Você também pode gostar

- Chapter-2: Review OF LiteratureDocumento36 páginasChapter-2: Review OF Literaturekanna_dhasan25581Ainda não há avaliações

- An Empirical Study of Profitability Analysis of Selected Steel Companies in IndiaDocumento17 páginasAn Empirical Study of Profitability Analysis of Selected Steel Companies in Indiamuktisolia17Ainda não há avaliações

- 65-Article Text-171-1-10-20200331Documento6 páginas65-Article Text-171-1-10-20200331mia muchia desdaAinda não há avaliações

- Financial Radio Analysis-AmbujaDocumento94 páginasFinancial Radio Analysis-Ambujak eswariAinda não há avaliações

- INSPIRA JOURNAL OF COMMERCEECONOMICS COMPUTER SCIENCEJCECS Vol 04 N0 04 Oct Dec 2018 Pages 181 To 187Documento7 páginasINSPIRA JOURNAL OF COMMERCEECONOMICS COMPUTER SCIENCEJCECS Vol 04 N0 04 Oct Dec 2018 Pages 181 To 187Aman RoyAinda não há avaliações

- Research Methodology and ObjectivesDocumento10 páginasResearch Methodology and ObjectivesSovin ChauhanAinda não há avaliações

- Impact of Free Cash Flow on ProfitabilityDocumento15 páginasImpact of Free Cash Flow on Profitabilitysajid gulAinda não há avaliações

- Profitability Analysis: CHADARGHAT Hyderabad TelanganaDocumento10 páginasProfitability Analysis: CHADARGHAT Hyderabad TelanganakhayyumAinda não há avaliações

- Working Capital Management and Profitability: A Study On Cement Industry in BangladeshDocumento12 páginasWorking Capital Management and Profitability: A Study On Cement Industry in BangladeshSudip BaruaAinda não há avaliações

- Evaluating The Impact of Working Capital Management Components On Corporate Profitability: Evidence From Indian Manufacturing FirmsDocumento10 páginasEvaluating The Impact of Working Capital Management Components On Corporate Profitability: Evidence From Indian Manufacturing FirmsderihoodAinda não há avaliações

- Measuring Financial Health of A Public Limited Company Using Z' Score Model - A Case StudyDocumento18 páginasMeasuring Financial Health of A Public Limited Company Using Z' Score Model - A Case Studytrinanjan bhowalAinda não há avaliações

- Asset Management that Affects Profit Quality Industrial Product Group in the Stock Exchange of ThailandDocumento10 páginasAsset Management that Affects Profit Quality Industrial Product Group in the Stock Exchange of ThailandInternational Journal of Innovative Science and Research TechnologyAinda não há avaliações

- 145-Article Text-429-1-10-20210803Documento12 páginas145-Article Text-429-1-10-20210803(FPTU HCM) Phạm Anh Thiện TùngAinda não há avaliações

- The Impact of Capital Structure On The Profitability of Publicly Traded Manufacturing Firms in BangladeshDocumento5 páginasThe Impact of Capital Structure On The Profitability of Publicly Traded Manufacturing Firms in BangladeshAnonymous XIwe3KKAinda não há avaliações

- Value Added and Financial Performance: A Case Study of Listed Manufacturing Companies in Sri LankaDocumento13 páginasValue Added and Financial Performance: A Case Study of Listed Manufacturing Companies in Sri LankaOilandGas IndependentProjectAinda não há avaliações

- Information SystemDocumento15 páginasInformation SystemSudip BaruaAinda não há avaliações

- E3sconf Pdsed2023 05005Documento12 páginasE3sconf Pdsed2023 05005opentp2002Ainda não há avaliações

- Organizational Study on Profitability of Travancore Cochin Chemicals LtdDocumento106 páginasOrganizational Study on Profitability of Travancore Cochin Chemicals Ltdsavitha satheesanAinda não há avaliações

- WCM and Profitability in Textiles IndustryDocumento18 páginasWCM and Profitability in Textiles IndustryMahesh BendigeriAinda não há avaliações

