Você também pode gostar

- Problems Faced by Accounting AcademicsDocumento7 páginasProblems Faced by Accounting AcademicsDrahneel MarasiganAinda não há avaliações

- Prospect For Accounting Academics - Examining The Effect of Undergraduate Students' Career Decision.Documento37 páginasProspect For Accounting Academics - Examining The Effect of Undergraduate Students' Career Decision.Louierose Joy CopreAinda não há avaliações

- Vocational Skills Gap in UK Accounting EducationDocumento34 páginasVocational Skills Gap in UK Accounting EducationadillahAinda não há avaliações

- Accounting Education: A Review of the Changes That Have Occurred in the Last Five YearsNo EverandAccounting Education: A Review of the Changes That Have Occurred in the Last Five YearsAinda não há avaliações

- Perceptions Accounting Major and Minor Students of Inductory Accounting CourseDocumento10 páginasPerceptions Accounting Major and Minor Students of Inductory Accounting Coursenicoleginesantonio30Ainda não há avaliações

- Accounting Curriculum Redesign: Improving Cpa Exam Pass-Rates at A Small UniversityDocumento14 páginasAccounting Curriculum Redesign: Improving Cpa Exam Pass-Rates at A Small Universitygreen helpersAinda não há avaliações

- 56.students Perception Towards Majoring in Accounting (Ida Haryanti) PP 405-412Documento8 páginas56.students Perception Towards Majoring in Accounting (Ida Haryanti) PP 405-412upenapahangAinda não há avaliações

- Accountants Embracing Changing Times in AcademeDocumento12 páginasAccountants Embracing Changing Times in AcademeLorie Anne ValleAinda não há avaliações

- ShortageofaccountingphdsDocumento10 páginasShortageofaccountingphdsRizwan M KhanAinda não há avaliações

- Title I. Group 2. Availability of Accounting ProfessionalsDocumento3 páginasTitle I. Group 2. Availability of Accounting ProfessionalsSEBASTIAN, JENNY LAinda não há avaliações

- Paper For A e Final VersionDocumento34 páginasPaper For A e Final VersionPASCUAL, CYREL, TABANGINAinda não há avaliações

- Current Opinions On Forensic Accounting Education: Bonita KramerDocumento16 páginasCurrent Opinions On Forensic Accounting Education: Bonita Kramerray roseAinda não há avaliações

- GENERIC SKILLS KEY FOR NEW ACCOUNTANTSDocumento15 páginasGENERIC SKILLS KEY FOR NEW ACCOUNTANTSRahulSheoranAinda não há avaliações

- Related ReviewDocumento4 páginasRelated ReviewJune Kathleen VillanuevaAinda não há avaliações

- Cover SheetDocumento24 páginasCover SheetMarck SitoAinda não há avaliações

- Accounting Students' Attitude Towads AccountingDocumento29 páginasAccounting Students' Attitude Towads AccountingSham Salonga Pascual50% (2)

- Proposal Business Students Perception of Accounting and Its Determinants2Documento19 páginasProposal Business Students Perception of Accounting and Its Determinants2Edith MartinAinda não há avaliações

- Factors That Impact Attrition and Retention Rates For Accountancy Diploma Students: Evidence From AustraliaDocumento23 páginasFactors That Impact Attrition and Retention Rates For Accountancy Diploma Students: Evidence From AustraliaYvone Claire Fernandez SalmorinAinda não há avaliações

- G7 - Senior High School Learners' Perception of Accountancy As A Career PathDocumento38 páginasG7 - Senior High School Learners' Perception of Accountancy As A Career PathMyke Andrei OpilacAinda não há avaliações

- Becoming A CPA: Evidence From Recent Graduates Kimberly Charron D. Jordan LoweDocumento18 páginasBecoming A CPA: Evidence From Recent Graduates Kimberly Charron D. Jordan LoweJonathan BausingAinda não há avaliações

- Differences in views on accounting techniquesDocumento20 páginasDifferences in views on accounting techniquesEth Fikir NatAinda não há avaliações

- Review of Related Literature and StudiesDocumento10 páginasReview of Related Literature and StudiesJaira May BustardeAinda não há avaliações

- Future Proofing Tomorrows Accounting GraduatesDocumento18 páginasFuture Proofing Tomorrows Accounting GraduatesSanti Azmi MursalinaAinda não há avaliações

