Você também pode gostar

- R48 Derivative Markets and InstrumentsDocumento179 páginasR48 Derivative Markets and InstrumentsAaliyan Bandealy100% (1)

- 8 CFA Exam Mistakes You Could Be MakingDocumento2 páginas8 CFA Exam Mistakes You Could Be Makingrajah2Ainda não há avaliações

- IBanking Interview Questions CornellDocumento1 páginaIBanking Interview Questions Cornelleberthere163Ainda não há avaliações

- Market Risk Questions PDFDocumento16 páginasMarket Risk Questions PDFbabubhagoud1983Ainda não há avaliações

- CSWP Practice Test Book: Certified Solidworks ProfessionalsDocumento20 páginasCSWP Practice Test Book: Certified Solidworks ProfessionalsmohamedAinda não há avaliações

- Energy Trading And Risk Management A Complete Guide - 2020 EditionNo EverandEnergy Trading And Risk Management A Complete Guide - 2020 EditionAinda não há avaliações

- Simply SaidDocumento1 páginaSimply SaidSamuel G. Korkulo Jr.Ainda não há avaliações

- Brochure AM in Quantitative Finance PDFDocumento6 páginasBrochure AM in Quantitative Finance PDFqueue2010Ainda não há avaliações

- A Z Reading Financial Ratios 1Documento45 páginasA Z Reading Financial Ratios 1HirasTindaon100% (1)

- Wiley CMAexcel Learning System Exam Review 2017: Part 1, Financial Reporting, Planning, Performance, and Control (1-year access)No EverandWiley CMAexcel Learning System Exam Review 2017: Part 1, Financial Reporting, Planning, Performance, and Control (1-year access)Ainda não há avaliações

- CFA - Student PresentationDocumento17 páginasCFA - Student PresentationJasmine Kaur100% (1)

- L1 - Roadmap To Passing The CFA ExamDocumento18 páginasL1 - Roadmap To Passing The CFA ExamSaman BajwaAinda não há avaliações

- Quant Finance RoadMapDocumento8 páginasQuant Finance RoadMapRahul AgarwalAinda não há avaliações

- How To Pass The CFA Level 1 ExamDocumento2 páginasHow To Pass The CFA Level 1 Examtanya1780Ainda não há avaliações

- Financing Agricultural Term InvestmentsDocumento181 páginasFinancing Agricultural Term InvestmentsioanyyAinda não há avaliações

- Weekly Market Commentary 04132015Documento4 páginasWeekly Market Commentary 04132015dpbasicAinda não há avaliações

- 1993-00 A Closed-Form Solution For Options With Stochastic Volatility With Applications To Bond and Currency Options - HestonDocumento17 páginas1993-00 A Closed-Form Solution For Options With Stochastic Volatility With Applications To Bond and Currency Options - Hestonrdouglas2002Ainda não há avaliações

- Safe Handling of Chlorine From Drums and Cylinders (Second Edition)Documento63 páginasSafe Handling of Chlorine From Drums and Cylinders (Second Edition)kapil 11Ainda não há avaliações

- Chapter 7Documento25 páginasChapter 7Cynthia AdiantiAinda não há avaliações

- 2024 L1 CorpIssuersDocumento73 páginas2024 L1 CorpIssuershamna wahabAinda não há avaliações

- Share-Based Compensation: Learning ObjectivesDocumento48 páginasShare-Based Compensation: Learning ObjectivesMark S MadsenAinda não há avaliações

- Investment Performance Measurement: Evaluating and Presenting ResultsNo EverandInvestment Performance Measurement: Evaluating and Presenting ResultsPhilip Lawton, CIPMNota: 1 de 5 estrelas1/5 (1)

- Improving Sector and Thematic ReportingDocumento19 páginasImproving Sector and Thematic ReportingADB Knowledge SolutionsAinda não há avaliações

- Coaching Skills For Optimal PerformanceDocumento58 páginasCoaching Skills For Optimal PerformanceYodhia Antariksa100% (3)

- Lab Report: SimulinkDocumento2 páginasLab Report: SimulinkM Luqman FarooquiAinda não há avaliações

- Risk in Capital Structure Arbitrage 2006Documento46 páginasRisk in Capital Structure Arbitrage 2006jinwei2011Ainda não há avaliações

- FPA Candidate HandbookDocumento32 páginasFPA Candidate HandbookFreddy - Marc NadjéAinda não há avaliações

- Lesson Plan1 Business EthicsDocumento4 páginasLesson Plan1 Business EthicsMonina Villa100% (1)

- The Main Ideas in An Apology For PoetryDocumento6 páginasThe Main Ideas in An Apology For PoetryShweta kashyap100% (3)

- Neuralink DocumentationDocumento25 páginasNeuralink DocumentationVAIDIK Kasoju100% (6)

