Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Gov AccDocumento17 páginasGov AccMon CuiAinda não há avaliações

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- Cordova, Monique C. BSA 4-1Documento4 páginasCordova, Monique C. BSA 4-1Mon CuiAinda não há avaliações

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Philippines To Spain FinalDocumento9 páginasPhilippines To Spain FinalMon CuiAinda não há avaliações

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (894)

- Audprob Quiz in Investment 20171004085936Documento4 páginasAudprob Quiz in Investment 20171004085936Mon CuiAinda não há avaliações

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Lesson 3 - Advent of A HeroDocumento21 páginasLesson 3 - Advent of A HeroMon CuiAinda não há avaliações

- Meal PlanDocumento1 páginaMeal PlanMon CuiAinda não há avaliações

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- Jam Corporation: InformationDocumento35 páginasJam Corporation: InformationMon CuiAinda não há avaliações

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Adjustment of The Obligation Incurred After The ProcessingDocumento9 páginasAdjustment of The Obligation Incurred After The ProcessingMon CuiAinda não há avaliações

- Cordova, Monique C. BSA 4-1Documento4 páginasCordova, Monique C. BSA 4-1Mon CuiAinda não há avaliações

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (265)

- Paris To Berlin JPR ReportDocumento23 páginasParis To Berlin JPR ReportMon CuiAinda não há avaliações

- New Doc 2017 08 31 21.54.50 - 20170905194201Documento6 páginasNew Doc 2017 08 31 21.54.50 - 20170905194201Mon CuiAinda não há avaliações

- Spain To ParisDocumento6 páginasSpain To ParisMon CuiAinda não há avaliações

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- CPA Review School Philippines Audit EngagementDocumento4 páginasCPA Review School Philippines Audit EngagementshambiruarAinda não há avaliações

- CH 4 ConsumptionDocumento40 páginasCH 4 ConsumptionMon CuiAinda não há avaliações

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Nuclear Power PlantDocumento5 páginasNuclear Power PlantMon CuiAinda não há avaliações

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- 01Documento24 páginas01Mon Cui100% (1)

- InvestmentGuide PDFDocumento2 páginasInvestmentGuide PDFMon CuiAinda não há avaliações

- At Quizzer (CPAR) - Audit PlanningDocumento9 páginasAt Quizzer (CPAR) - Audit Planningparakaybee100% (3)

- InvestmentGuide PDFDocumento2 páginasInvestmentGuide PDFMon CuiAinda não há avaliações

- CVP 2203workshopDocumento40 páginasCVP 2203workshopGelyn CruzAinda não há avaliações

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Definition of CreditDocumento7 páginasDefinition of CreditMon CuiAinda não há avaliações

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2219)

- Eco MidtermDocumento1 páginaEco MidtermMon CuiAinda não há avaliações

- wk53 Dec2016mktwatchDocumento3 páginaswk53 Dec2016mktwatchMon CuiAinda não há avaliações

- APA (American Psychological Association) Style Is Most Frequently Used Within The Social Sciences, in Order To Cite Various SourcesDocumento2 páginasAPA (American Psychological Association) Style Is Most Frequently Used Within The Social Sciences, in Order To Cite Various SourcesMon CuiAinda não há avaliações

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Definition of CreditDocumento7 páginasDefinition of CreditMon CuiAinda não há avaliações

- MA Div F 26-30 Case Study of Grasim LimitedDocumento9 páginasMA Div F 26-30 Case Study of Grasim LimitedSaiyam ShahAinda não há avaliações

- Chapter 7-The Revenue/Receivables/Cash Cycle: Multiple ChoiceDocumento32 páginasChapter 7-The Revenue/Receivables/Cash Cycle: Multiple ChoiceLeonardoAinda não há avaliações

- Maple Leaf Cement Factory Limited.Documento17 páginasMaple Leaf Cement Factory Limited.MubasharAinda não há avaliações

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (119)

- Dlca 1.B/D 2.sale 3.interest 4.dish0n0ur Cheque 1.cash Received 2.reurn 0utward 3.bad Debts 4. C0ntra Entry 5.C/DDocumento16 páginasDlca 1.B/D 2.sale 3.interest 4.dish0n0ur Cheque 1.cash Received 2.reurn 0utward 3.bad Debts 4. C0ntra Entry 5.C/DIqra HanifAinda não há avaliações

- J&J FS AnalysisDocumento5 páginasJ&J FS AnalysisEarl Justine FerrerAinda não há avaliações

- Product CostDocumento2 páginasProduct Costmba departmentAinda não há avaliações

