Você também pode gostar

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Music in The Air - Stairway To HeavenDocumento3 páginasMusic in The Air - Stairway To Heavenkunalwarwick0% (1)

- X 70 15 PDFDocumento32 páginasX 70 15 PDFkunalwarwickAinda não há avaliações

- Yale Som View BookDocumento36 páginasYale Som View BookkunalwarwickAinda não há avaliações

- TAP Press Release 01-30-2017Documento2 páginasTAP Press Release 01-30-2017kunalwarwickAinda não há avaliações

- WatsonPaths - Scenario-basedQuestionAnsweringand Inference Over Unstructured InformationDocumento20 páginasWatsonPaths - Scenario-basedQuestionAnsweringand Inference Over Unstructured InformationkunalwarwickAinda não há avaliações

- The Next 200 Years PDFDocumento258 páginasThe Next 200 Years PDFkunalwarwickAinda não há avaliações

- Clausing Profit ShiftingDocumento32 páginasClausing Profit ShiftingkunalwarwickAinda não há avaliações

- Baker Vertical MergersDocumento7 páginasBaker Vertical MergerskunalwarwickAinda não há avaliações

- The Next 200 YearsDocumento258 páginasThe Next 200 Yearskunalwarwick100% (1)

- UBS 2015 Final Final WithNotesDocumento148 páginasUBS 2015 Final Final WithNoteskunalwarwickAinda não há avaliações

- Safaricom Feasibility StudyDocumento11 páginasSafaricom Feasibility StudykunalwarwickAinda não há avaliações

- NFLX EarningsMiss NoSurpise2015!10!20Documento5 páginasNFLX EarningsMiss NoSurpise2015!10!20kunalwarwickAinda não há avaliações

- Q1 2015 AOL Trending SchedulesDocumento4 páginasQ1 2015 AOL Trending ScheduleskunalwarwickAinda não há avaliações

- AOL Transcript 2015 05 08T12 00Documento19 páginasAOL Transcript 2015 05 08T12 00kunalwarwickAinda não há avaliações

- Fiscal Policy Nov 2013 FINALDocumento7 páginasFiscal Policy Nov 2013 FINALkunalwarwickAinda não há avaliações

- Slides Machine Learning and EconometricsDocumento44 páginasSlides Machine Learning and EconometricsdiocerAinda não há avaliações

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- InvoiceDocumento21 páginasInvoiceDon SniperAinda não há avaliações

- DT 0103 Personal Income Tax Return Form V103-Ver-1.1..-1Documento4 páginasDT 0103 Personal Income Tax Return Form V103-Ver-1.1..-1AgyeiAinda não há avaliações

- Account StatementDocumento3 páginasAccount Statementug1837712Ainda não há avaliações

- Iblr220800068978 PDFDocumento1 páginaIblr220800068978 PDFMURALI HNAinda não há avaliações

- Statement 2023 01 06 2023 04 20Documento2 páginasStatement 2023 01 06 2023 04 20Avtar SAinda não há avaliações

- 596 Idbi StatementDocumento11 páginas596 Idbi Statementsri harshaAinda não há avaliações

- Bill Statement: Previous Charges Amount (RM) Current Charges Amount (RM)Documento6 páginasBill Statement: Previous Charges Amount (RM) Current Charges Amount (RM)شمس الدين إسماعيلAinda não há avaliações

- Ce Block NCF RC - 815 and RC-642 Haider Saleh Al-HaiderDocumento3 páginasCe Block NCF RC - 815 and RC-642 Haider Saleh Al-Haidersudeep karunAinda não há avaliações

- Bank Statement Sept 2017Documento2 páginasBank Statement Sept 2017Yogesh PangareAinda não há avaliações

- Muhammad Yousuf: Account StatementDocumento5 páginasMuhammad Yousuf: Account StatementYOUSUFAinda não há avaliações

- Phil Geothermal V CIR GR 154028 July 29, 2005Documento1 páginaPhil Geothermal V CIR GR 154028 July 29, 2005katentom-1Ainda não há avaliações

- Investment Income and Expenses: (Including Capital Gains and Losses)Documento76 páginasInvestment Income and Expenses: (Including Capital Gains and Losses)Kenny Svatek100% (1)

- FESCO N Type Nov 2023Documento1 páginaFESCO N Type Nov 2023tanveerAinda não há avaliações

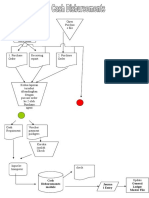

- Flowchart Account Payable & Cash DisbursementsDocumento4 páginasFlowchart Account Payable & Cash DisbursementsAlif Nur IrvanAinda não há avaliações

- AADocumento11 páginasAAJames wiliamAinda não há avaliações

- Taxation of Employment IncomeDocumento7 páginasTaxation of Employment IncomeJamvy Jose FernandezAinda não há avaliações

- TD Beyond Checking: Account SummaryDocumento4 páginasTD Beyond Checking: Account SummaryJohn BeanAinda não há avaliações

- PDFDocumento2 páginasPDFvvv sn raoAinda não há avaliações

- Fiscal Policy: Expansionary Fiscal Policy When The Government Spend More Then It Receives in Order ToDocumento2 páginasFiscal Policy: Expansionary Fiscal Policy When The Government Spend More Then It Receives in Order TominhaxxAinda não há avaliações

- May 30 Provider Relief Fund FAQ RedlineDocumento23 páginasMay 30 Provider Relief Fund FAQ RedlineRachel Cohrs100% (1)

- N3552005822 SKU71 - 2 - 3552005822: Service Number IvrsDocumento1 páginaN3552005822 SKU71 - 2 - 3552005822: Service Number IvrsShubham NamdevAinda não há avaliações

- Take Home Quiz On Taxation Law Prepared By: Prof. AGN Concepts To StudyDocumento3 páginasTake Home Quiz On Taxation Law Prepared By: Prof. AGN Concepts To StudyJImlan Sahipa IsmaelAinda não há avaliações

- 1701 Jan 2018 Final With RatesDocumento4 páginas1701 Jan 2018 Final With RatesexquisiteAinda não há avaliações

- Aston Corporation Performs Year End Planning in November of Each YearDocumento2 páginasAston Corporation Performs Year End Planning in November of Each YearAmit PandeyAinda não há avaliações

- TATA DOCOMO E-Bill Statement For MAR 15 PDFDocumento2 páginasTATA DOCOMO E-Bill Statement For MAR 15 PDFHafeezulla KhanAinda não há avaliações

- Taxation Law-IDocumento18 páginasTaxation Law-IMahamaya GautamiAinda não há avaliações

- PDF - ChallanList - 10 - 7 - 2021 12 - 00 - 00 AMDocumento1 páginaPDF - ChallanList - 10 - 7 - 2021 12 - 00 - 00 AM11 R N Roshikha 9 CAinda não há avaliações

- Agriculture IncomeDocumento6 páginasAgriculture IncomeKartikAinda não há avaliações

- Tax Income, Sunk Cost and Opportunity Cost: Week 13Documento46 páginasTax Income, Sunk Cost and Opportunity Cost: Week 13satryoyu811Ainda não há avaliações

- Ticket 2021 Mathematics Challenge For Young Australians (MCYA)Documento3 páginasTicket 2021 Mathematics Challenge For Young Australians (MCYA)Michael ChenAinda não há avaliações