- Conspicuous Consumption-A Literature ReviewDocumento15 páginasConspicuous Consumption-A Literature Reviewlieu_hyacinthAinda não há avaliações

- PJM ARR and FTR MarketDocumento159 páginasPJM ARR and FTR MarketfwlwllwAinda não há avaliações

- Quant Book ListDocumento8 páginasQuant Book ListdavyarperAinda não há avaliações

- ADDICTED (The Novel) Book 1 - The Original English TranslationDocumento1.788 páginasADDICTED (The Novel) Book 1 - The Original English TranslationMónica M. Giraldo100% (7)

- Ethics and Professional Standards: © Edupristine Cfa Level - IiDocumento128 páginasEthics and Professional Standards: © Edupristine Cfa Level - IiRahul Mehta100% (1)

- M&A TrendingsDocumento52 páginasM&A TrendingsMarcelo Bego LavanhiniAinda não há avaliações

- Accounting Dissertations - IfRSDocumento30 páginasAccounting Dissertations - IfRSgappu002Ainda não há avaliações

- CFITS BrochureDocumento6 páginasCFITS BrochureSiddhartha GaikwadAinda não há avaliações

- R27 CFA Level 3Documento10 páginasR27 CFA Level 3Ashna0188Ainda não há avaliações

- Mock 1 - Afternoon - AnswersDocumento27 páginasMock 1 - Afternoon - Answerspagis31861Ainda não há avaliações

- Ta CN TCNH - Unit 2 - Time Value of MoneyDocumento19 páginasTa CN TCNH - Unit 2 - Time Value of MoneyPhương NhiAinda não há avaliações

- Kroenke Ch01 IMDocumento6 páginasKroenke Ch01 IMArathiAinda não há avaliações

- CFA Vs FRM - Which Is BetterDocumento17 páginasCFA Vs FRM - Which Is BetterIsmael Torres-PizarroAinda não há avaliações

- Morning Session Q&ADocumento50 páginasMorning Session Q&AGANESH MENONAinda não há avaliações

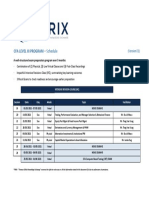

- FIRIX - CFA Level III - IRC (May 2021 Exam)Documento1 páginaFIRIX - CFA Level III - IRC (May 2021 Exam)Via Commerce Sdn BhdAinda não há avaliações

- Leland 1994Documento36 páginasLeland 1994pedda60100% (1)

- Homework Problem Set #4: 1. Trusty Bankco'S Lookback OptionDocumento4 páginasHomework Problem Set #4: 1. Trusty Bankco'S Lookback OptionVivek JaniAinda não há avaliações

- Presented By: Kaushambi Ghosh Manish Madhukar Mohit Almal Pankaj AgarwalDocumento68 páginasPresented By: Kaushambi Ghosh Manish Madhukar Mohit Almal Pankaj Agarwalmohit.almal100% (1)

- (UVTN 2022) Mock Aptitude Test GuidelineDocumento4 páginas(UVTN 2022) Mock Aptitude Test GuidelineTuyết Ngân LêAinda não há avaliações

- Graduate Numerical Tests - Major Providers and UsersDocumento7 páginasGraduate Numerical Tests - Major Providers and UsersAndreiBorseteAinda não há avaliações

- Adms 4551 PDFDocumento50 páginasAdms 4551 PDFjorAinda não há avaliações

- FRM Job Task Analysis:: Executive SummaryDocumento8 páginasFRM Job Task Analysis:: Executive SummaryMayuAinda não há avaliações

- Smart Summary Income Taxes CFADocumento3 páginasSmart Summary Income Taxes CFAKazi HasanAinda não há avaliações

- CFA Level 1 - Section 3 MicroEconomicsDocumento34 páginasCFA Level 1 - Section 3 MicroEconomicsapi-3763138Ainda não há avaliações

- Econ Final SolutionDocumento4 páginasEcon Final SolutionKebonaAinda não há avaliações

- SOA Exam P SyllabusDocumento3 páginasSOA Exam P SyllabusMuneer DhamaniAinda não há avaliações

- Cfa 2009 Level 3 - Exam Mock PM ErrataDocumento2 páginasCfa 2009 Level 3 - Exam Mock PM ErratabunnyblasterAinda não há avaliações

- T1-FRM-1-Ch1-501-502-20.1-20.3-v1 - Practice QuestionsDocumento19 páginasT1-FRM-1-Ch1-501-502-20.1-20.3-v1 - Practice QuestionscristianoAinda não há avaliações

- Rhonda Hamilton Case Scenario: Exhibit 1 Hamilton'S Regression Model For Electric Utility IndustryDocumento34 páginasRhonda Hamilton Case Scenario: Exhibit 1 Hamilton'S Regression Model For Electric Utility IndustryĐặng Xuân ĐỉnhAinda não há avaliações

