 páginasCorporate Strategy Diversificationharum77Ainda não há avaliações

- Quietly Brilliant HTCDocumento2 páginasQuietly Brilliant HTCOxky Setiawan WibisonoAinda não há avaliações

- Information Search and Analysis Skills (ISAS)Documento22 páginasInformation Search and Analysis Skills (ISAS)Izzuddin HananAinda não há avaliações

- Corporate Foresight in Multinational Business StrategiesDocumento15 páginasCorporate Foresight in Multinational Business StrategiesAladdin PrinceAinda não há avaliações

- Astra Sustainability Report Using GRI StandardsDocumento7 páginasAstra Sustainability Report Using GRI StandardsratihAinda não há avaliações

- Competitive AdvantageDocumento90 páginasCompetitive AdvantageEldhoAinda não há avaliações

- Cattani & Mabert Supply Chain Design Past Present and Future PDFDocumento12 páginasCattani & Mabert Supply Chain Design Past Present and Future PDFrahadimetaAinda não há avaliações

- Indofood CBP Sukses Makmur: Assessing The New Potential Sales DriverDocumento9 páginasIndofood CBP Sukses Makmur: Assessing The New Potential Sales DriverRizqi HarryAinda não há avaliações

- Case 2 S 1 Apple The Iphone Turns 10 PDFDocumento20 páginasCase 2 S 1 Apple The Iphone Turns 10 PDFMifta ZanariaAinda não há avaliações

- Mid Exam BSEM - SMEMBA 3 - 29318436 - Armita OctafianyDocumento6 páginasMid Exam BSEM - SMEMBA 3 - 29318436 - Armita Octafianyarmita octafianyAinda não há avaliações

- Chap 008Documento26 páginasChap 008Citra Dewi WulansariAinda não há avaliações

- wk2 SophiaDocumento7 páginaswk2 SophiaJong ChaAinda não há avaliações

- Basic Decision TreeDocumento48 páginasBasic Decision TreeFara PratiwiAinda não há avaliações

- Case Valuation PT Semen Gresik - CemexDocumento7 páginasCase Valuation PT Semen Gresik - CemexsyifanoeAinda não há avaliações

- #10. IS Similarity - Post MADocumento15 páginas#10. IS Similarity - Post MAdewimachfudAinda não há avaliações

- Primus AutomationDocumento26 páginasPrimus AutomationdewimachfudAinda não há avaliações

- Automotive Industry in The Context of Industry 40Documento5 páginasAutomotive Industry in The Context of Industry 40Nurul Aisyah Binti RamlanAinda não há avaliações

- Risk Analysis in Capital BudgetingDocumento23 páginasRisk Analysis in Capital BudgetingAbhilash MeruvaAinda não há avaliações

- Restructure or ReconfigureDocumento5 páginasRestructure or ReconfigureaniAinda não há avaliações

- Plaza Indonesia AR 2011 FINALDocumento172 páginasPlaza Indonesia AR 2011 FINALHiroshi Gozali MasehiAinda não há avaliações

- Financial Performance Analysis of Bumn Companyon Airline Industry (Pt. Garuda TBK) and Pharmaceutical Industry (Pt. Kimia Farma TBK) in IndonesiaDocumento14 páginasFinancial Performance Analysis of Bumn Companyon Airline Industry (Pt. Garuda TBK) and Pharmaceutical Industry (Pt. Kimia Farma TBK) in IndonesiaRaisha FaziyaAinda não há avaliações

- Capital Structure Decision - Written ReportDocumento9 páginasCapital Structure Decision - Written ReportEuniceBrillanteAinda não há avaliações

- FM - Chapter 15Documento8 páginasFM - Chapter 15Rahul ShrivastavaAinda não há avaliações

- Merger and Acquisition BasicDocumento19 páginasMerger and Acquisition BasicAliAinda não há avaliações

- 22-English-eLong Inc-2010 PDFDocumento237 páginas22-English-eLong Inc-2010 PDFAliAinda não há avaliações

- Holdings Ltd-2013Documento101 páginasHoldings Ltd-2013AliAinda não há avaliações

- STOXX Global ESG Leaders Index Price HistoryDocumento117 páginasSTOXX Global ESG Leaders Index Price HistoryAliAinda não há avaliações

- Getting Started with Bankscope DatasetDocumento43 páginasGetting Started with Bankscope DatasetAliAinda não há avaliações

- Setting Up Mendeley To Sync To Android DeviceDocumento5 páginasSetting Up Mendeley To Sync To Android DeviceAliAinda não há avaliações

- Migration and Development Brief 22Documento31 páginasMigration and Development Brief 22AliAinda não há avaliações

- Dividend Policy Literature ReviewDocumento11 páginasDividend Policy Literature ReviewAli100% (1)

- Eviews Tutorial 4 1Documento25 páginasEviews Tutorial 4 1AliAinda não há avaliações

- Introduction To FinanceDocumento6 páginasIntroduction To FinancesaadalamAinda não há avaliações

- FMS 2008 SolvedDocumento21 páginasFMS 2008 SolvedSiddhartha Shankar NayakAinda não há avaliações

- Unlock Research Proposal FormatDocumento21 páginasUnlock Research Proposal FormatAliAinda não há avaliações

- Assignments of Corporate FinanceDocumento21 páginasAssignments of Corporate FinanceAli0% (2)

- Management Sciences Core Areas BreakdownDocumento5 páginasManagement Sciences Core Areas BreakdownAliAinda não há avaliações

- Economics Syllabus GATDocumento5 páginasEconomics Syllabus GATAliAinda não há avaliações

- Writing and Presenting Your Thesis or DissertationDocumento14 páginasWriting and Presenting Your Thesis or DissertationDenkenAinda não há avaliações