- Lesson 1.1 - Construction Cost Control Basic CourseDocumento16 páginasLesson 1.1 - Construction Cost Control Basic Courseguy88Ainda não há avaliações

- 03 - HO - Statement of Comprehensive IncomeDocumento3 páginas03 - HO - Statement of Comprehensive IncomeYoung MetroAinda não há avaliações

- Tax-1 SyllabusDocumento16 páginasTax-1 SyllabusJennica Gyrl DelfinAinda não há avaliações

- Swinburne University Sarawak Campus Practice MCQs on Recording Business TransactionsDocumento11 páginasSwinburne University Sarawak Campus Practice MCQs on Recording Business TransactionsJordanAinda não há avaliações

- CapEx Definition ExplainedDocumento4 páginasCapEx Definition ExplainedMali MedoAinda não há avaliações

- Audit Materiality and TolerancesDocumento8 páginasAudit Materiality and TolerancesAlrac GarciaAinda não há avaliações

- Audit of Cash AssertionsDocumento13 páginasAudit of Cash AssertionsDanica GeneralaAinda não há avaliações

- GR 137377Documento19 páginasGR 137377jobelle barcellanoAinda não há avaliações

- Chapter 6 - Investment Evaluation (Engineering Economics)Documento53 páginasChapter 6 - Investment Evaluation (Engineering Economics)Bahredin AbdellaAinda não há avaliações

- Class Activity, Adjustments & WORK SHEETDocumento18 páginasClass Activity, Adjustments & WORK SHEETkhanAinda não há avaliações

- UV Health System LTAC Hospital Project Financial AnalysisDocumento4 páginasUV Health System LTAC Hospital Project Financial AnalysisSaiyed Anver Akhtar43% (7)

- Montee Company Income Statement For The Month Ended July 31, 2017 Debit Credit Revenue $ 6,150 Expenses $ 2,600 950 600 400 150 4,700 $1,450Documento3 páginasMontee Company Income Statement For The Month Ended July 31, 2017 Debit Credit Revenue $ 6,150 Expenses $ 2,600 950 600 400 150 4,700 $1,450Gerald DiazAinda não há avaliações

- Zydus Frontline New 4Documento1 páginaZydus Frontline New 4Sri Ganesh ComputersAinda não há avaliações

- Error Analysis Lowell Corporation Has Used The Accrual Basis of PDFDocumento1 páginaError Analysis Lowell Corporation Has Used The Accrual Basis of PDFAnbu jaromiaAinda não há avaliações

- Akuntansi p5Documento7 páginasAkuntansi p5Alche MistAinda não há avaliações

- Form 16: Ibm Daksh Business Process Services Pvt. LTDDocumento5 páginasForm 16: Ibm Daksh Business Process Services Pvt. LTDmadan mehtaAinda não há avaliações

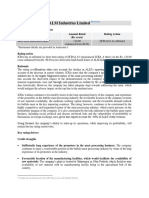

- ALM Industries Limited: Summary of Rated Instruments Instruments Amount Rated (Rs. Crore) Rating ActionDocumento6 páginasALM Industries Limited: Summary of Rated Instruments Instruments Amount Rated (Rs. Crore) Rating Actionsgr_kansagraAinda não há avaliações

- Partnership Operation: Acp 311 - UlobDocumento49 páginasPartnership Operation: Acp 311 - UlobMeleen TadenaAinda não há avaliações

- Dividend Policy at FPL Case 4Documento4 páginasDividend Policy at FPL Case 4Ankur280475% (4)

- Interest Expense - RR No. 13-00Documento8 páginasInterest Expense - RR No. 13-00美流Ainda não há avaliações

- ProblemsDocumento7 páginasProblemsHanna Mae Arcilla67% (6)

- Auditing Chapter 2 Part IIIDocumento3 páginasAuditing Chapter 2 Part IIIRegine A. AnsongAinda não há avaliações

- Pagcor V Bir GR 172087Documento16 páginasPagcor V Bir GR 172087LalaLanibaAinda não há avaliações

- SAP Internal Order: Conceptual Background and Usage For Harvey NormanDocumento15 páginasSAP Internal Order: Conceptual Background and Usage For Harvey NormanDeepesh100% (1)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)No EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Nota: 4.5 de 5 estrelas4.5/5 (12)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindNo EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindNota: 5 de 5 estrelas5/5 (231)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetNo EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetAinda não há avaliações

- Finance Basics (HBR 20-Minute Manager Series)No EverandFinance Basics (HBR 20-Minute Manager Series)Nota: 4.5 de 5 estrelas4.5/5 (32)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)No EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Nota: 4.5 de 5 estrelas4.5/5 (5)