Você também pode gostar

- Mercantile Law Bar QDocumento106 páginasMercantile Law Bar QMark Joseph DelimaAinda não há avaliações

- Q and A COMMERCIAL LAWDocumento81 páginasQ and A COMMERCIAL LAWMichael Ortega Ligalig83% (6)

- Mogello - Siliman Answers To BarDocumento244 páginasMogello - Siliman Answers To BarMaria Izza Nicola KatonAinda não há avaliações

- Commercial LawDocumento61 páginasCommercial LawthebfilesAinda não há avaliações

- 2013 2014 2015 Q and A Commercial LawDocumento80 páginas2013 2014 2015 Q and A Commercial LawStarr Weigand100% (3)

- Mercantile Law Bar Exam Q&A 1990-2006Documento201 páginasMercantile Law Bar Exam Q&A 1990-2006John Dx Lapid100% (3)

- Labor Law 2019 Bar Q and ADocumento11 páginasLabor Law 2019 Bar Q and Acarlo dumlao100% (7)

- Civil Law Reviewer 2022 (Revised)Documento23 páginasCivil Law Reviewer 2022 (Revised)atb333100% (1)

- Pomoly Bar Reviewer Day 2 PM EthicsDocumento35 páginasPomoly Bar Reviewer Day 2 PM EthicsRomeo RemotinAinda não há avaliações

- Teleconferencing and corporate existence attacks definedDocumento10 páginasTeleconferencing and corporate existence attacks definednichols greenAinda não há avaliações

- Corporation Law Take Home Exams (Class Participation)Documento22 páginasCorporation Law Take Home Exams (Class Participation)julieanne07Ainda não há avaliações

- Labor 2015 Bar Questions With AnswersDocumento9 páginasLabor 2015 Bar Questions With AnswersJoshuaLavegaAbrina100% (3)

- Commercial Law Compilation Bar Q&a 1990-2017 PDFDocumento354 páginasCommercial Law Compilation Bar Q&a 1990-2017 PDFShane Fernandez Jardinico100% (6)

- 2017 Bar QuestionsDocumento49 páginas2017 Bar QuestionsKimmy Yu100% (1)

- Suggested Answers to Taxation Law Bar Questions (2014-2017Documento81 páginasSuggested Answers to Taxation Law Bar Questions (2014-2017Kyle Ruzzel SuyuAinda não há avaliações

- Commercial Law Compilation Bar Q&A 1990-2017Documento435 páginasCommercial Law Compilation Bar Q&A 1990-2017chenezAinda não há avaliações

- Labor Law Bar QA (2012-2015)Documento84 páginasLabor Law Bar QA (2012-2015)Bumbo S. Cruz67% (3)

- Labor Relations - Finals ReviewerDocumento27 páginasLabor Relations - Finals ReviewerPamela Parce100% (1)

- Mercantile (2006-2018)Documento88 páginasMercantile (2006-2018)ptdwnhroAinda não há avaliações

- UST GN 2011 - Labor Law TablesDocumento12 páginasUST GN 2011 - Labor Law TablesGhost100% (4)

- A Compilation of Bar Questions and Suggested Answers Civil LawDocumento118 páginasA Compilation of Bar Questions and Suggested Answers Civil LawKym Algarme93% (28)

- CIVIL LAW Bar QA 1996 2016 PDFDocumento104 páginasCIVIL LAW Bar QA 1996 2016 PDFJuan ShahAinda não há avaliações

- Labor 2018 Bar Question and AnswerDocumento14 páginasLabor 2018 Bar Question and AnswerTap cruz89% (18)

- MOCK-BAR Labor AnswerkeyDocumento28 páginasMOCK-BAR Labor AnswerkeypaulAinda não há avaliações

- LABOR LAW MOCK BAR ANSWERSDocumento8 páginasLABOR LAW MOCK BAR ANSWERSJo Vic Cata Bona0% (1)

- PUP Iskolar's Aid Remedial LawDocumento237 páginasPUP Iskolar's Aid Remedial LawAmorsky LimAinda não há avaliações

- Simple Law Student 2007 2013 Bar Questions On Corporation LawsDocumento9 páginasSimple Law Student 2007 2013 Bar Questions On Corporation LawsAlexander Abonado100% (1)

- Be It Enacted by The Senate and The House of Representatives of The Philippines in Congress AssembledDocumento9 páginasBe It Enacted by The Senate and The House of Representatives of The Philippines in Congress AssembledKim SimagalaAinda não há avaliações

- Commercial Law Bar Q - A (2017-2019) (4D1920)Documento51 páginasCommercial Law Bar Q - A (2017-2019) (4D1920)Sage Lingatong50% (2)

