Você também pode gostar

- 6th Central Pay Commission Salary CalculatorDocumento15 páginas6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Bain Report India Venture Capital 2021Documento46 páginasBain Report India Venture Capital 2021Ansuka SahuAinda não há avaliações

- Nacpil v. IBC (GR 144767) Case DigestDocumento2 páginasNacpil v. IBC (GR 144767) Case DigestEricha Joy GonadanAinda não há avaliações

- PPP GuidelinesDocumento59 páginasPPP GuidelinesyonportesAinda não há avaliações

- New Commercial Company Law in Uae PDFDocumento7 páginasNew Commercial Company Law in Uae PDFAli AdnanAinda não há avaliações

- Money Flow IndexDocumento8 páginasMoney Flow IndexShahzad DalalAinda não há avaliações

- Budgeting in The PhilippinesDocumento22 páginasBudgeting in The PhilippinesBernice Purugganan AresAinda não há avaliações

- Gonzales vs. PNB (G.R. No. L-33320) CASE DIGESTDocumento2 páginasGonzales vs. PNB (G.R. No. L-33320) CASE DIGESTEricha Joy GonadanAinda não há avaliações

- Ethiopia's Growth and Transformation Plan (GTP) 2010/11-2014/15Documento85 páginasEthiopia's Growth and Transformation Plan (GTP) 2010/11-2014/15David BockAinda não há avaliações

- Financial Management Module PDFDocumento218 páginasFinancial Management Module PDFsoontheracesun100% (2)

- Philippine Development Issues and Problems ReflectionDocumento3 páginasPhilippine Development Issues and Problems ReflectionMichelle Baguio100% (1)

- Partition of Family Home DisputeDocumento1 páginaPartition of Family Home DisputeEricha Joy GonadanAinda não há avaliações

- Collins TCPA Fee ContestDocumento229 páginasCollins TCPA Fee ContestDaniel FisherAinda não há avaliações

- Raaaa A A AaaaaaaaaaaaaaaaaaaaaaaaaaDocumento140 páginasRaaaa A A Aaaaaaaaaaaaaaaaaaaaaaaaaajay4nothingAinda não há avaliações

- Philippines 2010 Progress Report On The Millenium Development GoalsDocumento292 páginasPhilippines 2010 Progress Report On The Millenium Development GoalsThe Outer Marker100% (2)

- Gonadan - Lao v. CADocumento2 páginasGonadan - Lao v. CAEricha Joy GonadanAinda não há avaliações

- Y-I Leisure held jointly liable for MADCI debtDocumento10 páginasY-I Leisure held jointly liable for MADCI debtEricha Joy GonadanAinda não há avaliações

- Y-I Leisure held jointly liable for MADCI debtDocumento10 páginasY-I Leisure held jointly liable for MADCI debtEricha Joy GonadanAinda não há avaliações

- Contract To SellDocumento2 páginasContract To SellPaolo Gabriel Sid Decena100% (2)

- Contract To SellDocumento2 páginasContract To SellPaolo Gabriel Sid Decena100% (2)

- Banking MCQDocumento5 páginasBanking MCQJT GalAinda não há avaliações

- Rural Bank of Lipa vs. CA (G.r. No. 124535) Case DigestDocumento2 páginasRural Bank of Lipa vs. CA (G.r. No. 124535) Case DigestEricha Joy GonadanAinda não há avaliações

- Expertravel & Tours, Inc. vs. CA (G.R. No. 152392) CASE DIGESTDocumento1 páginaExpertravel & Tours, Inc. vs. CA (G.R. No. 152392) CASE DIGESTEricha Joy GonadanAinda não há avaliações

- Expertravel & Tours, Inc. vs. CA (G.R. No. 152392) CASE DIGESTDocumento1 páginaExpertravel & Tours, Inc. vs. CA (G.R. No. 152392) CASE DIGESTEricha Joy GonadanAinda não há avaliações

- BPI Family Savings Bank vs. St. Michael Medical Center, Inc. (DIGEST)Documento3 páginasBPI Family Savings Bank vs. St. Michael Medical Center, Inc. (DIGEST)Ericha Joy GonadanAinda não há avaliações

