Você também pode gostar

- Declaration FormDocumento1 páginaDeclaration FormLizzette Dela PenaAinda não há avaliações

- HB 02100Documento6 páginasHB 02100Lizzette Dela PenaAinda não há avaliações

- Legislator's Forum On Law and ReligionDocumento1 páginaLegislator's Forum On Law and ReligionLizzette Dela PenaAinda não há avaliações

- SOCIAL WELFARE - Vulnerable SectorsDocumento8 páginasSOCIAL WELFARE - Vulnerable SectorsLizzette Dela PenaAinda não há avaliações

- Pidsdps 2223Documento38 páginasPidsdps 2223Lizzette Dela PenaAinda não há avaliações

- Executive Digest CompilationDocumento22 páginasExecutive Digest CompilationLizzette Dela PenaAinda não há avaliações

- HB 05445Documento5 páginasHB 05445Lizzette Dela PenaAinda não há avaliações

- IndexNCR30km BufferDocumento1 páginaIndexNCR30km BufferLizzette Dela PenaAinda não há avaliações

- Guide To Appellate PleadingsDocumento14 páginasGuide To Appellate PleadingsLizzette Dela PenaAinda não há avaliações

- Judicial Affidavit TemplateDocumento9 páginasJudicial Affidavit TemplateLizzette Dela PenaAinda não há avaliações

- Proposed Rules of Congress For The Canvassing of The Presidential and - Vice-Presidential Candidates in The 2022 Elections - FinalDocumento22 páginasProposed Rules of Congress For The Canvassing of The Presidential and - Vice-Presidential Candidates in The 2022 Elections - FinalLizzette Dela PenaAinda não há avaliações

- I. Executive Summary: Climate Change and The Philippines Executive Brief, 2018 Commission On Climate ChangeDocumento10 páginasI. Executive Summary: Climate Change and The Philippines Executive Brief, 2018 Commission On Climate ChangeLizzette Dela PenaAinda não há avaliações

- Merit and FitnessDocumento2 páginasMerit and FitnessLizzette Dela PenaAinda não há avaliações

- Roster LegislatorsDocumento215 páginasRoster LegislatorsLizzette Dela PenaAinda não há avaliações

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Transaction Date Value Date Cheque Number/ Transaction Number Description Debit Credit Running BalanceDocumento2 páginasTransaction Date Value Date Cheque Number/ Transaction Number Description Debit Credit Running Balancesylvereye07Ainda não há avaliações

- Plane Ticket Template 5Documento2 páginasPlane Ticket Template 503062872819sAinda não há avaliações

- Hetzner 2023-01-04 R0017904414Documento1 páginaHetzner 2023-01-04 R0017904414djsaba2010Ainda não há avaliações

- Derek Ramsay vs. CIR (2015)Documento24 páginasDerek Ramsay vs. CIR (2015)Marie MoralesAinda não há avaliações

- Fee Notification of Under-Graduate BAMS, BHMS, BNYS, BUMS, BHA, BPO & B.SC Allied Health Sciences During September2017Documento4 páginasFee Notification of Under-Graduate BAMS, BHMS, BNYS, BUMS, BHA, BPO & B.SC Allied Health Sciences During September2017passionAinda não há avaliações

- 0304 Crossing of ChequesDocumento8 páginas0304 Crossing of ChequesJitendra VirahyasAinda não há avaliações

- Receipt For Your Payment To American English TreeDocumento7 páginasReceipt For Your Payment To American English TreeLyle KajnerAinda não há avaliações

- GSRTCDocumento1 páginaGSRTCPratik JayswalAinda não há avaliações

- Direct Deposit Enrollment Form: Stride Bank, N.A. 123Documento1 páginaDirect Deposit Enrollment Form: Stride Bank, N.A. 123BotaAinda não há avaliações

- Basic Reconciliation StatementDocumento13 páginasBasic Reconciliation StatementEaster Adina-LumangAinda não há avaliações

- 04 Business Taxation: Clwtaxn de La Salle UniversityDocumento51 páginas04 Business Taxation: Clwtaxn de La Salle UniversityTrisha RuzolAinda não há avaliações

- Gsrtc. 2 - 1 - 24Documento1 páginaGsrtc. 2 - 1 - 24Mitanshu BhavsarAinda não há avaliações

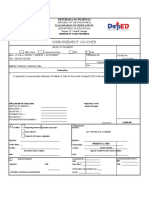

- VoucherDocumento1 páginaVoucherJeanette FerrolinoAinda não há avaliações

- Statement Showing Particulars of Claims by An Employee For Deduction of Tax Under Section 192Documento1 páginaStatement Showing Particulars of Claims by An Employee For Deduction of Tax Under Section 192Guru RajAinda não há avaliações

- Tolentino vs. Secretary of Finance - G.R. No. 115455 - October 30, 1995Documento1 páginaTolentino vs. Secretary of Finance - G.R. No. 115455 - October 30, 1995Andrew Gallardo100% (1)

- Rekening Koran Permata IDRDocumento2 páginasRekening Koran Permata IDRericksanjaya80% (5)

- Night Safari TicketDocumento2 páginasNight Safari TicketYongsem EngAinda não há avaliações

- Vyapti Infrabuild PVT - LTD.: Duvf - U QHN (Documento2 páginasVyapti Infrabuild PVT - LTD.: Duvf - U QHN (M AbhiAinda não há avaliações

- Od 226072731036375000Documento1 páginaOd 226072731036375000Chirag ChauhanAinda não há avaliações

- Apple South Asia Pte LTD: 7 Ang Mo Kio Street 64 SINGAPORE 569086 TEL: 6481 5511Documento1 páginaApple South Asia Pte LTD: 7 Ang Mo Kio Street 64 SINGAPORE 569086 TEL: 6481 5511Jesmine TgAinda não há avaliações

- UnlockedDocumento36 páginasUnlockedMayank ShrivastavaAinda não há avaliações

- ARS Telstra Australia PDFDocumento1 páginaARS Telstra Australia PDFishajain6920Ainda não há avaliações

- Ap TcodeDocumento3 páginasAp Tcodeanuagarwal anuAinda não há avaliações

- Girnar Insurance Brokers Private Limited: Salary Slip For The Month of February - 2023Documento2 páginasGirnar Insurance Brokers Private Limited: Salary Slip For The Month of February - 2023karanmitroo1Ainda não há avaliações

- K & C Band Rental Letter 2021Documento1 páginaK & C Band Rental Letter 2021ChuckAinda não há avaliações

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocumento27 páginasDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDHRUMIL NEGANDHIAinda não há avaliações

- Craig's Design and Landscaping Services: Account ListDocumento3 páginasCraig's Design and Landscaping Services: Account Listudit guptaAinda não há avaliações

- Bazaar Invitation Letter PDFDocumento1 páginaBazaar Invitation Letter PDFLara Zuñiga100% (1)

- UEC Placement Test GuideDocumento2 páginasUEC Placement Test GuideAnindya SUNAinda não há avaliações

- Cfs 9268 MDocumento1 páginaCfs 9268 Mdavidigoro26Ainda não há avaliações