- Pomoly Bar Reviewer Day 2 Am CivDocumento111 páginasPomoly Bar Reviewer Day 2 Am CivRomeo RemotinAinda não há avaliações

- EVIDENCE RULES SUMMARYDocumento17 páginasEVIDENCE RULES SUMMARYIrish BalabaAinda não há avaliações

- 2016 Mercantile Bar Questions and AnswersDocumento5 páginas2016 Mercantile Bar Questions and AnswersLinday LohanAinda não há avaliações

- 2016 Bar Examinations Labor LawDocumento10 páginas2016 Bar Examinations Labor LawMelody Ann MercadoAinda não há avaliações

- Conflict of LawDocumento13 páginasConflict of LawBo DistAinda não há avaliações

- Bar Exam Qs Taxation LawDocumento123 páginasBar Exam Qs Taxation LawUlyssesAinda não há avaliações

- Bar Questions and Answers in Mercantile LawDocumento248 páginasBar Questions and Answers in Mercantile LawKen ArnozaAinda não há avaliações

- Bar Exam 2010 Suggested Answers in LABOR AND SOCIAL LEGISLATIONDocumento19 páginasBar Exam 2010 Suggested Answers in LABOR AND SOCIAL LEGISLATIONargaoAinda não há avaliações

- Rem Law Bar 20182019Documento15 páginasRem Law Bar 20182019MargeAinda não há avaliações

- 5 Mercantile Law Bar Questions and Answers (2007-2017) PDFDocumento146 páginas5 Mercantile Law Bar Questions and Answers (2007-2017) PDFAngelica Fojas Rañola100% (6)

- Insurance Compilation of BarQsDocumento49 páginasInsurance Compilation of BarQsRocky Yap100% (1)

- Corporation TranscriptDocumento20 páginasCorporation TranscriptEarl Ian Debalucos100% (1)

- Corporation Bar QsDocumento111 páginasCorporation Bar QsPARDS MOTOVLOGSAinda não há avaliações

- Political Law Compiled 2006-2019Documento79 páginasPolitical Law Compiled 2006-2019IanLightPajaroAinda não há avaliações

- Printing Tax Bqa PDFDocumento51 páginasPrinting Tax Bqa PDFAzumi RobinAinda não há avaliações

- Corporation Code As Amended 2019Documento65 páginasCorporation Code As Amended 2019mc.rockz14Ainda não há avaliações

- Commercial Preweek Notes by Zarah CastroDocumento34 páginasCommercial Preweek Notes by Zarah CastroChrislyned Garces-Tan100% (1)

- Provisional Remedies 101Documento151 páginasProvisional Remedies 101Jeters VillaruelAinda não há avaliações

- USJR - Provrem - Support (2017) EDocumento27 páginasUSJR - Provrem - Support (2017) EPeter AllanAinda não há avaliações

- 400 Important Provisions by AlbanoDocumento56 páginas400 Important Provisions by AlbanoGracey CasianoAinda não há avaliações

- Case DoctrineDocumento17 páginasCase DoctrineAbdulRacman PindatonAinda não há avaliações

- Mercantile Law (1990-2014)Documento294 páginasMercantile Law (1990-2014)juju_batugalAinda não há avaliações

- Insurance Claim Dispute Over Stolen VehicleDocumento23 páginasInsurance Claim Dispute Over Stolen VehicleRosalyn Bahia100% (2)

- Remedial Law Bar Exam Compilation (2014-2018)Documento45 páginasRemedial Law Bar Exam Compilation (2014-2018)Anonymous oTRzcSSGunAinda não há avaliações

- 2014 Bar Exam QuestionsDocumento30 páginas2014 Bar Exam QuestionsdetteheartsAinda não há avaliações

- Commercial Law Bar 2014Documento21 páginasCommercial Law Bar 2014Dodong Lamela100% (1)

- Commercial Law 2014Documento21 páginasCommercial Law 2014Clarisse HattonAinda não há avaliações

- 2014 Remedial Law Bar Exam and AnswersDocumento11 páginas2014 Remedial Law Bar Exam and AnswersHome MalonAinda não há avaliações

- 2014 Bar ExaminationsDocumento10 páginas2014 Bar ExaminationsMariaAinda não há avaliações

- q14 BarDocumento25 páginasq14 BarTannie Lyn Ebarle BasubasAinda não há avaliações

- 1990 2014 Merc Law Bar Exam Q and ADocumento260 páginas1990 2014 Merc Law Bar Exam Q and ADahlia Claudine May Perral0% (1)