- Note FormulaeDocumento4 páginasNote FormulaeKaran N ShahAinda não há avaliações

- 43 43 Technical QuestionsDocumento3 páginas43 43 Technical QuestionsjayakrishnankprakashAinda não há avaliações

- Addictive DrugDocumento3 páginasAddictive DrugAliAinda não há avaliações

- Assignments of Corporate FinanceDocumento21 páginasAssignments of Corporate FinanceAli0% (2)

- Critical Review AtriclesDocumento19 páginasCritical Review AtriclesAliAinda não há avaliações

- Topics For PreparationDocumento23 páginasTopics For PreparationdwivedidilipAinda não há avaliações

- Casechart ComparisonDocumento1 páginaCasechart ComparisonAliAinda não há avaliações

- Dissertation TemplateDocumento33 páginasDissertation TemplateAliAinda não há avaliações

- Business Ethics - PakistanDocumento27 páginasBusiness Ethics - PakistanAliAinda não há avaliações

- WACCDocumento18 páginasWACCAliAinda não há avaliações

- BooksDocumento1 páginaBooksAliAinda não há avaliações

- BIR Ruling 097-11Documento4 páginasBIR Ruling 097-11Jobi BryantAinda não há avaliações

- Sulaimanov RuslanDocumento71 páginasSulaimanov RuslanAries SatriaAinda não há avaliações

- STD 8th Perfect History and Civics Notes English Medium MH BoardDocumento12 páginasSTD 8th Perfect History and Civics Notes English Medium MH BoardSam Pathan0% (1)

- Which of The Following Is The Correct Tax Implication of The Foregoing Data With Respect To Payment of Income Tax?Documento3 páginasWhich of The Following Is The Correct Tax Implication of The Foregoing Data With Respect To Payment of Income Tax?ROSEMARIE CRUZAinda não há avaliações

- US Internal Revenue Service: f8839 - 2004Documento2 páginasUS Internal Revenue Service: f8839 - 2004IRSAinda não há avaliações

- Print 1stDocumento1 páginaPrint 1stChristine Marie RamirezAinda não há avaliações

- A Foreign Investor's Guide to Tunisia OpportunitiesDocumento101 páginasA Foreign Investor's Guide to Tunisia OpportunitiesMatthew BennettAinda não há avaliações

- Scottish IndependenceDocumento128 páginasScottish IndependenceScottishIndependence100% (2)

- Dispatch Export DocumentsDocumento120 páginasDispatch Export DocumentsEdliraShehuAinda não há avaliações

- 2021 Tax Rates SwitzerlandDocumento4 páginas2021 Tax Rates SwitzerlandKamil JanasAinda não há avaliações

- Villanueva V City of IloiloDocumento1 páginaVillanueva V City of IloilorobbyAinda não há avaliações

- 221 Figuerres v. CADocumento14 páginas221 Figuerres v. CAJai HoAinda não há avaliações

- KRSE - B - 15-20HP-115PSI-230V - 20HP-115PSI-460V-SKK55 Parts Manual - 97002015000020BDocumento41 páginasKRSE - B - 15-20HP-115PSI-230V - 20HP-115PSI-460V-SKK55 Parts Manual - 97002015000020BRogelio MirelesAinda não há avaliações

- Alberto VegaDocumento1 páginaAlberto Vegaflordeliz12Ainda não há avaliações

- PTI Proposed Amended Constitution 2014Documento62 páginasPTI Proposed Amended Constitution 2014PTI OfficialAinda não há avaliações

- COM670 Chapter 4Documento28 páginasCOM670 Chapter 4aakapsAinda não há avaliações

- GST Past Exam AnalysisDocumento17 páginasGST Past Exam AnalysisSuraj PawarAinda não há avaliações

- Assessment ProcedureDocumento8 páginasAssessment ProcedureAbhishek SharmaAinda não há avaliações

- PPM223 Me-10299Documento3 páginasPPM223 Me-10299Rob PortAinda não há avaliações

- IntermediateDocumento139 páginasIntermediateabdulramani mbwanaAinda não há avaliações

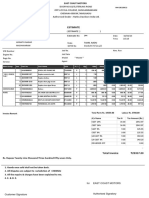

- Job Est PrintDocumento1 páginaJob Est PrintKashish JainAinda não há avaliações

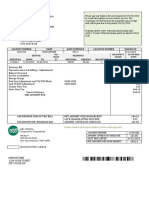

- C - L ElectricDocumento1 páginaC - L ElectricNoel FrömgenAinda não há avaliações

- Turkish Political Economy: 1923 - 1939: INTL 410 / ECIR 410 Prof. Ziya ÖnişDocumento15 páginasTurkish Political Economy: 1923 - 1939: INTL 410 / ECIR 410 Prof. Ziya ÖnişEce ErdoğanAinda não há avaliações

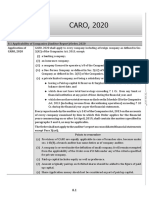

- Caro 2020 Main Book Pankaj GargDocumento23 páginasCaro 2020 Main Book Pankaj Gargajay adhikariAinda não há avaliações

- Tanzania Revenue Authority's Direct Tax Laws on Determining Year of IncomeDocumento64 páginasTanzania Revenue Authority's Direct Tax Laws on Determining Year of IncomeBISEKOAinda não há avaliações

- Palawan Pawnshop - Palawan Express Pera Padala: Net PayDocumento1 páginaPalawan Pawnshop - Palawan Express Pera Padala: Net PayRemart DultraAinda não há avaliações

- Group 2 Fiscal Policy Assignment 2Documento16 páginasGroup 2 Fiscal Policy Assignment 2NGHIÊM NGUYỄN MINH100% (1)