- 'Senior High School Learners' Perception of Accountancy As A Career PathDocumento41 páginas'Senior High School Learners' Perception of Accountancy As A Career PathMyke Andrei OpilacAinda não há avaliações

- 13 Problem-Based Learning (PBL) Does Accounting Education Need It JAEd 2012 Final SubmissionDocumento47 páginas13 Problem-Based Learning (PBL) Does Accounting Education Need It JAEd 2012 Final SubmissionMochamad Sandi NofiansyahAinda não há avaliações

- Bookkeeping RRLDocumento25 páginasBookkeeping RRLMark TepaceAinda não há avaliações

- Gmac Roi AnalysisDocumento12 páginasGmac Roi AnalysisdecnovAinda não há avaliações

- The Effect of Government Policy On Education in The UKDocumento10 páginasThe Effect of Government Policy On Education in The UKJane MansellAinda não há avaliações

- Thesis, Performance 2Documento25 páginasThesis, Performance 2Jezmelyn Antimano60% (5)

- Intern, Previously Used in The Medical Profession To Define A Person With A Degree ButDocumento2 páginasIntern, Previously Used in The Medical Profession To Define A Person With A Degree ButAnonymous 5sETvwAinda não há avaliações

- BibleDocumento15 páginasBiblevannesseAinda não há avaliações

- Inquiries Investigation and Immersion Group 5Documento8 páginasInquiries Investigation and Immersion Group 5Gerlen MendozaAinda não há avaliações

- 1 PBDocumento11 páginas1 PBgiselleAinda não há avaliações

- Factors Associated with High Failure Rates in Accounting Courses: A Case Study of Omani StudentsDocumento14 páginasFactors Associated with High Failure Rates in Accounting Courses: A Case Study of Omani Studentsrichel sanchezAinda não há avaliações

- Accounting EducationDocumento16 páginasAccounting EducationcpacpacpaAinda não há avaliações

- Students' Perception of The Causes of Low Performance in Financial AccountingDocumento48 páginasStudents' Perception of The Causes of Low Performance in Financial AccountingJodie Sagdullas100% (2)

- Impacts of InternshipDocumento18 páginasImpacts of InternshipJonz AquinoAinda não há avaliações

- Manuscript ARTT 2020 PDFDocumento28 páginasManuscript ARTT 2020 PDFHenry James NepomucenoAinda não há avaliações

- PHINMA - Union College of Laguna A.Mabini ST., Sta. Cruz, Laguna, Santa Cruz, Philippines Bachelor of Science in AccountancyDocumento3 páginasPHINMA - Union College of Laguna A.Mabini ST., Sta. Cruz, Laguna, Santa Cruz, Philippines Bachelor of Science in AccountancyBryan TanAinda não há avaliações

- Awareness, Motivations and Readiness For Professional Accounting Education - A Case of Accounting Students in UiTM JohorDocumento10 páginasAwareness, Motivations and Readiness For Professional Accounting Education - A Case of Accounting Students in UiTM JohorfidelaluthfianaAinda não há avaliações

- Chapter IDocumento8 páginasChapter ISeokjin KimAinda não há avaliações

- Academic Performance of Accountancy GradDocumento19 páginasAcademic Performance of Accountancy GradJeanette Agustin Gonzales-EikawaAinda não há avaliações

- ACCOUNTING INFORMATION AND EMPLOYMENT - AliDocumento9 páginasACCOUNTING INFORMATION AND EMPLOYMENT - AliAsadulla KhanAinda não há avaliações

- Chapter 2 - LiteratureDocumento21 páginasChapter 2 - LiteratureDianne Mei Tagabi CastroAinda não há avaliações

- Business & AdministrationDocumento2 páginasBusiness & AdministrationHehshjjjjsjAinda não há avaliações

- Do Students' Perceptions Matter? A Study of The Effect of Students' Perceptions On Academic PerformanceDocumento24 páginasDo Students' Perceptions Matter? A Study of The Effect of Students' Perceptions On Academic PerformanceIris DescentAinda não há avaliações

- The Problem and Its BackgroundDocumento9 páginasThe Problem and Its BackgroundrpaldeonAinda não há avaliações

- 45.the Relationship Between Students' Perception and Intention (Anis Barieyah Mat Bahari) PP 327-332Documento6 páginas45.the Relationship Between Students' Perception and Intention (Anis Barieyah Mat Bahari) PP 327-332upenapahangAinda não há avaliações

