Você também pode gostar

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

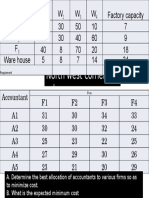

- Exam - Final - 11Documento7 páginasExam - Final - 11Yusuf HusseinAinda não há avaliações

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Except The: Income Sharing RatioDocumento1 páginaExcept The: Income Sharing RatioYusuf HusseinAinda não há avaliações

- Resource Usage: Issues Covered in This ChapterDocumento21 páginasResource Usage: Issues Covered in This ChapterYusuf HusseinAinda não há avaliações

- QuizzDocumento1 páginaQuizzYusuf HusseinAinda não há avaliações

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Lec 1 - Introduction To Wireless CommunicationDocumento60 páginasLec 1 - Introduction To Wireless CommunicationYusuf HusseinAinda não há avaliações

- RSH - Qam11 - Excel and Excel QM Explsm2010Documento153 páginasRSH - Qam11 - Excel and Excel QM Explsm2010Yusuf HusseinAinda não há avaliações

- Exam 2 Sample SolutionDocumento6 páginasExam 2 Sample SolutionYusuf HusseinAinda não há avaliações

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Example DVDDocumento17 páginasExample DVDYusuf HusseinAinda não há avaliações

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Data and Process Modeling: Husein OsmanDocumento17 páginasData and Process Modeling: Husein OsmanYusuf HusseinAinda não há avaliações

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- Lesson ThreeDocumento14 páginasLesson ThreeYusuf HusseinAinda não há avaliações

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Yaaqshiid: 1 Xaafadaha, Laamaha Iyo Waax-AhaDocumento4 páginasYaaqshiid: 1 Xaafadaha, Laamaha Iyo Waax-AhaYusuf HusseinAinda não há avaliações

- Chapter Four: Entering Beginning BalancesDocumento4 páginasChapter Four: Entering Beginning BalancesYusuf HusseinAinda não há avaliações

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Sample Solution: Midterm Exam - 300 PointsDocumento4 páginasSample Solution: Midterm Exam - 300 PointsYusuf HusseinAinda não há avaliações

- MSci331 - Simplex and Big MDocumento34 páginasMSci331 - Simplex and Big MYusuf HusseinAinda não há avaliações

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- CH 3 Accounting For Mudharabah Financing 1Documento32 páginasCH 3 Accounting For Mudharabah Financing 1Yusuf Hussein40% (5)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- Chapter EightDocumento11 páginasChapter EightYusuf HusseinAinda não há avaliações

- Chapter 1Documento29 páginasChapter 1Yusuf Hussein100% (2)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- Key Concepts: Week 5 Lesson 3: Economic Order Quantity (EOQ) ExtensionsDocumento5 páginasKey Concepts: Week 5 Lesson 3: Economic Order Quantity (EOQ) ExtensionsYusuf HusseinAinda não há avaliações

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Capital BudgetDocumento124 páginasCapital BudgetYusuf HusseinAinda não há avaliações

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Solution of Assignment Eco-04 Case: Mike (The Plumber) - A True StoryDocumento5 páginasSolution of Assignment Eco-04 Case: Mike (The Plumber) - A True StoryYusuf HusseinAinda não há avaliações

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Binomial Distribution WorksheetDocumento2 páginasBinomial Distribution WorksheetYusuf Hussein100% (1)

- COB291, Section - or Time of Class - Home Work Decision AnalysisDocumento8 páginasCOB291, Section - or Time of Class - Home Work Decision AnalysisYusuf HusseinAinda não há avaliações

- X P (X) XP (X) (X - E (X) ) P (X) : To See The Formulas, Hold Down The CTRL Key and Press The ' (Grave Accent) KeyDocumento7 páginasX P (X) XP (X) (X - E (X) ) P (X) : To See The Formulas, Hold Down The CTRL Key and Press The ' (Grave Accent) KeyYusuf HusseinAinda não há avaliações

- Research Methods - STA630 Spring 2007 Assignment 05Documento2 páginasResearch Methods - STA630 Spring 2007 Assignment 05Yusuf HusseinAinda não há avaliações

- CH I Introudction AISDocumento11 páginasCH I Introudction AISYusuf HusseinAinda não há avaliações

- Chapter 6 AnswersDocumento8 páginasChapter 6 AnswersYusuf HusseinAinda não há avaliações

- Chapter 6 Cost AccountingDocumento12 páginasChapter 6 Cost AccountingYusuf HusseinAinda não há avaliações

- Succeed With Facebook During Mega Sale EventsDocumento6 páginasSucceed With Facebook During Mega Sale EventsTanzir TanimAinda não há avaliações

- Evidencia 2 - Workshop "Distribution Channels"Documento6 páginasEvidencia 2 - Workshop "Distribution Channels"ChechoVegaAinda não há avaliações

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Chapter 2Documento2 páginasChapter 2Gaurav ChaudharyAinda não há avaliações

