Você também pode gostar

- Audit NotesDocumento1 páginaAudit NotesChauncey Benabaye MalazarteAinda não há avaliações

- Xerox CorporationDocumento9 páginasXerox CorporationAquila Di AngeloAinda não há avaliações

- Audit CapsuleDocumento20 páginasAudit Capsulevishnuverma100% (1)

- Forensic Investigation - ReportDocumento6 páginasForensic Investigation - Reportjhon DavidAinda não há avaliações

- Isa 210 Smart NotesDocumento18 páginasIsa 210 Smart Notesmnouman0309Ainda não há avaliações

- Aud679 Toturial 1Documento2 páginasAud679 Toturial 1liyanahamzahAinda não há avaliações

- Arens AAS17 sm 05筆記版Documento20 páginasArens AAS17 sm 05筆記版林芷瑜Ainda não há avaliações

- Ringkasan AKL1Documento98 páginasRingkasan AKL1BagoesadhiAinda não há avaliações

- Audit Planning - Analytical ProceduresDocumento35 páginasAudit Planning - Analytical ProceduresVenus Lyka LomocsoAinda não há avaliações

- 2018 Quarter 4 Report: Presented by You ExecDocumento20 páginas2018 Quarter 4 Report: Presented by You ExecLohith t rAinda não há avaliações

- Accounts TitleDocumento1 páginaAccounts TitlenovyAinda não há avaliações

- Auditing SP 2008 CH 6 SolutionsDocumento19 páginasAuditing SP 2008 CH 6 SolutionsManal ElkhoshkhanyAinda não há avaliações

- Reading 18 - Evaluating Quality of Financial ReportsDocumento10 páginasReading 18 - Evaluating Quality of Financial ReportsJuan MatiasAinda não há avaliações

- Auditing and Assurance Services 7e - Chapter 5 Flashcards - QuizletDocumento7 páginasAuditing and Assurance Services 7e - Chapter 5 Flashcards - QuizletDieter LudwigAinda não há avaliações

- Noer Rachmadhani H - 1810523011 - Week 10 AssignmentDocumento9 páginasNoer Rachmadhani H - 1810523011 - Week 10 AssignmentSajakul SornAinda não há avaliações

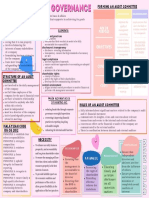

- Corporate Governance MIND MAPDocumento1 páginaCorporate Governance MIND MAPnormalasaliminAinda não há avaliações

- Chapter 9 (3) : Completing The AuditDocumento1 páginaChapter 9 (3) : Completing The AuditARMIZAWANI BINTI MOHAMED BUANG BMAinda não há avaliações

- AUE Answer SheetDocumento14 páginasAUE Answer Sheetcz82h7z84tAinda não há avaliações

- Chapter 15Documento9 páginasChapter 15Dhey LaxamanaAinda não há avaliações

- 6 MA Cheat SheetDocumento1 página6 MA Cheat SheetYASH MAKADIYAAinda não há avaliações

- Accounting InfoDocumento17 páginasAccounting InfoJellivie ManansalaAinda não há avaliações

- Difference Between Accounts & FinanceDocumento4 páginasDifference Between Accounts & Financesameer amjadAinda não há avaliações

- CFAP-6-Summer-2021 AnsDocumento9 páginasCFAP-6-Summer-2021 AnsMuhammad ArslanAinda não há avaliações

- Agency Theory ConflictDocumento5 páginasAgency Theory ConflictDINDAAinda não há avaliações

- Leverage and Excess Risk Acivity Based Costing: BusinessDocumento1 páginaLeverage and Excess Risk Acivity Based Costing: Businessjavier apodacaAinda não há avaliações

- Jun PDFDocumento20 páginasJun PDFCA Guru MadevuAinda não há avaliações

- Audit Responsibilities and Objectives: Review Questions 6-1Documento19 páginasAudit Responsibilities and Objectives: Review Questions 6-1GuinevereAinda não há avaliações

- Case Study Lines Audit Risk Business Risk Auditor's ResponseDocumento8 páginasCase Study Lines Audit Risk Business Risk Auditor's ResponseTushar RegmiAinda não há avaliações

- Basic Elements of ControlDocumento18 páginasBasic Elements of ControlSrijon TalukderAinda não há avaliações

- Chapter 15 AnsDocumento10 páginasChapter 15 AnsDave ManaloAinda não há avaliações

- Analyzing Earnings QualityDocumento6 páginasAnalyzing Earnings QualityLiew Chee KiongAinda não há avaliações

- At.3507 - Considering The Risk of Frauds Errors and NOCLARDocumento5 páginasAt.3507 - Considering The Risk of Frauds Errors and NOCLARJohn MaynardAinda não há avaliações

