Você também pode gostar

- PlanetTran EvaluationDocumento18 páginasPlanetTran EvaluationNATOEEAinda não há avaliações

- Test Bank For Essentials of Corporate Finance 9th Edition by RossDocumento24 páginasTest Bank For Essentials of Corporate Finance 9th Edition by Rosspauljohnstonapgsoemyjk98% (45)

- XZT-Quadzilla InstallDocumento2 páginasXZT-Quadzilla InstallAfzal Imam0% (1)

- Answer The Questions That Follow The Case Information System in RestaurantDocumento4 páginasAnswer The Questions That Follow The Case Information System in RestaurantTonmoy Borah0% (1)

- Branch Vs Subsidiary (TAX)Documento4 páginasBranch Vs Subsidiary (TAX)pokeball001Ainda não há avaliações

- Foreign Corporation Registration in TheDocumento2 páginasForeign Corporation Registration in TheDodongAinda não há avaliações

- Registration of A Representative OfficeDocumento2 páginasRegistration of A Representative OfficeGlory PerezAinda não há avaliações

- Affidavit of Loss - PassportDocumento1 páginaAffidavit of Loss - PassportAnna Victoria Dela VegaAinda não há avaliações

- Data Privacy Act Bar Review Notes 2019Documento15 páginasData Privacy Act Bar Review Notes 2019Heidi De'NakedAinda não há avaliações

- 2nd Motex VergaraDocumento4 páginas2nd Motex VergaraMarie AlarconAinda não há avaliações

- TH ST RDDocumento2 páginasTH ST RDVivo MayvelAinda não há avaliações

- 2021 Forecast - Civil LawDocumento59 páginas2021 Forecast - Civil LawSheilaAinda não há avaliações

- EMELINO T MAESTRO BIR Ask For ReceiptDocumento1 páginaEMELINO T MAESTRO BIR Ask For Receiptjuliet_emelinotmaestroAinda não há avaliações

- Salient Features of The Revised Guidelines For Continuous Trial of Criminal CasesDocumento7 páginasSalient Features of The Revised Guidelines For Continuous Trial of Criminal CasesIbiang DeleozAinda não há avaliações

- National Taxation (Income & Business Tax) OCTOBER 1, 2014Documento39 páginasNational Taxation (Income & Business Tax) OCTOBER 1, 2014Eliza Corpuz GadonAinda não há avaliações

- Feb 8 Senate Impeachment Court RecordDocumento79 páginasFeb 8 Senate Impeachment Court RecordVERA FilesAinda não há avaliações

- Agpalo Book OutlineDocumento9 páginasAgpalo Book OutlineLeighAinda não há avaliações

- 2009 RMC 23-2009 LOA RevalidationDocumento2 páginas2009 RMC 23-2009 LOA Revalidationedong the greatAinda não há avaliações

- Criminal Law Mock BarDocumento9 páginasCriminal Law Mock BarJonathan ClarusAinda não há avaliações

- Tax Remedies Chapter 2 ReportDocumento69 páginasTax Remedies Chapter 2 ReportVinz G. VizAinda não há avaliações

- Labor Procedure Charts (Edited)Documento11 páginasLabor Procedure Charts (Edited)Edward Kenneth KungAinda não há avaliações

- 11 Saraza Vs FranciscoDocumento11 páginas11 Saraza Vs FranciscoMRAinda não há avaliações

- The Philippine Accountancy Act of 2004Documento74 páginasThe Philippine Accountancy Act of 2004YamateAinda não há avaliações

- Enbanc: DecisionDocumento15 páginasEnbanc: DecisionGilbert John LacorteAinda não há avaliações

- Fringe Benefit Tax Train LawDocumento27 páginasFringe Benefit Tax Train LawJoyce Leeann Manansala75% (4)

- Doctrines AntichresisDocumento15 páginasDoctrines AntichresisMargeAinda não há avaliações

- TAX REMEDIES UNDER THE NIRC PowerDocumento5 páginasTAX REMEDIES UNDER THE NIRC PowerjonahAinda não há avaliações

- Summary of Significant SC Decisions (April May June 2011)Documento2 páginasSummary of Significant SC Decisions (April May June 2011)elmersgluethebombAinda não há avaliações

- DOJ DC 38s of 2012 PDFDocumento7 páginasDOJ DC 38s of 2012 PDFSammy EscañoAinda não há avaliações

- Taxrev SyllabusDocumento12 páginasTaxrev SyllabusDiane JulianAinda não há avaliações

- Pleading - Ariola - Specific Perforamnce - 7october2019Documento3 páginasPleading - Ariola - Specific Perforamnce - 7october2019Paul AriolaAinda não há avaliações