- 6 Mohamed S. MDocumento8 páginas6 Mohamed S. MAshley MorganAinda não há avaliações

- Accounting Student Academic Dishonesty: What Accounting Faculty and Administrators Believe Douglas M. BoyleDocumento23 páginasAccounting Student Academic Dishonesty: What Accounting Faculty and Administrators Believe Douglas M. Boyle?????Ainda não há avaliações

- TTR Schoolstaffing 1Documento16 páginasTTR Schoolstaffing 1National Education Policy CenterAinda não há avaliações

- Causes of Students Failure in Financial Accounting in Senior Secondary Certificate Examination in Secondary Schools in Awka LgaDocumento73 páginasCauses of Students Failure in Financial Accounting in Senior Secondary Certificate Examination in Secondary Schools in Awka Lgajamessabraham2Ainda não há avaliações

- TTR Schoolstaffing 0Documento16 páginasTTR Schoolstaffing 0National Education Policy CenterAinda não há avaliações

- Student Academic PerformanceDocumento13 páginasStudent Academic PerformanceThalia SandersAinda não há avaliações

- Ref1.1 Accounting Learning in PhilippinesDocumento7 páginasRef1.1 Accounting Learning in PhilippinesRico Jay EmejasAinda não há avaliações

- abm students having hardtime Catching up with their Accounting SubjectsDocumento4 páginasabm students having hardtime Catching up with their Accounting SubjectsyhuijiexylieAinda não há avaliações

- Improving Written Skills in Accounting StudentsDocumento14 páginasImproving Written Skills in Accounting StudentsJay Pee EspirituAinda não há avaliações

- TTR SchoolstaffingDocumento16 páginasTTR SchoolstaffingNational Education Policy CenterAinda não há avaliações

- Factors Affecting Accountancy Students' Remote Learning During COVIDDocumento23 páginasFactors Affecting Accountancy Students' Remote Learning During COVIDedrianclydeAinda não há avaliações

- Time To Change Introductory AccountingDocumento5 páginasTime To Change Introductory AccountingthoritruongAinda não há avaliações

- (Ernst FDocumento2.031 páginas(Ernst Fitn_nti100% (1)

- Sap TablesDocumento29 páginasSap Tableslucaslu100% (14)

- Tire A PartDocumento13 páginasTire A Partitn_ntiAinda não há avaliações

- The Rules For Being Amazing PDFDocumento1 páginaThe Rules For Being Amazing PDFAkshay PrasathAinda não há avaliações

- Culture of FranceDocumento2 páginasCulture of Franceitn_ntiAinda não há avaliações

- Creation IndicatorDocumento2 páginasCreation Indicatoritn_ntiAinda não há avaliações

- Using MDM 7.1 Key-Mappings in A PI LandscapeDocumento40 páginasUsing MDM 7.1 Key-Mappings in A PI LandscapeshahrokhhassasianAinda não há avaliações

- Stock Transfer Configure DocumentDocumento7 páginasStock Transfer Configure DocumentSatyendra Gupta100% (1)

- Refrigerators, Best Refrigerators India, Compare Refrigerator BrandsDocumento3 páginasRefrigerators, Best Refrigerators India, Compare Refrigerator Brandsitn_ntiAinda não há avaliações

- SBI PO 17072011 AdvtDocumento3 páginasSBI PO 17072011 AdvtRupak NathAinda não há avaliações

- Work Immersion Career PreparationDocumento5 páginasWork Immersion Career PreparationAllysa Kim DumpAinda não há avaliações

- Essential criteria employee evaluationDocumento3 páginasEssential criteria employee evaluationMuhammad Hanis WafieyudinAinda não há avaliações

- Scope of WorkDocumento24 páginasScope of WorkGijo GeorgeAinda não há avaliações

- A Study On Employee Welfare Measures With Special Refference To Kitex LTD Kizhakkambalam Aluva 1384Documento7 páginasA Study On Employee Welfare Measures With Special Refference To Kitex LTD Kizhakkambalam Aluva 1384SULTANA TAJAinda não há avaliações

- Final Examinations Leadership and Management Name: - QUIJANO - Year/ Level: - Date/ TimeDocumento4 páginasFinal Examinations Leadership and Management Name: - QUIJANO - Year/ Level: - Date/ TimeARISAinda não há avaliações