- Republic v. COCOFED (G.R. No. 147062-64) CASE DIGESTDocumento3 páginasRepublic v. COCOFED (G.R. No. 147062-64) CASE DIGESTEricha Joy GonadanAinda não há avaliações

- President Benigno Aquino Iii's 4TH State of The Nation Address (Sona) : A Critical Reflection Paper On Economic Planning & PolicyDocumento9 páginasPresident Benigno Aquino Iii's 4TH State of The Nation Address (Sona) : A Critical Reflection Paper On Economic Planning & PolicyMark Martin C. CelinoAinda não há avaliações

- Unlocking The Future Potential For Kenya: The Vision 2030: (Preliminary Draft)Documento29 páginasUnlocking The Future Potential For Kenya: The Vision 2030: (Preliminary Draft)riki187Ainda não há avaliações

- 04 PovertyDocumento10 páginas04 Povertyapi-3696301Ainda não há avaliações

- 2008 State of The Nation Address Technical Report PDFDocumento112 páginas2008 State of The Nation Address Technical Report PDFnow mAinda não há avaliações

- INTRODUCTIONDocumento3 páginasINTRODUCTIONMohdd HarryAinda não há avaliações

- Philippines GDP contraction moderates in Q4 2020Documento2 páginasPhilippines GDP contraction moderates in Q4 2020mohannad amanollahAinda não há avaliações

- Group7 MacroeconomicsDocumento21 páginasGroup7 MacroeconomicsAashay JainAinda não há avaliações

- MMMMSSSDocumento371 páginasMMMMSSSMhiltz Ibarra De GuiaAinda não há avaliações

- Prospects and Policy Challenges in The Twelfth Plan: Is IsDocumento18 páginasProspects and Policy Challenges in The Twelfth Plan: Is IsVaishnavi JayakumarAinda não há avaliações

- THE IMPACT OF ECONOMIC CRISES ON THE POOR IN SOUTHEAST ASIADocumento34 páginasTHE IMPACT OF ECONOMIC CRISES ON THE POOR IN SOUTHEAST ASIAMohd Faizol IsmailAinda não há avaliações

- Macroeconomics PDFDocumento74 páginasMacroeconomics PDFabainzaraymartAinda não há avaliações

- Peruvian Financial System Growth and StrategiesDocumento17 páginasPeruvian Financial System Growth and StrategiesGustavo MenaAinda não há avaliações

- 1.4 Poverty Reduction in East Asia-EnDocumento2 páginas1.4 Poverty Reduction in East Asia-EnАльбіна ДележаAinda não há avaliações

- "Philippine Economic Development": TO: Prof. Paul Espinosa SUBJECT: Economic Development AE 12Documento6 páginas"Philippine Economic Development": TO: Prof. Paul Espinosa SUBJECT: Economic Development AE 12adie2thalesAinda não há avaliações

- Bçì Êçç QK Dçåò Äéò Åç Oçë Êáç Dêéöçêáç J Å Ë ÅDocumento60 páginasBçì Êçç QK Dçåò Äéò Åç Oçë Êáç Dêéöçêáç J Å Ë ÅmarielAinda não há avaliações

- Economic Progress and Human Advancement in The Philippine ContextDocumento6 páginasEconomic Progress and Human Advancement in The Philippine Contextmayeee.eAinda não há avaliações

- Why Creativity and Innovation Is Important To MalaysiaDocumento14 páginasWhy Creativity and Innovation Is Important To MalaysiaDr Bugs Tan100% (1)

- Grp3 Ged103 ResDocumento9 páginasGrp3 Ged103 ResGabriele TalubAinda não há avaliações

- Examining Recent Trends in Poverty, Inequality, and Vulnerability (An Executive Summary)Documento12 páginasExamining Recent Trends in Poverty, Inequality, and Vulnerability (An Executive Summary)Jose Ramon G AlbertAinda não há avaliações

- III RecomendationsDocumento7 páginasIII RecomendationsTuấn TítAinda não há avaliações