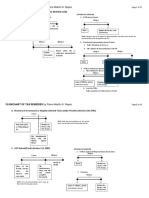

- Flowchart of Tax Remedies I. Remedies Un PDFDocumento12 páginasFlowchart of Tax Remedies I. Remedies Un PDFJunivenReyUmadhayAinda não há avaliações

- Flowchart of Tax Remedies I. Remedies Un PDFDocumento12 páginasFlowchart of Tax Remedies I. Remedies Un PDFJunivenReyUmadhayAinda não há avaliações

- Biodata Format FinalDocumento2 páginasBiodata Format Finalanon-90865197% (120)

- Interview LectureDocumento10 páginasInterview LectureZoe Gacod Takumii UsuiiAinda não há avaliações

- Bar Q and A (2007-2008)Documento3 páginasBar Q and A (2007-2008)Zoe Gacod Takumii UsuiiAinda não há avaliações

- Biodata Format FinalDocumento2 páginasBiodata Format Finalanon-90865197% (120)

- 2014 Commercial Law Bar Q and ADocumento20 páginas2014 Commercial Law Bar Q and AZoe Gacod Takumii UsuiiAinda não há avaliações

- 2014 Commercial Law Bar Q and ADocumento20 páginas2014 Commercial Law Bar Q and AZoe Gacod Takumii UsuiiAinda não há avaliações

- 14 15Documento5 páginas14 15Zoe Gacod Takumii UsuiiAinda não há avaliações

- DNA Rules On EvidenceDocumento4 páginasDNA Rules On EvidenceZoe Gacod Takumii UsuiiAinda não há avaliações

- Republic of The Philippines First Judicial Region Municipal Trial Court Branch 5 Baguio CityDocumento7 páginasRepublic of The Philippines First Judicial Region Municipal Trial Court Branch 5 Baguio CityZoe Gacod Takumii UsuiiAinda não há avaliações

- Tax InversionDocumento1 páginaTax InversionZoe Gacod Takumii UsuiiAinda não há avaliações

- Unethical business practices and treatment of competitorsDocumento2 páginasUnethical business practices and treatment of competitorsZoe Gacod Takumii UsuiiAinda não há avaliações

- Summarized Table of Just Causes and Authorized CausesDocumento3 páginasSummarized Table of Just Causes and Authorized CausesZoe Gacod Takumii UsuiiAinda não há avaliações

- Mead Vs McCullough Case DigestDocumento3 páginasMead Vs McCullough Case DigestZoe Gacod Takumii Usuii0% (1)

- Intellectual Property Law On CopyrightDocumento26 páginasIntellectual Property Law On CopyrightZoe Gacod Takumii UsuiiAinda não há avaliações

- Barcelon vs. BakerDocumento3 páginasBarcelon vs. BakerZoe Gacod Takumii UsuiiAinda não há avaliações

- Constitutional Law 2Documento3 páginasConstitutional Law 2Zoe Gacod Takumii UsuiiAinda não há avaliações

- Transportation Case DigestDocumento5 páginasTransportation Case DigestZoe Gacod Takumii UsuiiAinda não há avaliações

- The First Issue Involved Is Simple Enough: Should A Special Indorsement On Bearer Paper Control Its Future Negotiation?Documento4 páginasThe First Issue Involved Is Simple Enough: Should A Special Indorsement On Bearer Paper Control Its Future Negotiation?Zoe Gacod Takumii UsuiiAinda não há avaliações

- Marriage Without LicenseDocumento2 páginasMarriage Without LicenseZoe Gacod Takumii UsuiiAinda não há avaliações

- UST GN 2011 - Labor Law TablesDocumento12 páginasUST GN 2011 - Labor Law TablesGhost100% (4)

- Magna Carta of WomenDocumento16 páginasMagna Carta of WomenZoe Gacod Takumii UsuiiAinda não há avaliações

- 30 Hussainara Khatoon (II)Documento4 páginas30 Hussainara Khatoon (II)devrudra07Ainda não há avaliações

- 099-Vassar Industries Employees Union v. Estrella G.R. No. L-46562 March 31, 1978Documento4 páginas099-Vassar Industries Employees Union v. Estrella G.R. No. L-46562 March 31, 1978Jopan SJAinda não há avaliações

- CPC IndiaDocumento14 páginasCPC IndiaVishnu NarayananAinda não há avaliações

- Bagaoisan v. National Tobacco AdministrationDocumento12 páginasBagaoisan v. National Tobacco AdministrationKristinaCuetoAinda não há avaliações

- Janet I Fischer Vs UsDocumento66 páginasJanet I Fischer Vs Uslegalmatters100% (1)