- NU 3 Phil Deposit Insurance LawDocumento36 páginasNU 3 Phil Deposit Insurance LawBack upAinda não há avaliações

- Promoting E-Governance Through Right To InformationDocumento9 páginasPromoting E-Governance Through Right To InformationIJSER ( ISSN 2229-5518 )Ainda não há avaliações

- Notes in Legal CounsellingDocumento11 páginasNotes in Legal CounsellingJenely Joy Areola-TelanAinda não há avaliações

- AUSL Bar Operations 2017 LMT Property EditedDocumento6 páginasAUSL Bar Operations 2017 LMT Property EditedEron Roi Centina-gacutanAinda não há avaliações

- Finals Commercial LawDocumento2 páginasFinals Commercial Lawvn wnstnAinda não há avaliações

- CMBE 2018 Taxation Law Suggested Answers - 9-23-18Documento19 páginasCMBE 2018 Taxation Law Suggested Answers - 9-23-18Remnant KaysAinda não há avaliações

- BSP Guideline On Registration-Of-Foreign-InvestmentsDocumento6 páginasBSP Guideline On Registration-Of-Foreign-InvestmentsmtscoAinda não há avaliações

- Paprint Chan ReviewerDocumento77 páginasPaprint Chan ReviewerLois Renee TubonAinda não há avaliações

- D'Armoured v. OrpiaDocumento3 páginasD'Armoured v. OrpiaTJ CortezAinda não há avaliações

- Petition - Manggapis EditedDocumento9 páginasPetition - Manggapis EditedGlendz RetubadoAinda não há avaliações

- MOA SampleDocumento8 páginasMOA SampleCrisDBAinda não há avaliações

- Bersamin Dicta in Disini v. Sandiganbayan PDFDocumento28 páginasBersamin Dicta in Disini v. Sandiganbayan PDFirwinarielmielAinda não há avaliações

- 17abad Vs BiasonDocumento2 páginas17abad Vs BiasonmarbienAinda não há avaliações

- SababanMagicNotes TaxationLaw1Documento46 páginasSababanMagicNotes TaxationLaw1Marife Tubilag Maneja100% (1)

- TaxDocumento12 páginasTaxCherry DuldulaoAinda não há avaliações

- 2013 Bar QuestionsDocumento95 páginas2013 Bar QuestionsMJ DecolongonAinda não há avaliações

- Cases - Assigned - B in DocsDocumento21 páginasCases - Assigned - B in Docsjanine nenariaAinda não há avaliações

- Political Law BarqsDocumento22 páginasPolitical Law BarqsMuhammad FadelAinda não há avaliações

- Ecommerce Act PDFDocumento35 páginasEcommerce Act PDFChristian GabrielAinda não há avaliações

- SEC Form SampleDocumento3 páginasSEC Form SampleBrandon Beach100% (1)

- Annulment of MarriageDocumento9 páginasAnnulment of MarriageReynante GungonAinda não há avaliações

- IBP JFBA - Conference Convenor SummaryDocumento7 páginasIBP JFBA - Conference Convenor SummaryAngela ConejeroAinda não há avaliações

- Taxation LawDocumento4 páginasTaxation LawtynajoydelossantosAinda não há avaliações

- Title XIII of The RPC: Crimes Against HonourDocumento16 páginasTitle XIII of The RPC: Crimes Against HonourNorman CaronanAinda não há avaliações

- LegCoun InterviewDocumento4 páginasLegCoun InterviewJohansen FerrerAinda não há avaliações

- ADR Operations Manual - AM No 01-10-05 SC - ADR GuidelinesDocumento15 páginasADR Operations Manual - AM No 01-10-05 SC - ADR GuidelinesRaffy PangilinanAinda não há avaliações

- Example Legal OpinionDocumento4 páginasExample Legal OpinionKristine De VillaAinda não há avaliações

- Tax ReviewerDocumento39 páginasTax ReviewerLuigiMangayaAinda não há avaliações

- VatDocumento5 páginasVatninaryzaAinda não há avaliações

- Urban & Rural Use: Enp Gus AgostoDocumento22 páginasUrban & Rural Use: Enp Gus AgostoAngel Grace BayangAinda não há avaliações

- Articles of Incorporation GreenDocumento14 páginasArticles of Incorporation GreenMarkus AureliusAinda não há avaliações

- Business Registration RequirementsDocumento17 páginasBusiness Registration RequirementsBeverlyAinda não há avaliações

