Você também pode gostar

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

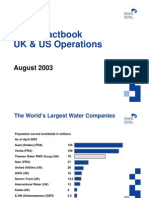

- WS Refe 20161128173914 TSL1PROD 32680Documento557 páginasWS Refe 20161128173914 TSL1PROD 32680josepmcdalena6542Ainda não há avaliações

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Seven WondersDocumento14 páginasSeven Wondersjosepmcdalena6542Ainda não há avaliações

- Unlocking The Energy Efficiency Opportunity Main Report .75081.shortcutDocumento89 páginasUnlocking The Energy Efficiency Opportunity Main Report .75081.shortcutjosepmcdalena6542Ainda não há avaliações

- Basic ShapesDocumento12 páginasBasic Shapesjosepmcdalena6542Ainda não há avaliações

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- US Energy Efficiency Full ReportDocumento165 páginasUS Energy Efficiency Full Reportjosepmcdalena6542Ainda não há avaliações

- The Best of Charlie Munger 1994 2011Documento349 páginasThe Best of Charlie Munger 1994 2011VALUEWALK LLC100% (6)

- Japanese VerbsDocumento8 páginasJapanese Verbsjosepmcdalena6542Ainda não há avaliações

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Disruptive Technologies McKinsey May 2013Documento176 páginasDisruptive Technologies McKinsey May 2013mattb411Ainda não há avaliações

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Arduino Booklet PDFDocumento45 páginasArduino Booklet PDFgpt1708Ainda não há avaliações

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- Mercado Del AguaDocumento27 páginasMercado Del Aguajosepmcdalena6542Ainda não há avaliações

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Tilson Funds Annual Report 2005Documento28 páginasTilson Funds Annual Report 2005josepmcdalena6542Ainda não há avaliações

- Forward Contract Vs Futures ContractDocumento4 páginasForward Contract Vs Futures ContractabdulwadoodansariAinda não há avaliações

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Impacts of Oil Price and Exchange Rate On Vietnamese Stock MarketDocumento8 páginasThe Impacts of Oil Price and Exchange Rate On Vietnamese Stock MarketSATYAM MISHRAAinda não há avaliações

- Interest Rates and Bond Valuation Chapter 6Documento29 páginasInterest Rates and Bond Valuation Chapter 6Mariana MuñozAinda não há avaliações

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- FIN352 - Review Questions For Midterm Exam 1Documento6 páginasFIN352 - Review Questions For Midterm Exam 1Samantha IslamAinda não há avaliações

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- DCI Blog - How DCI Will Tokenize Your Company Assets Into DigitalDocumento2 páginasDCI Blog - How DCI Will Tokenize Your Company Assets Into DigitalGaurav SAGAinda não há avaliações

- MKTG 6223Documento11 páginasMKTG 6223Ann LysterAinda não há avaliações

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- FINA 4319 Syllabus Spring 2021-NDocumento6 páginasFINA 4319 Syllabus Spring 2021-NAnh NguyenAinda não há avaliações

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Risk Management (P3) : Forex - 01Documento21 páginasRisk Management (P3) : Forex - 01moody84Ainda não há avaliações

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Trade LifecycleDocumento2 páginasTrade LifecycleSaurabhAinda não há avaliações

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Nomura - Tata MotorsDocumento5 páginasNomura - Tata MotorsAshish GuptaAinda não há avaliações

- 694 Idbi StatementDocumento26 páginas694 Idbi StatementAyn RockyAinda não há avaliações

- Introduction To Investment BankingDocumento27 páginasIntroduction To Investment Bankingpriya_1234563236967% (6)

- Chapter 11Documento38 páginasChapter 11Affira AfriAinda não há avaliações

- AMAZON Insider TradingDocumento9 páginasAMAZON Insider TradingZerohedgeAinda não há avaliações

- Ab 3Documento2 páginasAb 3sanpoung809Ainda não há avaliações

- Guidance Note On Derivative AccountingDocumento9 páginasGuidance Note On Derivative AccountingHimanshu AggarwalAinda não há avaliações

- CA Devendra Jain Sec 56 9-6-2018Documento46 páginasCA Devendra Jain Sec 56 9-6-2018ShabarishAinda não há avaliações

- JPM 2010 Annual ReviewDocumento300 páginasJPM 2010 Annual ReviewMatt CareyAinda não há avaliações

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Trading Plan Harian - Binary OptionsDocumento6 páginasTrading Plan Harian - Binary OptionsFarhan AlthafAinda não há avaliações

- PriceDocumento4 páginasPriceBel KisAinda não há avaliações

- Letter of TransmittalDocumento7 páginasLetter of TransmittalK. J. M. Rezaur RahmanAinda não há avaliações

- Module 1 Business Finance Quarter 3 Module 12 Introduction To Financial ManagementDocumento24 páginasModule 1 Business Finance Quarter 3 Module 12 Introduction To Financial ManagementClird Ford CastilloAinda não há avaliações

- Checklist For DematerialisationDocumento2 páginasChecklist For Dematerialisationsneha hegdeAinda não há avaliações

- SV - Topic 2. Cong Cu Tai ChinhDocumento56 páginasSV - Topic 2. Cong Cu Tai ChinhPhương DiAinda não há avaliações

- Export Value DeclarationDocumento1 páginaExport Value DeclarationdocrmpjodAinda não há avaliações

- Tsaasf Practice ExamDocumento11 páginasTsaasf Practice ExamRajeshbhai vaghaniAinda não há avaliações

- Madura ch4 TBDocumento11 páginasMadura ch4 TBSameh Ahmed Hassan80% (5)

- MFM Chap-01Documento17 páginasMFM Chap-01VEDANT XAinda não há avaliações

- MGT201 Short NotesDocumento14 páginasMGT201 Short NotesShahid SaeedAinda não há avaliações

- Period Close Exception ReportDocumento11 páginasPeriod Close Exception ReportKumarAinda não há avaliações