Você também pode gostar

- Cash Flow Statement AnalysisDocumento11 páginasCash Flow Statement Analysisrscjat100% (1)

- Balance Sheet AccountsDocumento7 páginasBalance Sheet AccountsroldanAinda não há avaliações

- Term-Paper - Personal Finance and New TechnologiesDocumento11 páginasTerm-Paper - Personal Finance and New TechnologiesMae Ann BongcoAinda não há avaliações

- Cash Flow StatementDocumento19 páginasCash Flow Statementasherjoe67% (3)

- Share CapitalDocumento21 páginasShare CapitalMehal Ur RahmanAinda não há avaliações

- Foreign Exchange Risk ManagementDocumento12 páginasForeign Exchange Risk ManagementDinesh KumarAinda não há avaliações

- Financial ManagementDocumento51 páginasFinancial Managementarjunmba119624Ainda não há avaliações

- Evolution of International MonetaryDocumento7 páginasEvolution of International MonetaryManish KumarAinda não há avaliações

- Chap 001Documento14 páginasChap 001Adi Susilo100% (1)

- Investments and Portfolio ManagementDocumento5 páginasInvestments and Portfolio ManagementFedrick BuenaventuraAinda não há avaliações

- Financial Market in Pakistan: Financial Markets and Their Roles: Commercial BanksDocumento5 páginasFinancial Market in Pakistan: Financial Markets and Their Roles: Commercial BanksAnamMalikAinda não há avaliações

- Accounting Is An Information System That IdentifiesDocumento5 páginasAccounting Is An Information System That Identifiesniser88Ainda não há avaliações

- Capital and Money MarketDocumento17 páginasCapital and Money MarketBalamanichalaBmcAinda não há avaliações

- Balance of Payment: According To International Monetary Fund (IMF)Documento6 páginasBalance of Payment: According To International Monetary Fund (IMF)Asim RazaAinda não há avaliações

- EC10120-Economic Principles and Skills I - Why Do Countries Trade With Each OtherDocumento3 páginasEC10120-Economic Principles and Skills I - Why Do Countries Trade With Each OtherdpsmafiaAinda não há avaliações

- Fima30063-Lect1-Overview of CreditDocumento24 páginasFima30063-Lect1-Overview of CreditNicole Lanorio100% (1)

- Money MarketDocumento20 páginasMoney Marketmanisha guptaAinda não há avaliações

- Franco UNIT 6 - AssignmentDocumento2 páginasFranco UNIT 6 - AssignmentBREVISH DAME FRANCOAinda não há avaliações

- Introduction To Financial TechnologyDocumento6 páginasIntroduction To Financial TechnologyKelvin Lim Wei QuanAinda não há avaliações

- Revenue Recognition: Sale of Goods and Services (AS-9) and Construction Contracts (AS-7)Documento31 páginasRevenue Recognition: Sale of Goods and Services (AS-9) and Construction Contracts (AS-7)Aayushi AroraAinda não há avaliações

- List of Indian Accounting Standards Along With Comparative Accounting Standard (AS)Documento6 páginasList of Indian Accounting Standards Along With Comparative Accounting Standard (AS)Krishna PrasadAinda não há avaliações

- Foreign Exchange MarketDocumento8 páginasForeign Exchange MarketYadhu ManuAinda não há avaliações

- Financial ManagementDocumento23 páginasFinancial ManagementArayKumisbayAinda não há avaliações

- Tandon Committee Report On Working CapitalDocumento4 páginasTandon Committee Report On Working CapitalMohitAhujaAinda não há avaliações

- 6.sources of FundsDocumento10 páginas6.sources of FundsHafizullah AnsariAinda não há avaliações

- An Introduction To Mutual Funds: Umair Javed ImamDocumento57 páginasAn Introduction To Mutual Funds: Umair Javed Imamapi-2719799150% (2)

- Exchange Rate Management SystemsDocumento3 páginasExchange Rate Management SystemsMonalisa PadhyAinda não há avaliações

- Working Capital Management of SectrixDocumento50 páginasWorking Capital Management of SectrixsectrixAinda não há avaliações

- Making An Investment PlanDocumento10 páginasMaking An Investment Plananon_118801Ainda não há avaliações

- International Liquidity & International ReservesDocumento17 páginasInternational Liquidity & International ReservesPrabu ManoharanAinda não há avaliações

- Attributes and Features of InvestmentDocumento5 páginasAttributes and Features of InvestmentAashutosh ChandraAinda não há avaliações

- Forex Reserves IndiaDocumento27 páginasForex Reserves IndiaDhaval Lagwankar100% (2)

- Balance Sheet Income StatementDocumento50 páginasBalance Sheet Income Statementgurbaxeesh0% (1)

- Capital MarketDocumento8 páginasCapital Marketshounak3Ainda não há avaliações

- Financial ManagementDocumento43 páginasFinancial Managementonly_vimaljoshi100% (3)

- Operation Management NotesDocumento30 páginasOperation Management NotesRenato WilsonAinda não há avaliações

- Time Value of MoneyDocumento10 páginasTime Value of Moneyanupamamathur09100% (1)

- Bond Valuation NotesDocumento3 páginasBond Valuation NotesChristine LealAinda não há avaliações