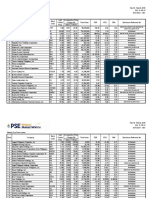

- Weekly Top Price Gainers Rank Company Stock Code Last Traded Price Disclosure Reference No. PBV Total Value PER EPS Comparative Price Change (%)Documento3 páginasWeekly Top Price Gainers Rank Company Stock Code Last Traded Price Disclosure Reference No. PBV Total Value PER EPS Comparative Price Change (%)Kristian AguilarAinda não há avaliações

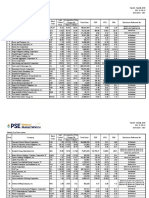

- Weekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVDocumento3 páginasWeekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVKristian AguilarAinda não há avaliações

- Weekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVDocumento3 páginasWeekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVKristian AguilarAinda não há avaliações

- Weekly Top Price Gainers Rank Company Stock Code Last Traded Price Disclosure Reference No. PBV Total Value PER EPS Comparative Price Change (%)Documento3 páginasWeekly Top Price Gainers Rank Company Stock Code Last Traded Price Disclosure Reference No. PBV Total Value PER EPS Comparative Price Change (%)Kristian AguilarAinda não há avaliações

- Weekly Top Price Gainers Rank Company Stock Code Last Traded Price Disclosure Reference No. PBV Total Value PER EPS Comparative Price Change (%)Documento3 páginasWeekly Top Price Gainers Rank Company Stock Code Last Traded Price Disclosure Reference No. PBV Total Value PER EPS Comparative Price Change (%)Kristian AguilarAinda não há avaliações

- Weekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVDocumento3 páginasWeekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVKristian AguilarAinda não há avaliações

- Weekly Top Price Gainers Rank Company Stock Code Last Traded Price Disclosure Reference No. PBV Total Value PER EPS Comparative Price Change (%)Documento3 páginasWeekly Top Price Gainers Rank Company Stock Code Last Traded Price Disclosure Reference No. PBV Total Value PER EPS Comparative Price Change (%)Kristian AguilarAinda não há avaliações

- Weekly Top Price Gainers Rank Company Stock Code Last Traded Price Disclosure Reference No. PBV Total Value PER EPS Comparative Price Change (%)Documento3 páginasWeekly Top Price Gainers Rank Company Stock Code Last Traded Price Disclosure Reference No. PBV Total Value PER EPS Comparative Price Change (%)Kristian AguilarAinda não há avaliações

- Weekly Top Price Gainers Rank Company Stock Code Last Traded Price Disclosure Reference No. PBV Total Value PER EPS Comparative Price Change (%)Documento3 páginasWeekly Top Price Gainers Rank Company Stock Code Last Traded Price Disclosure Reference No. PBV Total Value PER EPS Comparative Price Change (%)Kristian AguilarAinda não há avaliações

- Pinoy Millionaire Game Plan The BlueprintDocumento22 páginasPinoy Millionaire Game Plan The BlueprintKristian AguilarAinda não há avaliações

- Weekly Top Price Gainers Rank Company Stock Code Last Traded Price Disclosure Reference No. PBV Total Value PER EPS Comparative Price Change (%)Documento3 páginasWeekly Top Price Gainers Rank Company Stock Code Last Traded Price Disclosure Reference No. PBV Total Value PER EPS Comparative Price Change (%)Kristian AguilarAinda não há avaliações

- Weekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVDocumento3 páginasWeekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVKristian AguilarAinda não há avaliações

- Weekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVDocumento4 páginasWeekly Top Price Gainers Total Value PER EPS Comparative Price Change (%) Rank Company Stock Code Last Traded Price Disclosure Reference No. PBVKristian AguilarAinda não há avaliações

- SdfasdfasdfDocumento9 páginasSdfasdfasdfsimonAinda não há avaliações

- Scribd DL4Documento1 páginaScribd DL4Kristian AguilarAinda não há avaliações

- SdfasdfasdfDocumento9 páginasSdfasdfasdfsimonAinda não há avaliações

- SdfasdfasdfDocumento9 páginasSdfasdfasdfsimonAinda não há avaliações

- Scribd 2Documento1 páginaScribd 2Kristian AguilarAinda não há avaliações

- Scribd DL1Documento1 páginaScribd DL1Kristian AguilarAinda não há avaliações

- SdfasdfasdfDocumento9 páginasSdfasdfasdfsimonAinda não há avaliações

- Asdasdsafsdfcsdfsdf SDF SDF Sdfs DF GRT Htyjk Uig Lol HiDocumento1 páginaAsdasdsafsdfcsdfsdf SDF SDF Sdfs DF GRT Htyjk Uig Lol HiKristian AguilarAinda não há avaliações