- Response - Revenue AssuranceDocumento4 páginasResponse - Revenue AssuranceBhagwatiprasad MathurAinda não há avaliações

- Guide Internal Control Over Financial Reporting 2019-05Documento24 páginasGuide Internal Control Over Financial Reporting 2019-05hanafi prasentianto100% (1)

- 3bsa-Tos 1S2223Documento44 páginas3bsa-Tos 1S2223Mary Joy Jessa Santiago BernardinoAinda não há avaliações

- Audit Quick Review PDFDocumento41 páginasAudit Quick Review PDFChunnu ChamkilaAinda não há avaliações

- Auditing ReviewerDocumento2 páginasAuditing ReviewerQueenie de BorjaAinda não há avaliações

- Financial Statement PresentationDocumento9 páginasFinancial Statement PresentationMARIBEL SANTOSAinda não há avaliações

- Chapter 20Documento20 páginasChapter 20Moktasid HossainAinda não há avaliações

- Auditing and The Public Accounting ProfessionDocumento12 páginasAuditing and The Public Accounting ProfessionYebegashet AlemayehuAinda não há avaliações

- Materi Presentasi Audit GabunganDocumento39 páginasMateri Presentasi Audit GabunganRenny NAinda não há avaliações

- TOPICDocumento3 páginasTOPICMariel GarraAinda não há avaliações

- 2Lt Derrick Monriel D Suarez Mac 2Lt Joan C Columbres Mac 2Lt Yvan Rose Villaverde MacDocumento15 páginas2Lt Derrick Monriel D Suarez Mac 2Lt Joan C Columbres Mac 2Lt Yvan Rose Villaverde MacSibin PiptiAinda não há avaliações

- Chapter 14Documento85 páginasChapter 14Crizryshel Loreen P. DeramaAinda não há avaliações

- Annual Report of IOCL 95Documento1 páginaAnnual Report of IOCL 95Nikunj ParmarAinda não há avaliações

- Objective: ISA 570 Going ConcernDocumento10 páginasObjective: ISA 570 Going ConcernHarutraAinda não há avaliações

- Day 33Documento11 páginasDay 33Reem JavedAinda não há avaliações

- Chapter 04Documento39 páginasChapter 04LouiseAinda não há avaliações

- Referencer For Quick Revision: Intermediate Course Paper-6: Auditing and AssuranceDocumento29 páginasReferencer For Quick Revision: Intermediate Course Paper-6: Auditing and AssuranceRamAinda não há avaliações

- Internal Financial Control (Ifc) & Internal Financial Controls Over Financial Reporting (Ifcofr)Documento22 páginasInternal Financial Control (Ifc) & Internal Financial Controls Over Financial Reporting (Ifcofr)Tabassum ButtAinda não há avaliações

- ICFR - NewDocumento31 páginasICFR - NewAnupam BaliAinda não há avaliações

- Regulatory FrameworkDocumento31 páginasRegulatory FrameworkMOHIT BORALKARAinda não há avaliações

- Audit Responsibilities and Objectives: Concept Checks P. 129Documento20 páginasAudit Responsibilities and Objectives: Concept Checks P. 129hsingting yuAinda não há avaliações

- Business Combination and Corporate Restructuring: After Studying This Chapter, You Would Be Able ToDocumento98 páginasBusiness Combination and Corporate Restructuring: After Studying This Chapter, You Would Be Able ToYUUSDHAinda não há avaliações

- IndAS 103 AmalgamationDocumento98 páginasIndAS 103 AmalgamationadityaAinda não há avaliações

- BSBMGT517 Contingency Plan Hima RaiDocumento3 páginasBSBMGT517 Contingency Plan Hima RaiHima RaiAinda não há avaliações

- CH Analisis Aktivitas InvestasiDocumento29 páginasCH Analisis Aktivitas Investasiannis sakinahAinda não há avaliações

- Principles of Auditing and Other Assurance Services 20Th Edition Whittington Solutions Manual Full Chapter PDFDocumento43 páginasPrinciples of Auditing and Other Assurance Services 20Th Edition Whittington Solutions Manual Full Chapter PDFAndrewRobinsonixez100% (10)

- Principles of Auditing and Other Assurance Services 20th Edition Whittington Solutions ManualDocumento22 páginasPrinciples of Auditing and Other Assurance Services 20th Edition Whittington Solutions Manualclarathanhbit05100% (27)

- Vaishnavi FPC - Vegetables NarrationDocumento17 páginasVaishnavi FPC - Vegetables NarrationSamakoi freshAinda não há avaliações

- Chapter 3Documento39 páginasChapter 3bladehero10Ainda não há avaliações

- Randheer Yadav PayslipDocumento1 páginaRandheer Yadav Payslippankaj yadavAinda não há avaliações