- 7 Figure Copywriting - Sales Page ChecklistDocumento2 páginas7 Figure Copywriting - Sales Page ChecklistDynamic Creations100% (1)

- Molly Von Eschenbach ResumeDocumento1 páginaMolly Von Eschenbach ResumeMolly von EschenbachAinda não há avaliações

- Market Anaysis MarigoldDocumento32 páginasMarket Anaysis MarigoldAh Hui23% (13)

- Chap09 RevenueDocumento7 páginasChap09 RevenueJohn Glenn LambayonAinda não há avaliações

- ACC301 Auditing NotesDocumento19 páginasACC301 Auditing NotesShakeel AhmedAinda não há avaliações

- P6-18 Unrealized Profit On Upstream SalesDocumento4 páginasP6-18 Unrealized Profit On Upstream Salesw3n123Ainda não há avaliações

- ASSIGNMENTDocumento2 páginasASSIGNMENTKomal KapilAinda não há avaliações

- Financial Analysis of MicrosoftDocumento7 páginasFinancial Analysis of MicrosoftDavid RiveraAinda não há avaliações

- Buisness Model ReinventionDocumento18 páginasBuisness Model ReinventionFaraz AkhtarAinda não há avaliações

- 11-03 TB Value Chains and BPs - WolfDocumento3 páginas11-03 TB Value Chains and BPs - WolfPrakash PandeyAinda não há avaliações

- Introduction and Axioms of Urban Economics: Mcgraw-Hill/Irwin ©2009 The Mcgraw-Hill Companies, All Rights ReservedDocumento23 páginasIntroduction and Axioms of Urban Economics: Mcgraw-Hill/Irwin ©2009 The Mcgraw-Hill Companies, All Rights ReservedSixd WaznineAinda não há avaliações

- Socrative QuizDocumento1 páginaSocrative Quizapi-307974839Ainda não há avaliações

- Sam SegmentationDocumento7 páginasSam SegmentationSameer SharmaAinda não há avaliações

- Avion Case StudyDocumento5 páginasAvion Case StudyAnurag GauraitraAinda não há avaliações

- 2024 Grade 12 Controlled Test MG 1 2Documento4 páginas2024 Grade 12 Controlled Test MG 1 2Zenzele100% (1)

- Investment Policy StatementDocumento5 páginasInvestment Policy StatementKenya HunterAinda não há avaliações

- Chapter 11: Inventory Cost Flow Cost Formula PAS 2, Paragraph 25 States That The Cost of Inventory Should Be A. Fifo B. Weighted AverageDocumento7 páginasChapter 11: Inventory Cost Flow Cost Formula PAS 2, Paragraph 25 States That The Cost of Inventory Should Be A. Fifo B. Weighted AverageYami HeatherAinda não há avaliações

- Strategic Brand Concept-ImageDocumento2 páginasStrategic Brand Concept-ImageMadalina ZamfirAinda não há avaliações

- Quiz 6 SolDocumento2 páginasQuiz 6 SolimagineimfAinda não há avaliações

- Acctg 2 - 2nd MimeoDocumento4 páginasAcctg 2 - 2nd MimeoJon Dumagil Inocentes, CPAAinda não há avaliações

- Lays Marketing ProjectDocumento18 páginasLays Marketing ProjectCharanjeet SinghAinda não há avaliações

- Marketing of Luxury of GoodsDocumento2 páginasMarketing of Luxury of GoodsDullStar MOTOAinda não há avaliações

- CHAPTER 3 - The Revised Chart of AccountsDocumento16 páginasCHAPTER 3 - The Revised Chart of AccountsRafael VictoriaAinda não há avaliações

- Acquisitions and Restructuring StrategiesDocumento31 páginasAcquisitions and Restructuring StrategiesYber LexAinda não há avaliações

- Template Dan LatiihanDocumento11 páginasTemplate Dan Latiihanlaurentinus fikaAinda não há avaliações

- Does Visual Merchandising, Store Atmosphere and Private Label Product Influence Impulse Buying? Evidence in JakartaDocumento9 páginasDoes Visual Merchandising, Store Atmosphere and Private Label Product Influence Impulse Buying? Evidence in Jakartahari karyadiAinda não há avaliações

- Test Bank For Principles of Corporate Finance 9th Edition Richard A BrealeyDocumento18 páginasTest Bank For Principles of Corporate Finance 9th Edition Richard A Brealeyhightpiprall3cb2Ainda não há avaliações

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNNo Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNNota: 4.5 de 5 estrelas4.5/5 (3)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisNo EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisNota: 5 de 5 estrelas5/5 (6)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaNo EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaNota: 3.5 de 5 estrelas3.5/5 (8)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaNo EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaNota: 4.5 de 5 estrelas4.5/5 (14)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successNo EverandReady, Set, Growth hack:: A beginners guide to growth hacking successNota: 4.5 de 5 estrelas4.5/5 (93)

- An easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyNo EverandAn easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyNota: 3 de 5 estrelas3/5 (1)