- Succession Planning Practices and Their Impact On Employee RetentionDocumento80 páginasSuccession Planning Practices and Their Impact On Employee RetentionOUSMAN SEIDAinda não há avaliações

- IbmDocumento35 páginasIbmCyril ChettiarAinda não há avaliações

- NWPC vs Regional Tripartite Wages BoardDocumento2 páginasNWPC vs Regional Tripartite Wages BoardDeniece Loutchie A CorralAinda não há avaliações

- Institute For Construction Training and Development (ICTAD)Documento33 páginasInstitute For Construction Training and Development (ICTAD)Nuwan Sudharshana Weerathunga60% (5)

- Unit 2 d3Documento9 páginasUnit 2 d3api-359460355Ainda não há avaliações

- IJERT Critical Factors Influencing WorkDocumento3 páginasIJERT Critical Factors Influencing WorkAngelica MendozaAinda não há avaliações

- Cost Accounting Unit 2Documento75 páginasCost Accounting Unit 2lakshyajai70Ainda não há avaliações

- ED to Probe Flipkart, Bharti Walmart for FDI Norm ViolationsDocumento7 páginasED to Probe Flipkart, Bharti Walmart for FDI Norm ViolationsPrabhakar KumarAinda não há avaliações

- The Minimum Wages Act, 1948Documento40 páginasThe Minimum Wages Act, 1948Abha NagpalAinda não há avaliações

- Assessment FrameworkDocumento50 páginasAssessment FrameworkCharles OndiekiAinda não há avaliações

- Terminal ReportDocumento4 páginasTerminal ReportshamilleAinda não há avaliações

- Exports Impact On EconomyDocumento4 páginasExports Impact On EconomyjainchanchalAinda não há avaliações

- Reading and Writing Portfolio 3: Applying for a JobDocumento2 páginasReading and Writing Portfolio 3: Applying for a JobLeo AquinoAinda não há avaliações

- Nurses and Stress: Recognizing Causes and Seeking SolutionsDocumento10 páginasNurses and Stress: Recognizing Causes and Seeking SolutionsRAHMAT ALI PUTRAAinda não há avaliações

- Income Tax Law - A Capsule For Quick Recap IPCC Nov 18Documento28 páginasIncome Tax Law - A Capsule For Quick Recap IPCC Nov 18k moviesAinda não há avaliações

- Article 91. Right To Weekly Rest Day. It Shall Be The Duty of Every Employer, WhetherDocumento18 páginasArticle 91. Right To Weekly Rest Day. It Shall Be The Duty of Every Employer, WhetherApril Ann Sapinoso Bigay-PanghulanAinda não há avaliações

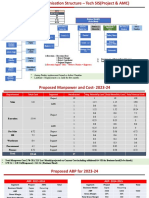

- Proposed Organisation Structure and Cost Projections for Tech SISDocumento5 páginasProposed Organisation Structure and Cost Projections for Tech SISSantosh KumarAinda não há avaliações

- HSHT Team Building Ice Breaker Manual 2008 09 PDFDocumento108 páginasHSHT Team Building Ice Breaker Manual 2008 09 PDFChris ChiangAinda não há avaliações

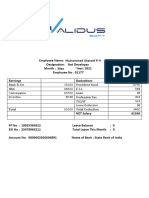

- Salary SlipDocumento4 páginasSalary Slipbindu mathaiAinda não há avaliações

- Decentralization Education PhilippinesDocumento34 páginasDecentralization Education PhilippinesDanvie Ryan Phi100% (4)

- TEF Business Management Training for African EntrepreneursDocumento21 páginasTEF Business Management Training for African EntrepreneursVictor EtudorAinda não há avaliações

- Annexure CD - 01': L T P/S SW/FW No. of Psda Total Credit UnitsDocumento4 páginasAnnexure CD - 01': L T P/S SW/FW No. of Psda Total Credit UnitsNitya SagarAinda não há avaliações

- Managing Culture at British Airways Hype, Hope and Reality PDFDocumento16 páginasManaging Culture at British Airways Hype, Hope and Reality PDF陆奕敏Ainda não há avaliações

- Washington SB 5599 (2023)Documento9 páginasWashington SB 5599 (2023)ThePoliticalHatAinda não há avaliações

- Quiz MB0038 Management Process and Organization Behaviour FinalDocumento63 páginasQuiz MB0038 Management Process and Organization Behaviour FinalSanehi RamAinda não há avaliações