- Financial Statement'Documento55 páginasFinancial Statement'mukesh lingamAinda não há avaliações

- Study the Relationship between Financial Ratios and Profitability to Market Value of Companies Listed on the Stock Exchange of Thailand. Resource Industry Group Energy and Utilities CategoryDocumento12 páginasStudy the Relationship between Financial Ratios and Profitability to Market Value of Companies Listed on the Stock Exchange of Thailand. Resource Industry Group Energy and Utilities CategoryInternational Journal of Innovative Science and Research TechnologyAinda não há avaliações

- Running Head: Influence of ProfitabilityDocumento14 páginasRunning Head: Influence of ProfitabilityYayu KersaAinda não há avaliações

- SSRN Id4730116Documento12 páginasSSRN Id4730116rochdi.keffalaAinda não há avaliações

- Financial Performance of Cement Companies in TamilnaduDocumento6 páginasFinancial Performance of Cement Companies in TamilnaduShrirang LichadeAinda não há avaliações

- Full ProjectDocumento55 páginasFull ProjectPRIYAM XEROXAinda não há avaliações

- Analysis of The Financial Performance of Processors and Glass Applications "Yoonly Glass"Documento6 páginasAnalysis of The Financial Performance of Processors and Glass Applications "Yoonly Glass"aijbmAinda não há avaliações

- Abhinav: International Monthly Refereed Journal of Research in Management & TechnologyDocumento6 páginasAbhinav: International Monthly Refereed Journal of Research in Management & TechnologymgajenAinda não há avaliações

- RONIN petroleum performance evaluation using trend percentageDocumento36 páginasRONIN petroleum performance evaluation using trend percentageRayan ShamsadenAinda não há avaliações

- An Empirical Study of Profitability Anal PDFDocumento12 páginasAn Empirical Study of Profitability Anal PDFsurajcool999Ainda não há avaliações

- iJARS 520Documento16 páginasiJARS 520Sasi KumarAinda não há avaliações

- Submitted By: Project Submitted in Partial Fulfillment For The Award of Degree ofDocumento21 páginasSubmitted By: Project Submitted in Partial Fulfillment For The Award of Degree ofMOHAMMED KHAYYUMAinda não há avaliações

- KBL ProjectDocumento63 páginasKBL ProjectSunil Darak100% (1)

- Variabel FundamentalDocumento11 páginasVariabel FundamentalMurphy HeideggerAinda não há avaliações

- UntitledDocumento68 páginasUntitledSurendra SkAinda não há avaliações

- Literature Review on Financial Performance and Profitability of BanksDocumento17 páginasLiterature Review on Financial Performance and Profitability of Bankssheleftme100% (3)

- Anisha Corrected ProposalDocumento7 páginasAnisha Corrected ProposalSajina DhunganaAinda não há avaliações

- Term Paper Insurance CompanyDocumento24 páginasTerm Paper Insurance CompanyartusharAinda não há avaliações

- The Efficiency of Financial Ratios Analysis To Evaluate Company'S ProfitabilityDocumento15 páginasThe Efficiency of Financial Ratios Analysis To Evaluate Company'S Profitabilityfaizal1229Ainda não há avaliações

- Profitabulity Analysis - PDF IntroductionDocumento87 páginasProfitabulity Analysis - PDF IntroductionUsha Rani Vajroj100% (1)

- 09 - Chapter 2Documento32 páginas09 - Chapter 2Apoorva A NAinda não há avaliações

- Evaluation of Financial Performance Using Value Addition Metrics - A Select Study of 'It' Companies in IndiaDocumento6 páginasEvaluation of Financial Performance Using Value Addition Metrics - A Select Study of 'It' Companies in IndiaAnonymous CwJeBCAXpAinda não há avaliações

- A Comparative Study On Performance of ITC Hotels and Taj Hotels LTD From 2013-2017 Using Leverage and TrendDocumento5 páginasA Comparative Study On Performance of ITC Hotels and Taj Hotels LTD From 2013-2017 Using Leverage and TrendPragya Singh BaghelAinda não há avaliações

