Você também pode gostar

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- T03 - Working Capital FinanceDocumento39 páginasT03 - Working Capital FinanceJesha Jotojot100% (1)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Financial PlanningDocumento119 páginasFinancial PlanningUmang Jain100% (1)

- Asset and Equity VolatilitiesDocumento40 páginasAsset and Equity Volatilitiescorporateboy36596Ainda não há avaliações

- Wealth Management & Asset ManagementDocumento32 páginasWealth Management & Asset ManagementVineetChandakAinda não há avaliações

- Power Exchange OperationDocumento114 páginasPower Exchange OperationNRLDCAinda não há avaliações

- 335872Documento7 páginas335872pradhan13Ainda não há avaliações

- Retail ManagementDocumento115 páginasRetail Managementarora08sumit71% (7)

- 7.1 Paculdo Vs Regalado DigestDocumento2 páginas7.1 Paculdo Vs Regalado Digesthectorjr100% (2)

- Law 4Documento2 páginasLaw 4Jesha JotojotAinda não há avaliações

- Civil Law Reviewer by JuradoDocumento340 páginasCivil Law Reviewer by JuradoGlyza Kaye Zorilla Patiag92% (13)

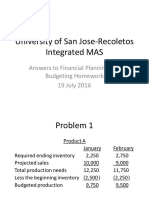

- IntegMAS HO 008 Homework AnswersDocumento17 páginasIntegMAS HO 008 Homework AnswersJesha JotojotAinda não há avaliações

- T03 - Working Capital FinanceDocumento40 páginasT03 - Working Capital FinanceJesha JotojotAinda não há avaliações

- FinalDocumento1 páginaFinalJesha JotojotAinda não há avaliações

- Own Mock QualiDocumento10 páginasOwn Mock QualiDarwin John SantosAinda não há avaliações

- Excel Academy of CommerceDocumento2 páginasExcel Academy of CommerceHassan Jameel SheikhAinda não há avaliações

- Meaning of Business: Art. 1767, New Civil Code of The Philippines Sec.2 B.P. 68 or Corporation Code of The PhilippinesDocumento25 páginasMeaning of Business: Art. 1767, New Civil Code of The Philippines Sec.2 B.P. 68 or Corporation Code of The PhilippinesAnali BarbonAinda não há avaliações

- Unit 21 Private Equity and Venture CapitalDocumento10 páginasUnit 21 Private Equity and Venture CapitalHari RajAinda não há avaliações

- Curtain InvoiceDocumento1 páginaCurtain Invoicebilalahmad566Ainda não há avaliações

- Oct 3rd Week Details (Eng) by AffairsCloudDocumento27 páginasOct 3rd Week Details (Eng) by AffairsCloudAniket ZunkeAinda não há avaliações

- A Study On Customer Satisfaction of Reliance Life InsuranceDocumento57 páginasA Study On Customer Satisfaction of Reliance Life InsuranceRishabh PandeAinda não há avaliações

- Supreme Court rules on banking operations without authorityDocumento45 páginasSupreme Court rules on banking operations without authorityJustice PajarilloAinda não há avaliações

- Kind of Stock BrokersDocumento4 páginasKind of Stock BrokersImran HassanAinda não há avaliações

- Working Capital Management and Banks' Performance: Evidence From IndiaDocumento13 páginasWorking Capital Management and Banks' Performance: Evidence From Indiaboby.prashantkumar.boby066Ainda não há avaliações

- Maintain Data Origin TypeDocumento6 páginasMaintain Data Origin Typeshiva_1912-1Ainda não há avaliações

- Indebted Isko: Philippine CollegianDocumento12 páginasIndebted Isko: Philippine CollegianPhilippine CollegianAinda não há avaliações

- Financial Management Part 3 UpdatedDocumento65 páginasFinancial Management Part 3 UpdatedMarielle Ace Gole CruzAinda não há avaliações

- 028 Ptrs Modul Matematik t4 Sel-96-99Documento4 páginas028 Ptrs Modul Matematik t4 Sel-96-99mardhiah88Ainda não há avaliações

- The Concepts and Practice of Mathematical Finance: Second EditionDocumento8 páginasThe Concepts and Practice of Mathematical Finance: Second EditionChâu GiangAinda não há avaliações

- Malaysian Trustee Incorporation Act SummaryDocumento19 páginasMalaysian Trustee Incorporation Act SummarySchen NgAinda não há avaliações

- FFM Chapter 8Documento5 páginasFFM Chapter 8Dawn CaldeiraAinda não há avaliações

- Tax 2 4Documento9 páginasTax 2 4amlecdeyojAinda não há avaliações

- Mishkin Econ13e PPT 11Documento39 páginasMishkin Econ13e PPT 11hangbg2k3Ainda não há avaliações

- National Highways Authority of India (Nhai) DeputyDocumento1 páginaNational Highways Authority of India (Nhai) DeputyHarsh RanjanAinda não há avaliações

- Chapter 6 Mental AccountingDocumento6 páginasChapter 6 Mental AccountingAbdulAinda não há avaliações

- Eurobonds: Euro BondsDocumento5 páginasEurobonds: Euro BondssuperjagdishAinda não há avaliações

- Jaffar and Musa (2013) PDFDocumento10 páginasJaffar and Musa (2013) PDFMohamed FAKHFEKHAinda não há avaliações