- Real Change in Sight Despite Political SpectacleDocumento40 páginasReal Change in Sight Despite Political SpectacleibonsurveysAinda não há avaliações

- Growth and Poverty Reduction - Draft - ADBDocumento23 páginasGrowth and Poverty Reduction - Draft - ADBoryuichiAinda não há avaliações

- A Retrospective On Past 30 Years of Development in VietnamDocumento53 páginasA Retrospective On Past 30 Years of Development in VietnamJenny DangAinda não há avaliações

- Economy and Society 2 PDFDocumento62 páginasEconomy and Society 2 PDFSelvaraj VillyAinda não há avaliações

- Assignment 2Documento26 páginasAssignment 2Shar KhanAinda não há avaliações

- Research Paper 4Documento14 páginasResearch Paper 4Alishba AnjumAinda não há avaliações

- 12 Economics Case StudyDocumento9 páginas12 Economics Case StudyconnorAinda não há avaliações

- VIETNAM Achievements, Challenges, and the Path AheadDocumento2 páginasVIETNAM Achievements, Challenges, and the Path AheadVu ToanAinda não há avaliações

- Relationship Analysis of Economic Indicators in Laos and ThailandDocumento15 páginasRelationship Analysis of Economic Indicators in Laos and ThailandnarutoAinda não há avaliações

- Philippine Economic MalaiseDocumento2 páginasPhilippine Economic Malaiselaur33nAinda não há avaliações

- Poverty inDocumento4 páginasPoverty inAli TahirAinda não há avaliações

- Thailand Economic Growth and Trajectory: A Case Study Rishabh Vaish (14553), Siddarth Agarwal (14691), Akshay Wadhwani (14063)Documento7 páginasThailand Economic Growth and Trajectory: A Case Study Rishabh Vaish (14553), Siddarth Agarwal (14691), Akshay Wadhwani (14063)Rishabh VaishAinda não há avaliações

- Operational Plan 2011-2015 Dfid VietnamDocumento12 páginasOperational Plan 2011-2015 Dfid VietnamedselsawyerAinda não há avaliações

- India's Economic Growth and Response to the Global CrisisDocumento23 páginasIndia's Economic Growth and Response to the Global CrisisNILOTPAL SARKAR (RA2152001010046)Ainda não há avaliações

- Universal Health Care Coverage Through Pluralistic Approaches: Experience From ThailandDocumento27 páginasUniversal Health Care Coverage Through Pluralistic Approaches: Experience From ThailandThaworn SakunphanitAinda não há avaliações

- World Bank Assignment - PhilippinesDocumento8 páginasWorld Bank Assignment - PhilippinesMMMAinda não há avaliações

- Lesson 1.3Documento13 páginasLesson 1.3JCieldon C. LumusadAinda não há avaliações

- Explore Economic Growth As It Is The Objective of All Governments To Create Economic, Social, and Environmental Progress Opportunities For Their PeopleDocumento9 páginasExplore Economic Growth As It Is The Objective of All Governments To Create Economic, Social, and Environmental Progress Opportunities For Their PeopleJaydine Jenny SonnekusAinda não há avaliações

- EconDocumento23 páginasEconPJ BundalianAinda não há avaliações

- Research Paper of DR Fernando Aldaba (As of 21 May)Documento37 páginasResearch Paper of DR Fernando Aldaba (As of 21 May)meagon_cjAinda não há avaliações

- U Myint - Myanmar GDP Growth Rate Rev 01Documento8 páginasU Myint - Myanmar GDP Growth Rate Rev 01Ye PhoneAinda não há avaliações

- Philippines: Gilberto M. Llanto President, Philippine Institute For Development StudiesDocumento19 páginasPhilippines: Gilberto M. Llanto President, Philippine Institute For Development StudiesPatrisse ProsperoAinda não há avaliações

- Learning From Double-Digit Growth ExperiencesDocumento37 páginasLearning From Double-Digit Growth ExperiencesFelis_Demulcta_MitisAinda não há avaliações

