Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (120)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- "Financial Statement": Lovely Professional UniversityDocumento87 páginas"Financial Statement": Lovely Professional UniversityBHARATAinda não há avaliações

- Proof of AddressDocumento9 páginasProof of AddressATIF ALIAinda não há avaliações

- ProjectDocumento17 páginasProjectBHARATAinda não há avaliações

- Project Report ON "Customer Satisfaction Regarding HDFC Bank"Documento63 páginasProject Report ON "Customer Satisfaction Regarding HDFC Bank"BHARATAinda não há avaliações

- Final Project SamsungDocumento45 páginasFinal Project SamsungBHARATAinda não há avaliações

- Your Account NotesDocumento30 páginasYour Account NotesBHARATAinda não há avaliações

- Final Project SamsungDocumento48 páginasFinal Project SamsungBHARATAinda não há avaliações

- Century PietDocumento59 páginasCentury PietBHARATAinda não há avaliações

- A Project Report: Submitted in The Partial Fulfillment For The Award ofDocumento57 páginasA Project Report: Submitted in The Partial Fulfillment For The Award ofBHARATAinda não há avaliações

- HCLDocumento15 páginasHCLBHARATAinda não há avaliações

- A Lecture Upon The ShadowDocumento1 páginaA Lecture Upon The ShadowBHARATAinda não há avaliações

- Equity Analysis NumberDocumento59 páginasEquity Analysis NumberBHARATAinda não há avaliações

- Executive SummaryDocumento15 páginasExecutive SummaryBHARATAinda não há avaliações

- Final Project SamsungDocumento53 páginasFinal Project SamsungBHARATAinda não há avaliações

- IDBI Project PDFDocumento47 páginasIDBI Project PDFBHARATAinda não há avaliações

- AmulDocumento101 páginasAmulBHARATAinda não há avaliações

- Limitations of The Study Conclusions & Suggestions BibliographyDocumento43 páginasLimitations of The Study Conclusions & Suggestions BibliographyBHARATAinda não há avaliações

- Summer Project Shubham PNBDocumento60 páginasSummer Project Shubham PNBBHARATAinda não há avaliações

- Table of Contents:: NO. NO. 1Documento61 páginasTable of Contents:: NO. NO. 1BHARATAinda não há avaliações

- Liberty ProjectDocumento73 páginasLiberty ProjectBHARATAinda não há avaliações

- Industry Profile: Overview of The Footwear Industrial SectorDocumento68 páginasIndustry Profile: Overview of The Footwear Industrial SectorBHARATAinda não há avaliações

- ProjectDocumento71 páginasProjectBHARATAinda não há avaliações

- Final ReportDocumento74 páginasFinal ReportBHARATAinda não há avaliações

- Final ProjectDocumento61 páginasFinal ProjectBHARATAinda não há avaliações

- Liberty Project2Documento75 páginasLiberty Project2BHARATAinda não há avaliações

- Final ReportDocumento72 páginasFinal ReportBHARATAinda não há avaliações

- Axis Bank Project ReportDocumento63 páginasAxis Bank Project ReportBHARATAinda não há avaliações

- Arya (P.G) College, Panipat: Training ReportDocumento34 páginasArya (P.G) College, Panipat: Training ReportBHARATAinda não há avaliações

- Final ProjectDocumento74 páginasFinal ProjectBHARATAinda não há avaliações

- Chapter No. Names of Chapters 1.: Introduction To Hero CycleDocumento63 páginasChapter No. Names of Chapters 1.: Introduction To Hero CycleBHARATAinda não há avaliações

- Final ReportDocumento63 páginasFinal ReportBHARATAinda não há avaliações

- Human Rights Defense Center v. MCCA Self-Funded Risk Management PoolDocumento18 páginasHuman Rights Defense Center v. MCCA Self-Funded Risk Management PoolMaine Trust For Local NewsAinda não há avaliações

- Analysis of Bailout Funding - 19012008Documento14 páginasAnalysis of Bailout Funding - 19012008ep heidner100% (6)