- CHR Lacks Jurisdiction to Adjudicate Teacher DismissalsDocumento2 páginasCHR Lacks Jurisdiction to Adjudicate Teacher DismissalsEbbe DyAinda não há avaliações

- Grand Juries Vol 38a Corpusjurissecundum 1Documento65 páginasGrand Juries Vol 38a Corpusjurissecundum 1Truth Press Media100% (1)

- Special Proceedings Rule 82 Rule 83Documento40 páginasSpecial Proceedings Rule 82 Rule 83ptdwnhroAinda não há avaliações

- Gamb v. Hilton Hotels Corp., 132 F.3d 46, 11th Cir. (1997)Documento1 páginaGamb v. Hilton Hotels Corp., 132 F.3d 46, 11th Cir. (1997)Scribd Government DocsAinda não há avaliações

- Srikant Pandey Affidavit and BailDocumento8 páginasSrikant Pandey Affidavit and Bailalok srivastavaAinda não há avaliações

- Show MultidocsDocumento11 páginasShow MultidocsAnonymous GF8PPILW5Ainda não há avaliações

- Don SamuelsDocumento3 páginasDon SamuelsSarah McKenzieAinda não há avaliações

- Role of Foreign Decisions in Interpretation: Waquar AhmadDocumento17 páginasRole of Foreign Decisions in Interpretation: Waquar AhmadEarphone BhaiAinda não há avaliações

- Contract Act 1872 For MBADocumento47 páginasContract Act 1872 For MBARavi Sharma0% (1)

- People vs. PagalasanDocumento33 páginasPeople vs. PagalasanDaley Catugda100% (1)

- Election Law Syllabus OverviewDocumento3 páginasElection Law Syllabus OverviewloricaloAinda não há avaliações

- Philip Mathews vs. Benjamin and Joselyn Taylor, GR 164584, June 22, 2009Documento4 páginasPhilip Mathews vs. Benjamin and Joselyn Taylor, GR 164584, June 22, 2009FranzMordenoAinda não há avaliações

- Nebreja v. Reonal - A.C. No. 9896 (Resolution)Documento6 páginasNebreja v. Reonal - A.C. No. 9896 (Resolution)Amielle CanilloAinda não há avaliações

- Kendra's Law - New York's Assisted Outpatient Treatment StatuteDocumento23 páginasKendra's Law - New York's Assisted Outpatient Treatment StatuteAlexander J. NicasAinda não há avaliações

- Lot No. 6278-M, A 17,181 Square Meter Parcel of Land Covered by TCT No. T-11397Documento3 páginasLot No. 6278-M, A 17,181 Square Meter Parcel of Land Covered by TCT No. T-11397Sonny MorilloAinda não há avaliações

- Felicisimo M. Montano vs. Ibp and Atty. Juan S. Dealca, Ac No. 4215Documento3 páginasFelicisimo M. Montano vs. Ibp and Atty. Juan S. Dealca, Ac No. 4215Katharina CantaAinda não há avaliações

- Tijam vs. SibonghanoyDocumento4 páginasTijam vs. SibonghanoyIrish Bianca Usob LunaAinda não há avaliações

- Codal Coverage For PropertyDocumento5 páginasCodal Coverage For PropertyRomAinda não há avaliações

- Mankind ProjectDocumento20 páginasMankind ProjectTheresa VanHorn D'AngeloAinda não há avaliações

- Diokno Notes of TrialDocumento16 páginasDiokno Notes of TrialIsidore Tarol III80% (10)

- People of The Philippines, Appellee, Versus Roberto Quiachon Y Bayona, AppeellantDocumento9 páginasPeople of The Philippines, Appellee, Versus Roberto Quiachon Y Bayona, AppeellantPiayaAinda não há avaliações

- HARIHAR Calls For The Disbarment of David E. Fialkow - K&L Gates Atty For WELLS FARGO and US BANK (Ref. HARIHAR V US BANK Et Al)Documento27 páginasHARIHAR Calls For The Disbarment of David E. Fialkow - K&L Gates Atty For WELLS FARGO and US BANK (Ref. HARIHAR V US BANK Et Al)Mohan Harihar100% (1)

- Crim 2 Reviewer - Slander Part 2Documento9 páginasCrim 2 Reviewer - Slander Part 2SuiAinda não há avaliações

- V. Contract of AdhesionDocumento2 páginasV. Contract of AdhesionAngela Louise SabaoanAinda não há avaliações

- Interview Insights on Legal Writing StyleDocumento2 páginasInterview Insights on Legal Writing StyleSharan HansAinda não há avaliações