Você também pode gostar

- Ibps Clerk 2015 Application Fees ReceiptDocumento1 páginaIbps Clerk 2015 Application Fees ReceiptAsim JavedAinda não há avaliações

- Saif Ullah Khan: ObjectiveDocumento3 páginasSaif Ullah Khan: ObjectiveAsim JavedAinda não há avaliações

- Jpqr9l104xgdt5lvxacedw IV GP PyslpDocumento1 páginaJpqr9l104xgdt5lvxacedw IV GP PyslpAsim JavedAinda não há avaliações

- UPSSSC Revenue Inspector Registration SlipDocumento1 páginaUPSSSC Revenue Inspector Registration SlipAsim JavedAinda não há avaliações

- ) /"2 B . - '.,r. L (,.fli) T J: - 6otffi""drt"jf"'u'" - ) I "-, N /s-U, GDocumento1 página) /"2 B . - '.,r. L (,.fli) T J: - 6otffi""drt"jf"'u'" - ) I "-, N /s-U, GAsim JavedAinda não há avaliações

- Ordinary PostDocumento1 páginaOrdinary PostAsim JavedAinda não há avaliações

- Requirements For CADocumento5 páginasRequirements For CAKunwar Shivpal SinghAinda não há avaliações

- Resume - CA7 SchedulerDocumento5 páginasResume - CA7 SchedulerAsim JavedAinda não há avaliações

- z/OS MVS JCL IntermediateDocumento73 páginasz/OS MVS JCL IntermediateasimAinda não há avaliações

- z/OS MVS JCL IntermediateDocumento80 páginasz/OS MVS JCL IntermediateasimAinda não há avaliações

- SR Software Engineer-Mainframes - C1Documento3 páginasSR Software Engineer-Mainframes - C1Asim JavedAinda não há avaliações

- z/OS MVS JCL IntermediateDocumento61 páginasz/OS MVS JCL IntermediateasimAinda não há avaliações

- z/OS MVS JCL IntermediateDocumento58 páginasz/OS MVS JCL IntermediateasimAinda não há avaliações

- SQL QueriesDocumento32 páginasSQL QueriesAmarnath ReddyAinda não há avaliações

- z/OS MVS JCL IntermediateDocumento70 páginasz/OS MVS JCL IntermediateasimAinda não há avaliações

- Code of Ethics Revisionary StatementsDocumento3 páginasCode of Ethics Revisionary StatementsAsim JavedAinda não há avaliações

- z/OS MVS JCL IntermediateDocumento58 páginasz/OS MVS JCL IntermediateasimAinda não há avaliações

- AS400 Job Scheduler PDFDocumento183 páginasAS400 Job Scheduler PDFAsim JavedAinda não há avaliações

- Audit report drafting and auditor independence issuesDocumento4 páginasAudit report drafting and auditor independence issuesAsim JavedAinda não há avaliações

- Application Form IOCLDocumento2 páginasApplication Form IOCLAsim JavedAinda não há avaliações

- Commerce - ObjectivesDocumento28 páginasCommerce - ObjectivesAsim JavedAinda não há avaliações

- Ind As Summary For Amendment ClassesDocumento29 páginasInd As Summary For Amendment ClassesAsim JavedAinda não há avaliações

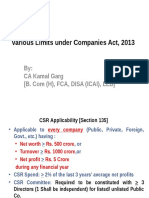

- Various Limits Under Companies Act, 2013 (CA Final)Documento61 páginasVarious Limits Under Companies Act, 2013 (CA Final)Asim JavedAinda não há avaliações

- Corporate and Allied Laws Solution For November 2016 Practice PaperDocumento14 páginasCorporate and Allied Laws Solution For November 2016 Practice PaperAsim JavedAinda não há avaliações

- CARO 2016 For CA FinalDocumento19 páginasCARO 2016 For CA FinalAsim JavedAinda não há avaliações

- SARFAESI Act in Layman WordsDocumento2 páginasSARFAESI Act in Layman WordsAsim Javed100% (1)

- Microsoft Word - Practice Paper On Corporate and Allied Laws For CA Final November 2016 ExaminationDocumento6 páginasMicrosoft Word - Practice Paper On Corporate and Allied Laws For CA Final November 2016 ExaminationAsim JavedAinda não há avaliações

- Ind AS Solutions For CA Final Class - PPSXDocumento50 páginasInd AS Solutions For CA Final Class - PPSXAsim JavedAinda não há avaliações

- List of Harmony Involved in Standards On Auditing and Companies Act, 2013Documento1 páginaList of Harmony Involved in Standards On Auditing and Companies Act, 2013Asim JavedAinda não há avaliações

- Ind As Summary For Amendment ClassesDocumento29 páginasInd As Summary For Amendment ClassesAsim JavedAinda não há avaliações

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (119)