- Project Report Sem 4 BbaDocumento43 páginasProject Report Sem 4 BbaTanya RajaniAinda não há avaliações

- The Theoretical Aspect of Profit and Profitability AnalysisDocumento8 páginasThe Theoretical Aspect of Profit and Profitability AnalysisAlison VelozAinda não há avaliações

- IJRPR18248Documento5 páginasIJRPR18248mudrankiagrawalAinda não há avaliações

- 1326-Article Text-1446-1-10-20160730 PDFDocumento5 páginas1326-Article Text-1446-1-10-20160730 PDFbare fruitAinda não há avaliações

- SSRN Id3289616Documento6 páginasSSRN Id3289616Harshit SharmaAinda não há avaliações

- Exploring The Link Between Operational Efficiency and Firms' Financial Performance An Empirical Evidence From The Ghana Stock Exchange GSEDocumento7 páginasExploring The Link Between Operational Efficiency and Firms' Financial Performance An Empirical Evidence From The Ghana Stock Exchange GSEEditor IJTSRDAinda não há avaliações

- Financial Health of NFCL - A Z-Model ApproachDocumento6 páginasFinancial Health of NFCL - A Z-Model ApproachDebosmita SinhaAinda não há avaliações

- Reliance Industries Financial Report AnalysisDocumento52 páginasReliance Industries Financial Report Analysissagar029Ainda não há avaliações

- Public Sector Bank Profitability and Efficiency StudyDocumento22 páginasPublic Sector Bank Profitability and Efficiency StudykizieAinda não há avaliações

- NPM and EPS Effect on Stock PricesDocumento9 páginasNPM and EPS Effect on Stock PricesNUR SARAH 'ALIAH HAIRUL AZHARAinda não há avaliações

- Impact of Working Capital Management On Profitability: A Case of Pakistan Textile IndustryDocumento4 páginasImpact of Working Capital Management On Profitability: A Case of Pakistan Textile IndustryUmar AbbasAinda não há avaliações

- The Efficiency of Financial Ratios Analysis To Evaluate Company'S ProfitabilityDocumento15 páginasThe Efficiency of Financial Ratios Analysis To Evaluate Company'S ProfitabilityadssdasdsadAinda não há avaliações

- Parv - Himanshu.finance ..Documento25 páginasParv - Himanshu.finance ..HIMANSHU GOYALAinda não há avaliações

- Final Project Final Work 222222222222Documento61 páginasFinal Project Final Work 222222222222kwame1986Ainda não há avaliações

- Project On Private Label of "Shopper Stop Limited": ContentDocumento11 páginasProject On Private Label of "Shopper Stop Limited": ContentRakesh SamariyaAinda não há avaliações

- Fund Management and Profitability With Reference To APMDCDocumento5 páginasFund Management and Profitability With Reference To APMDCthesijAinda não há avaliações

- 188-Article Text-627-1-10-20210218Documento7 páginas188-Article Text-627-1-10-20210218vansaj pandeyAinda não há avaliações

- Financial Statement Analysis Study Resource for CIMA & ACCA Students: CIMA Study ResourcesNo EverandFinancial Statement Analysis Study Resource for CIMA & ACCA Students: CIMA Study ResourcesAinda não há avaliações

- Bdo BranchesDocumento43 páginasBdo BranchesJohn Carlo ChomatogAinda não há avaliações

- Government Grants: Responsi UTS Akkeu 2Documento7 páginasGovernment Grants: Responsi UTS Akkeu 2Angel Valentine TirayoAinda não há avaliações

- Filipinas Port ServicesDocumento8 páginasFilipinas Port ServicesLiezl Oreilly VillanuevaAinda não há avaliações

- Kap 4 Parimet EkontabilitetitDocumento18 páginasKap 4 Parimet EkontabilitetitEdmond KeraAinda não há avaliações

- Kraft and CadburyDocumento2 páginasKraft and CadburyRezaHakimAinda não há avaliações