- 2014 Mock Exam - AM - QuestionDocumento30 páginas2014 Mock Exam - AM - Question12jdAinda não há avaliações

- Vault Guide To Actuarial Careers (2007)Documento232 páginasVault Guide To Actuarial Careers (2007)Christopher KingAinda não há avaliações

- JP Morgan Guide - To - Mutual - Fund - InvestingDocumento12 páginasJP Morgan Guide - To - Mutual - Fund - InvestingAnkit KanojiaAinda não há avaliações

- Cunningham MixtapeDocumento328 páginasCunningham MixtapeBen HarveyAinda não há avaliações

- 10 Must-Know Topics To Prepare For A Financial Analyst InterviewDocumento3 páginas10 Must-Know Topics To Prepare For A Financial Analyst InterviewAdilAinda não há avaliações

- CFA Level 1Documento2 páginasCFA Level 1dnavaneethapriyaAinda não há avaliações

- HW 2Documento11 páginasHW 2Sander WongAinda não há avaliações

- Yield Curves and Term Structure TheoryDocumento25 páginasYield Curves and Term Structure TheorychanstriAinda não há avaliações

- SOA Exam CDocumento6 páginasSOA Exam CNoDriverAinda não há avaliações

- Recent Trends in Industrial Growth in IndiaDocumento8 páginasRecent Trends in Industrial Growth in Indiaanubhav mishraAinda não há avaliações

- 1 2+Book+FormatDocumento44 páginas1 2+Book+Formataloo+gubhiAinda não há avaliações

- India's Trade Reform: Arvind PanagariyaDocumento68 páginasIndia's Trade Reform: Arvind Panagariyaaloo+gubhiAinda não há avaliações

- Guide To BibliographyDocumento46 páginasGuide To Bibliographyaloo+gubhiAinda não há avaliações

- Recent Trends in Industrial Growth in IndiaDocumento8 páginasRecent Trends in Industrial Growth in Indiaanubhav mishraAinda não há avaliações

- Recent Trends in Industrial Growth in IndiaDocumento8 páginasRecent Trends in Industrial Growth in Indiaanubhav mishraAinda não há avaliações

- Install Guide For Sandisk® Memory Zone App To Use Along With Your Sandisk Ultra® Dual DrivesDocumento7 páginasInstall Guide For Sandisk® Memory Zone App To Use Along With Your Sandisk Ultra® Dual DrivesGalih PranayudhaAinda não há avaliações

- OECD Composite Leading Indicators:: February 2017Documento48 páginasOECD Composite Leading Indicators:: February 2017aloo+gubhiAinda não há avaliações

- 180 Sample-Chapter PDFDocumento15 páginas180 Sample-Chapter PDFhanumanthaiahgowdaAinda não há avaliações

- Annexure I: Departmental Assistance at Rs. 3000/-P.a. Per Student To The Host Institution For Pursuing InfrastructureDocumento1 páginaAnnexure I: Departmental Assistance at Rs. 3000/-P.a. Per Student To The Host Institution For Pursuing InfrastructureSonam TobgyalAinda não há avaliações

- This Is To Certify ThatDocumento1 páginaThis Is To Certify ThatSonam TobgyalAinda não há avaliações

- This Is To Certify ThatDocumento1 páginaThis Is To Certify ThatSonam TobgyalAinda não há avaliações

- This Is To Certify ThatDocumento1 páginaThis Is To Certify ThatSonam TobgyalAinda não há avaliações

- Growth Rate at Factor Cost at Constant PricesDocumento2 páginasGrowth Rate at Factor Cost at Constant Pricesaloo+gubhiAinda não há avaliações

- Journal ListDocumento2 páginasJournal Listaloo+gubhiAinda não há avaliações

- Application For Birth Certificate PDFDocumento1 páginaApplication For Birth Certificate PDFAjayAsthanaAinda não há avaliações

- Workshop Brochure - Fin EconometricsDocumento3 páginasWorkshop Brochure - Fin EconometricsjamesAinda não há avaliações

- (A) Bimetallism:: Monetary Standards: Bimetallism, Monometallism and Paper StandardDocumento8 páginas(A) Bimetallism:: Monetary Standards: Bimetallism, Monometallism and Paper Standardaloo+gubhiAinda não há avaliações

- Abhi J It SenguptaDocumento33 páginasAbhi J It Senguptaaloo+gubhiAinda não há avaliações

- DatabookDec2014 10Documento2 páginasDatabookDec2014 10anirbanccim8493Ainda não há avaliações

- Chapter BibDocumento5 páginasChapter Bibaloo+gubhiAinda não há avaliações

- Ts DynDocumento86 páginasTs Dynaloo+gubhiAinda não há avaliações

- Suspension of Classess - 6nov2017Documento1 páginaSuspension of Classess - 6nov2017aloo+gubhiAinda não há avaliações