- Bankdirectorysap v1 SampleDocumento48 páginasBankdirectorysap v1 Sampleshinerulz100% (1)

- CRMDocumento25 páginasCRMAlana PetersonAinda não há avaliações

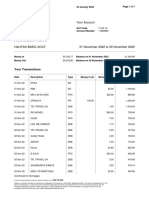

- 2023 11 11 16 29 12 Statement - 1699680552067Documento7 páginas2023 11 11 16 29 12 Statement - 1699680552067roshansm1978Ainda não há avaliações

- Logistics Tech Investor Landscape - 2024Documento1.664 páginasLogistics Tech Investor Landscape - 2024Nitin VarmanAinda não há avaliações

- InternshipDocumento2 páginasInternshipChelsi Christine TenorioAinda não há avaliações

- Rep 1011033305 1Documento421 páginasRep 1011033305 1Miles Mertens0% (1)

- Public Sector BanksDocumento2 páginasPublic Sector BanksRUBY DIANAAinda não há avaliações

- Series PoDocumento35 páginasSeries PoAishwaryaAyrawhsiaKohliAinda não há avaliações

- Nov Pay PDFDocumento7 páginasNov Pay PDFRoland Lovelace OpokuAinda não há avaliações

- Functioning OF Unit Trust of IndiaDocumento23 páginasFunctioning OF Unit Trust of IndiaRohit MalviyaAinda não há avaliações

- Ipo of Alibaba: One of The Most Mysterious Ipos in The Tech IndustryDocumento16 páginasIpo of Alibaba: One of The Most Mysterious Ipos in The Tech IndustryAshish VermaAinda não há avaliações

- Isc Report1c 1314Documento33 páginasIsc Report1c 1314Rajanna JadiAinda não há avaliações

- List of Accredited Collection Agency As of October 2021Documento3 páginasList of Accredited Collection Agency As of October 2021DODJIE DIMACULANGANAinda não há avaliações

- MJL Bangladesh Limited: Bank Code Br. Code Bank & Branch NameDocumento9 páginasMJL Bangladesh Limited: Bank Code Br. Code Bank & Branch Namectgdesired7106Ainda não há avaliações

- The Karur Vysya Bank LimitedDocumento11 páginasThe Karur Vysya Bank LimitedmithradharunAinda não há avaliações

- List+No 347+update+Available+BGs, MTNS, CDs+&+BONDsDocumento15 páginasList+No 347+update+Available+BGs, MTNS, CDs+&+BONDsJuan Pablo ArangoAinda não há avaliações

- Usa SetupDocumento174 páginasUsa SetupTounsi HurrAinda não há avaliações

- Finance Team 2020-2021Documento465 páginasFinance Team 2020-2021DIVYANSHU SHEKHARAinda não há avaliações

- Project Report - The Saraswat Co-Op Bank LTD - by Pahal SatvilkarDocumento6 páginasProject Report - The Saraswat Co-Op Bank LTD - by Pahal SatvilkarPRALHADAinda não há avaliações

- Monthly Unicorn Report - Jan 2021Documento95 páginasMonthly Unicorn Report - Jan 2021Tulasi Ram BoddetiAinda não há avaliações

- Life Insurance Scenario in IndiaDocumento41 páginasLife Insurance Scenario in IndiaPraveen ChaturvediAinda não há avaliações

- Elite ResignationsDocumento133 páginasElite ResignationsPlanet Awakening100% (1)

- Your Bank Statement Is Ready 2Documento53 páginasYour Bank Statement Is Ready 2mariakylie99Ainda não há avaliações

- Recent General Knowledge On Bangladesh & World Economy PDFDocumento49 páginasRecent General Knowledge On Bangladesh & World Economy PDFarifAinda não há avaliações

- Oriental Mba Front Pagesand ProjectDocumento102 páginasOriental Mba Front Pagesand ProjectNAVEEN ROYAinda não há avaliações

- W AsiaDocumento6 páginasW Asiaapi-213954485Ainda não há avaliações

- BRAC Bank Statement 01082023Documento15 páginasBRAC Bank Statement 01082023freelancer.siddikAinda não há avaliações