- New York State Urban Development Corporation D/b/a Empire State DevelopmentDocumento166 páginasNew York State Urban Development Corporation D/b/a Empire State DevelopmentjspectorAinda não há avaliações

- An Investigation Into The Dividend Policy of Firms in East AsiaDocumento53 páginasAn Investigation Into The Dividend Policy of Firms in East AsiaEvvone Ling Yee FengAinda não há avaliações

- List of Commercial Banks in KenyaDocumento4 páginasList of Commercial Banks in KenyaJarida La UongoAinda não há avaliações

- Taxation in India Vs AfghanistanDocumento11 páginasTaxation in India Vs AfghanistanKomal AgrawalAinda não há avaliações

- A Report On Merchant Banking and Portfolio Management Rules: A Comparison of Bangladesh and IndiaDocumento49 páginasA Report On Merchant Banking and Portfolio Management Rules: A Comparison of Bangladesh and IndiaYeasir ArafatAinda não há avaliações

- Missing Miles Request Form enDocumento2 páginasMissing Miles Request Form enazrarajanAinda não há avaliações

- TAXATION QUESTIONS & ANSWERSDocumento49 páginasTAXATION QUESTIONS & ANSWERSMarc ToresAinda não há avaliações

- Contact Sushant Kumar Add Sushant Kumar To Your NetworkDocumento2 páginasContact Sushant Kumar Add Sushant Kumar To Your NetworkJaspreet Singh SahaniAinda não há avaliações

- Business Forum: Lipstick Won't Help This Pig: Valerie GundersonDocumento3 páginasBusiness Forum: Lipstick Won't Help This Pig: Valerie GundersonValerie MartinAinda não há avaliações

- Nord Gold: New Kid On The BlockDocumento34 páginasNord Gold: New Kid On The Blocksovereign01Ainda não há avaliações

- 20th Koeberg 15km race results from 22 February 2014Documento32 páginas20th Koeberg 15km race results from 22 February 2014abstickleAinda não há avaliações

- Mandatory ELearning CIRCULAR+FOR+2016-17Documento8 páginasMandatory ELearning CIRCULAR+FOR+2016-17Urmi SenAinda não há avaliações

- Case Study Cola Wars in ChinaDocumento5 páginasCase Study Cola Wars in ChinalumiradutAinda não há avaliações

- Salary Bills (Pa)Documento72 páginasSalary Bills (Pa)MD.khalilAinda não há avaliações

- Dann Corporation Working Balance Sheet Decemeber 31, 2016Documento12 páginasDann Corporation Working Balance Sheet Decemeber 31, 2016Ne BzAinda não há avaliações

- F Annual Report 2011 ITDocumento164 páginasF Annual Report 2011 ITwarun88Ainda não há avaliações

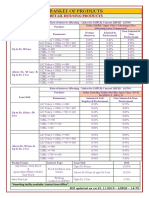

- BASKET OF RETAIL PRODUCTS RATESDocumento3 páginasBASKET OF RETAIL PRODUCTS RATESVirendra K VermaAinda não há avaliações

- About SonyDocumento4 páginasAbout SonyMoon HassanAinda não há avaliações

- Fake Nigerian Offer For Petrol IPCCDocumento16 páginasFake Nigerian Offer For Petrol IPCCDani NIANGAinda não há avaliações

- CSR 7-11Documento16 páginasCSR 7-11Genepearl Divinagracia100% (1)

- Understanding the Amended BBBEE FrameworkDocumento12 páginasUnderstanding the Amended BBBEE FrameworkCorey AcevedoAinda não há avaliações

- Organizational Plan:: Form of OwnershipDocumento3 páginasOrganizational Plan:: Form of OwnershiphibaAinda não há avaliações

- Orgs ExistDocumento15 páginasOrgs ExistFiroz AminAinda não há avaliações

- Ias 27 KPMGDocumento16 páginasIas 27 KPMGAgha AsadAinda não há avaliações

- Otis - FujitecDocumento2 páginasOtis - Fujitecapi-249461242Ainda não há avaliações