- Mohanty2005 PDFDocumento41 páginasMohanty2005 PDFaloo+gubhiAinda não há avaliações

- IfyDocumento6 páginasIfyVibhor MittalAinda não há avaliações

- How Well Have You Learnt About Fractions?Documento28 páginasHow Well Have You Learnt About Fractions?aloo+gubhiAinda não há avaliações

- Journals at IDEASDocumento158 páginasJournals at IDEASaloo+gubhiAinda não há avaliações

- Journal Quality List: Fifty-Seventh Edition, 18 April 2016Documento25 páginasJournal Quality List: Fifty-Seventh Edition, 18 April 2016aloo+gubhiAinda não há avaliações

- 1 PDFDocumento30 páginas1 PDFaloo+gubhiAinda não há avaliações

- Birth Control Comparison Chart 2018Documento1 páginaBirth Control Comparison Chart 2018Eric SandesAinda não há avaliações

- Learn JQuery - Learn JQuery - Event Handlers Cheatsheet - CodecademyDocumento2 páginasLearn JQuery - Learn JQuery - Event Handlers Cheatsheet - Codecademyilias ahmedAinda não há avaliações

- 145class 7 Integers CH 1Documento2 páginas145class 7 Integers CH 17A04Aditya MayankAinda não há avaliações

- Research in NursingDocumento54 páginasResearch in Nursingrockycamaligan2356Ainda não há avaliações

- ENVSOCTY 1HA3 - Lecture 01 - Introduction & Course Overview - Skeletal NotesDocumento28 páginasENVSOCTY 1HA3 - Lecture 01 - Introduction & Course Overview - Skeletal NotesluxsunAinda não há avaliações

- Part 4 Basic ConsolidationDocumento3 páginasPart 4 Basic Consolidationtαtmαn dє grєαtAinda não há avaliações

- Ethics - FinalsDocumento18 páginasEthics - Finalsannie lalangAinda não há avaliações

- Assignment in Legal CounselingDocumento4 páginasAssignment in Legal CounselingEmmagine E EyanaAinda não há avaliações

- Amy Kelaidis Resume Indigeous Education 2015 FinalDocumento3 páginasAmy Kelaidis Resume Indigeous Education 2015 Finalapi-292414807Ainda não há avaliações

- Building Social CapitalDocumento17 páginasBuilding Social CapitalMuhammad RonyAinda não há avaliações

- Investigative Project Group 8Documento7 páginasInvestigative Project Group 8Riordan MoraldeAinda não há avaliações

- 3a Ela Day 3Documento5 páginas3a Ela Day 3api-373496210Ainda não há avaliações

- Integrating Intuition and Analysis Edward Deming Once SaidDocumento2 páginasIntegrating Intuition and Analysis Edward Deming Once SaidRimsha Noor ChaudaryAinda não há avaliações

- HeavyReding ReportDocumento96 páginasHeavyReding ReportshethAinda não há avaliações

- Privileged Communications Between Husband and Wife - Extension of PDFDocumento7 páginasPrivileged Communications Between Husband and Wife - Extension of PDFKitingPadayhagAinda não há avaliações

- Upanikhat-I Garbha A Mughal Translation PDFDocumento18 páginasUpanikhat-I Garbha A Mughal Translation PDFReginaldoJurandyrdeMatosAinda não há avaliações

- QUARTER 3, WEEK 9 ENGLISH Inkay - PeraltaDocumento43 páginasQUARTER 3, WEEK 9 ENGLISH Inkay - PeraltaPatrick EdrosoloAinda não há avaliações

- Guoyin Shen, Ho-Kwang Mao and Russell J. Hemley - Laser-Heated Diamond Anvil Cell Technique: Double-Sided Heating With Multimode Nd:YAG LaserDocumento5 páginasGuoyin Shen, Ho-Kwang Mao and Russell J. Hemley - Laser-Heated Diamond Anvil Cell Technique: Double-Sided Heating With Multimode Nd:YAG LaserDeez34PAinda não há avaliações

- Physiotherapy For ChildrenDocumento2 páginasPhysiotherapy For ChildrenCatalina LucaAinda não há avaliações

- Audi A4 Quattro 3.0 Liter 6-Cyl. 5V Fuel Injection & IgnitionDocumento259 páginasAudi A4 Quattro 3.0 Liter 6-Cyl. 5V Fuel Injection & IgnitionNPAinda não há avaliações

- Recurrent: or Reinfection Susceptible People: Adult With Low Im Munity (Especially HIV Patient) Pathologic ChangesDocumento36 páginasRecurrent: or Reinfection Susceptible People: Adult With Low Im Munity (Especially HIV Patient) Pathologic ChangesOsama SaidatAinda não há avaliações