- East Asia's Inclusive Growth Model 1Documento2 páginasEast Asia's Inclusive Growth Model 1Raheel AhmadAinda não há avaliações

- Duterte's Ambitious 'Build, Build, Build' Project To Transform The Philippines Could Become His LegacyDocumento18 páginasDuterte's Ambitious 'Build, Build, Build' Project To Transform The Philippines Could Become His LegacyJoana Mae AgusAinda não há avaliações

- Cornell Dyson Wp1815Documento15 páginasCornell Dyson Wp1815PIR AIZAZ ALI SHAHAinda não há avaliações

- Protección Social en CoreaDocumento44 páginasProtección Social en CoreaEl CuervoAinda não há avaliações

- Demographic Transition-SoteloDocumento5 páginasDemographic Transition-SoteloPilsam, Jr. SoteloAinda não há avaliações

- To Sustain Economy GrowthDocumento2 páginasTo Sustain Economy GrowthAishah AladdinAinda não há avaliações

- Assignment-2 Bangladesh EconomicsDocumento4 páginasAssignment-2 Bangladesh Economicsashraf07sAinda não há avaliações

- The Case of Paraguay: Working PaperDocumento35 páginasThe Case of Paraguay: Working PaperVFCAinda não há avaliações

- The Labor Market Story Behind Latin America’s TransformationNo EverandThe Labor Market Story Behind Latin America’s TransformationAinda não há avaliações

- Framework of Inclusive Growth Indicators 2012: Key Indicators for Asia and the Pacific Special SupplementNo EverandFramework of Inclusive Growth Indicators 2012: Key Indicators for Asia and the Pacific Special SupplementAinda não há avaliações

- Reviving Economic Growth: Policy Proposals from 51 Leading ExpertsNo EverandReviving Economic Growth: Policy Proposals from 51 Leading ExpertsAinda não há avaliações

- Spec Comm Compiled CasesDocumento20 páginasSpec Comm Compiled CasesEricha Joy GonadanAinda não há avaliações

- CASE in Polit LawDocumento2 páginasCASE in Polit LawEricha Joy GonadanAinda não há avaliações

- Lucman v. Malawi (G.R. No. 159794)Documento1 páginaLucman v. Malawi (G.R. No. 159794)Ericha Joy GonadanAinda não há avaliações

- North Cotabato v. Government of RPDocumento60 páginasNorth Cotabato v. Government of RPEricha Joy GonadanAinda não há avaliações

- Saguisag vs. Ochoa, JR., 779 SCRA 241, January 12, 2016Documento111 páginasSaguisag vs. Ochoa, JR., 779 SCRA 241, January 12, 2016Ericha Joy GonadanAinda não há avaliações

- Stockholder's Right to Inspect Corporate Records UpheldDocumento7 páginasStockholder's Right to Inspect Corporate Records UpheldEricha Joy GonadanAinda não há avaliações

- G.R. No. 150283 Yamamoto v. Nishino FULL CASEDocumento4 páginasG.R. No. 150283 Yamamoto v. Nishino FULL CASERose Ann VeloriaAinda não há avaliações

- G.R. No. 178511 (Genato vs. Ang) Full CaseDocumento7 páginasG.R. No. 178511 (Genato vs. Ang) Full CaseEricha Joy GonadanAinda não há avaliações

- G.R. No. 178511 (Genato vs. Ang) Full CaseDocumento7 páginasG.R. No. 178511 (Genato vs. Ang) Full CaseEricha Joy GonadanAinda não há avaliações

- G.R. No. 178511 (Genato vs. Ang) Full CaseDocumento7 páginasG.R. No. 178511 (Genato vs. Ang) Full CaseEricha Joy GonadanAinda não há avaliações

- Lee V CADocumento10 páginasLee V CAJojo FarconAinda não há avaliações

- Lee V CADocumento10 páginasLee V CAJojo FarconAinda não há avaliações

- Stockholder's Right to Inspect Corporate Records UpheldDocumento7 páginasStockholder's Right to Inspect Corporate Records UpheldEricha Joy GonadanAinda não há avaliações