- Scribd DL3Documento1 páginaScribd DL3Kristian AguilarAinda não há avaliações

- Asdasdsafsdfcsdfsdf SDF SDF Sdfs DF GRT Htyjk Uig Lol HiDocumento1 páginaAsdasdsafsdfcsdfsdf SDF SDF Sdfs DF GRT Htyjk Uig Lol HiKristian AguilarAinda não há avaliações

- Scribd DL2Documento1 páginaScribd DL2Kristian AguilarAinda não há avaliações

- FC-pascual Vs Cir (1988)Documento6 páginasFC-pascual Vs Cir (1988)Abbot ReyesAinda não há avaliações

- Herewego 59Documento6 páginasHerewego 59Kristian AguilarAinda não há avaliações

- CIR V Soriano DigestDocumento4 páginasCIR V Soriano DigestKristian AguilarAinda não há avaliações

- Scribd DL1Documento1 páginaScribd DL1Kristian AguilarAinda não há avaliações

- Herewego 23Documento2 páginasHerewego 23Kristian AguilarAinda não há avaliações

- Chapter 1 (Group 5)Documento6 páginasChapter 1 (Group 5)Chariese May MacapiaAinda não há avaliações

- Overview of Project FinanceDocumento76 páginasOverview of Project FinanceVaidyanathan Ravichandran100% (1)

- 124-Video Conference RFP PDFDocumento64 páginas124-Video Conference RFP PDFSV BAinda não há avaliações

- WorkdayDocumento22 páginasWorkdaysunnydeol4580% (5)

- 6418940483439f07302c4c4d - Employment Contract Agreement TemplateDocumento4 páginas6418940483439f07302c4c4d - Employment Contract Agreement TemplatepablooliveiraprestesAinda não há avaliações

- JP Morgan IB TaskDocumento2 páginasJP Morgan IB TaskDhanush JainAinda não há avaliações

- Ibc Notes 636839419149778471 PDFDocumento151 páginasIbc Notes 636839419149778471 PDFVrinda GuptaAinda não há avaliações

- The Issues On Corporate GovernanceDocumento15 páginasThe Issues On Corporate Governanceanitama_aminAinda não há avaliações

- Week 8 Case Study 10 - Shouldice Hospital LimitedDocumento6 páginasWeek 8 Case Study 10 - Shouldice Hospital LimitedMahpara Rahman RafaAinda não há avaliações

- Literature Review On Employees RetentionDocumento8 páginasLiterature Review On Employees Retentionafdtnybjp100% (1)

- Nutanix Designing & Building Hybrid Cloud OReillyDocumento51 páginasNutanix Designing & Building Hybrid Cloud OReillyPiyush ChavdaAinda não há avaliações

- International Trade Finance - Nov 2009Documento8 páginasInternational Trade Finance - Nov 2009Basilio MaliwangaAinda não há avaliações

- Tugas 2 - Unit 3 System Wide ConceptDocumento19 páginasTugas 2 - Unit 3 System Wide ConceptRista RistaAinda não há avaliações

- Developing SMART Goals For Your OrganizationDocumento2 páginasDeveloping SMART Goals For Your OrganizationtrangAinda não há avaliações

- Listening Comprehension SectionDocumento41 páginasListening Comprehension SectionKhoirul AnasAinda não há avaliações

- Sales Promotion & Methods ADVDocumento36 páginasSales Promotion & Methods ADVNATUREAinda não há avaliações

- Sage X3 Important Acronyms and DefinitionsDocumento4 páginasSage X3 Important Acronyms and DefinitionsMohamed AliAinda não há avaliações

- Audit ClauseDocumento3 páginasAudit ClauseSonica DhankharAinda não há avaliações

- Lesson 5 Information System DevelopmentDocumento15 páginasLesson 5 Information System DevelopmentDominic Dave Davin EmboresAinda não há avaliações

- Arvind MillsDocumento33 páginasArvind MillshasmukhAinda não há avaliações

- Day1 10daysaccountingchallengeDocumento16 páginasDay1 10daysaccountingchallengeSeungyun ChoAinda não há avaliações

- Mountain Man Brewing Company Case Study Essay Example For Free - Sample 2525 WordsDocumento8 páginasMountain Man Brewing Company Case Study Essay Example For Free - Sample 2525 WordsAnshul Yadav100% (1)

- Literature Review: Group 1 BADB3024 Research MethodDocumento32 páginasLiterature Review: Group 1 BADB3024 Research Methodyoyohoney singleAinda não há avaliações

- Bata AssignmentDocumento5 páginasBata AssignmentMumit Ahmed100% (1)

- Call For Expression of InterestDocumento1 páginaCall For Expression of InterestBen AdamteyAinda não há avaliações

- How To Master Sprint PlanningDocumento19 páginasHow To Master Sprint PlanningAshok KumarAinda não há avaliações