- Lease FA1Documento39 páginasLease FA1Chitta LeeAinda não há avaliações

- Thariq QuestionnaireDocumento3 páginasThariq QuestionnaireThariq MohammedAinda não há avaliações

- Materi Bapak Bayu HieDocumento20 páginasMateri Bapak Bayu Hiemutarto haroenAinda não há avaliações

- Rithmic Risk Parameters Guide Digital - EnglishDocumento5 páginasRithmic Risk Parameters Guide Digital - EnglishThe Trading PitAinda não há avaliações

- Detailed Analysis of 920 Short Straddle Strategy. Is It Stopped Working?Documento4 páginasDetailed Analysis of 920 Short Straddle Strategy. Is It Stopped Working?Navin ChandarAinda não há avaliações

- Completed Chapter 6 Problem Working Papers For Artero Corporation Fall 2014Documento5 páginasCompleted Chapter 6 Problem Working Papers For Artero Corporation Fall 2014ZachLoving75% (4)

- Screenshot 2024-01-29 at 19.03.05Documento20 páginasScreenshot 2024-01-29 at 19.03.0547z597rcf6Ainda não há avaliações

- Laporan Keuangan TSPC Q1-23Documento81 páginasLaporan Keuangan TSPC Q1-23Ardina LukitaAinda não há avaliações

- Integration 1. Backward IntegrationDocumento5 páginasIntegration 1. Backward IntegrationMae ann LomugdaAinda não há avaliações

- Course Code: ECO 501 Level: MBA Semester: Semester I Credit Hours: 4 Course ObjectiveDocumento5 páginasCourse Code: ECO 501 Level: MBA Semester: Semester I Credit Hours: 4 Course Objectivesatyendra_upreti2011Ainda não há avaliações

- Tweeter Etc Case StudyDocumento17 páginasTweeter Etc Case StudyArpit CooldudeAinda não há avaliações

- Parag ProjDocumento86 páginasParag ProjParshva VoraAinda não há avaliações

- 1 Business LettersDocumento13 páginas1 Business LettersAnne Dela CruzAinda não há avaliações

- 1458 2735 1 SM PDFDocumento25 páginas1458 2735 1 SM PDFDyenAinda não há avaliações

- APQC - Using APQC Process Classification FrameworkDocumento27 páginasAPQC - Using APQC Process Classification FrameworkAnderson EijiAinda não há avaliações

- SCD Course List in Sem 2.2020 (FTF or Online) (Updated 02 July 2020)Documento2 páginasSCD Course List in Sem 2.2020 (FTF or Online) (Updated 02 July 2020)Nguyễn Hồng AnhAinda não há avaliações

- Verbeke Chapter 1 Conceptual Foundations of International Business StrategyDocumento8 páginasVerbeke Chapter 1 Conceptual Foundations of International Business StrategyCarolina Pérez HuamaníAinda não há avaliações

- ECO101 - Introduction To Microeconomics Lecture Notes: Ahsan Senan (ASE) Last Updated: June 26, 2020Documento64 páginasECO101 - Introduction To Microeconomics Lecture Notes: Ahsan Senan (ASE) Last Updated: June 26, 2020Mahmud Al HasanAinda não há avaliações

- Financial Fragility: Entrepreneurs Can Certainly Provide Many Benefits To Individuals, Society As WellDocumento4 páginasFinancial Fragility: Entrepreneurs Can Certainly Provide Many Benefits To Individuals, Society As WellMohd Azmezanshah Bin SezwanAinda não há avaliações

- Spree Watch Marketing Plan Summary: Situation AnalysisDocumento8 páginasSpree Watch Marketing Plan Summary: Situation AnalysisSreejib DebAinda não há avaliações

- Maxwell CompanyDocumento1 páginaMaxwell CompanyAngeline RamirezAinda não há avaliações

- ISVSej 11.01.X Tanisha RevisedDocumento18 páginasISVSej 11.01.X Tanisha Revisedtanisha rampalAinda não há avaliações

- AF2110 Management Accounting 1 Assignment 05 Suggested Solutions Exercise 6-13 (20 Minutes)Documento12 páginasAF2110 Management Accounting 1 Assignment 05 Suggested Solutions Exercise 6-13 (20 Minutes)Shadow IpAinda não há avaliações

- Resume QuestionsDocumento13 páginasResume Questionsshashank shekharAinda não há avaliações

- Virtual Assistant Agreement: RecitalsDocumento8 páginasVirtual Assistant Agreement: RecitalsmartinaAinda não há avaliações

- Module 4 Macro Perspective of Tourism EditedDocumento13 páginasModule 4 Macro Perspective of Tourism EditedFinn DanganAinda não há avaliações

- V.M.C. Furniture: For Retail / Manufacturing IndustryDocumento2 páginasV.M.C. Furniture: For Retail / Manufacturing Industrycristina constantinoAinda não há avaliações