- G.R. No. L-45911 (Gokongwei vs. Sec) Full CaseDocumento53 páginasG.R. No. L-45911 (Gokongwei vs. Sec) Full CaseEricha Joy GonadanAinda não há avaliações

- PCGG), PetitionerDocumento14 páginasPCGG), PetitionerInnah Agito-RamosAinda não há avaliações

- VagueDocumento1 páginaVagueEricha Joy GonadanAinda não há avaliações

- Canara Bank - Roadshow Presentation - 24th January 2018Documento26 páginasCanara Bank - Roadshow Presentation - 24th January 2018Vijay PawarAinda não há avaliações

- ALFI and ABBL Guidelines and Recommendations For Depositaries Safekeeping of Other AssetsDocumento62 páginasALFI and ABBL Guidelines and Recommendations For Depositaries Safekeeping of Other AssetsludivineAinda não há avaliações

- Assignment On Analysis of Annual Report ofDocumento12 páginasAssignment On Analysis of Annual Report ofdevbreezeAinda não há avaliações

- Stinnett's Pontiac Service, Inc., Richard W. Stinnett and Gay P. Stinnett v. Commissioner of Internal Revenue Service, 730 F.2d 634, 11th Cir. (1984)Documento11 páginasStinnett's Pontiac Service, Inc., Richard W. Stinnett and Gay P. Stinnett v. Commissioner of Internal Revenue Service, 730 F.2d 634, 11th Cir. (1984)Scribd Government DocsAinda não há avaliações

- Horizontal & Common-Size Analysis of Financial StatementsDocumento7 páginasHorizontal & Common-Size Analysis of Financial StatementsRichard MamisAinda não há avaliações

- Practical Accounting 2Documento4 páginasPractical Accounting 2RajkumariAinda não há avaliações

- The Market 2008Documento108 páginasThe Market 2008rakeshkrAinda não há avaliações

- Government Policy and Strategy: For SME DevelopmentDocumento22 páginasGovernment Policy and Strategy: For SME Developmentmonther32Ainda não há avaliações

- ProposalDocumento3 páginasProposalapi-488672844Ainda não há avaliações

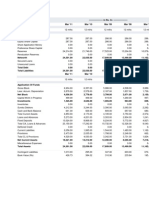

- 201B 201A Peso Change % ChangeDocumento4 páginas201B 201A Peso Change % ChangeNin JahAinda não há avaliações

- Great Indian Personalities and Business Tycoon Lakshmi MittalDocumento1 páginaGreat Indian Personalities and Business Tycoon Lakshmi MittalimmadiuttejAinda não há avaliações

- APM Terminals Company PresentationDocumento28 páginasAPM Terminals Company Presentationchuongnino123Ainda não há avaliações

- Balance Sheet of InfosysDocumento5 páginasBalance Sheet of InfosysLincy SubinAinda não há avaliações

- Fera and Fema: Submitted To: Prof. Anant AmdekarDocumento40 páginasFera and Fema: Submitted To: Prof. Anant AmdekarhasbicAinda não há avaliações

- Chapter 6Documento23 páginasChapter 6red8blue8Ainda não há avaliações

- Citizen - FinalDocumento54 páginasCitizen - FinalReshma DhulapAinda não há avaliações

- Practice Tests Partnership FormationDocumento10 páginasPractice Tests Partnership FormationClaire RamosAinda não há avaliações

- Ratio Analysis of Askari Bank LimitedDocumento26 páginasRatio Analysis of Askari Bank Limited✬ SHANZA MALIK ✬89% (9)

- Basic Problems of An EconomyDocumento2 páginasBasic Problems of An EconomyMaria Andrea SajoniaAinda não há avaliações

- Political BarrierDocumento1 páginaPolitical BarrierBrenda WijayaAinda não há avaliações

- RAASI Cement HimanshuDocumento7 páginasRAASI Cement HimanshuSamarth MewadaAinda não há avaliações

- Chapter 11 17Documento62 páginasChapter 11 17Melissa Cabigat Abdul KarimAinda não há avaliações