- Corporate Governance and Other StakeholdersDocumento44 páginasCorporate Governance and Other Stakeholdersswatantra.s8872450% (1)

- Analysis of Financial Statements Of: Presented by AyeshaDocumento30 páginasAnalysis of Financial Statements Of: Presented by AyeshaaaaaAinda não há avaliações

- Unit I Introduction To Marketing FinanceDocumento3 páginasUnit I Introduction To Marketing Financerajesh laddhaAinda não há avaliações

- Unit 10 Financial MarketsDocumento9 páginasUnit 10 Financial MarketsDURGESH MANI MISHRA PAinda não há avaliações

- Working Capital AnalysisDocumento20 páginasWorking Capital Analysisaneek100% (1)

- Sources of Funds: Presented by Yogeesh L N Lecturer in Commerce and Management BangaloreDocumento14 páginasSources of Funds: Presented by Yogeesh L N Lecturer in Commerce and Management BangaloreYogeesh LNAinda não há avaliações

- Financial ManagementDocumento103 páginasFinancial ManagementMehwishAinda não há avaliações

- Banking Diploma Bangladesh Law Short NotesDocumento19 páginasBanking Diploma Bangladesh Law Short NotesNiladri HasanAinda não há avaliações

- Analyzing Balance SheetDocumento29 páginasAnalyzing Balance Sheetpark_site_atAinda não há avaliações

- C.A IPCC Ratio AnalysisDocumento6 páginasC.A IPCC Ratio AnalysisAkash Gupta100% (2)

- Savings andDocumento9 páginasSavings andRamiz JavedAinda não há avaliações

- 4.1-Hortizontal/Trends Analysis: Chapter No # 4Documento32 páginas4.1-Hortizontal/Trends Analysis: Chapter No # 4Sadi ShahzadiAinda não há avaliações

- Determinants of Exchange RateDocumento2 páginasDeterminants of Exchange RateSajid Ali BhuttaAinda não há avaliações

- Debt Vs Equity FinancingDocumento6 páginasDebt Vs Equity FinancingJo Angeli100% (2)

- Sources of International FinancingDocumento6 páginasSources of International FinancingSabha Pathy100% (2)

- Evolution of Financial SystemDocumento12 páginasEvolution of Financial SystemGautam JayasuryaAinda não há avaliações

- Sections of A Business PlanDocumento7 páginasSections of A Business PlanajmeredithAinda não há avaliações

- Profit Maximization and Wealth MaximixationDocumento1 páginaProfit Maximization and Wealth MaximixationG_BaseAinda não há avaliações

- Meaning of CapitalizationDocumento16 páginasMeaning of CapitalizationSaumya GaurAinda não há avaliações

- Presentation On Stock BrokingDocumento21 páginasPresentation On Stock Brokingocy120% (1)

- FM Reliance IndustriesDocumento30 páginasFM Reliance IndustriesAkshata Masurkar100% (2)

- Analyzing Financial Statements: Before You Go On Questions and AnswersDocumento52 páginasAnalyzing Financial Statements: Before You Go On Questions and AnswersNguyen Ngoc Minh Chau (K15 HL)Ainda não há avaliações

- MSME Certificate With AnnexureDocumento2 páginasMSME Certificate With AnnexureRanjeet MauryaAinda não há avaliações

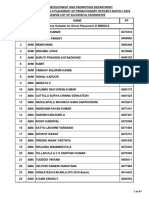

- PO 2019 Final+Select+List-SBITIMESDocumento67 páginasPO 2019 Final+Select+List-SBITIMESRanjeet MauryaAinda não há avaliações

- Evolution of Panchayati Raj System in India - General Knowledge TodayDocumento5 páginasEvolution of Panchayati Raj System in India - General Knowledge TodayRanjeet MauryaAinda não há avaliações

- List of Names of Various Tribal Groups and EconomyDocumento50 páginasList of Names of Various Tribal Groups and EconomyRanjeet MauryaAinda não há avaliações

- Concepts of Political ScienceDocumento57 páginasConcepts of Political ScienceRanjeet Maurya100% (2)

- Sessions of ParliamentDocumento16 páginasSessions of ParliamentRanjeet MauryaAinda não há avaliações

- Syllabus of APFC EPFODocumento1 páginaSyllabus of APFC EPFORanjeet MauryaAinda não há avaliações

- World BankDocumento3 páginasWorld BankRanjeet MauryaAinda não há avaliações

- DerivativesDocumento2 páginasDerivativesRanjeet MauryaAinda não há avaliações

- Infrastructure FinancingDocumento6 páginasInfrastructure FinancingapmeaAinda não há avaliações

- Brexit and Its Impact On Sri LankaDocumento15 páginasBrexit and Its Impact On Sri LankaChathurika Wijayawardana50% (2)

- All Linear Equation Questions From CAT Previous PapersDocumento26 páginasAll Linear Equation Questions From CAT Previous PapersSima DuttaAinda não há avaliações

- Barclays Headquarters II Withdraw Protocol: Bank Use OnlyDocumento1 páginaBarclays Headquarters II Withdraw Protocol: Bank Use OnlyАртём Надемский50% (2)

- Fims Unit - 1Documento17 páginasFims Unit - 1arjunmba119624Ainda não há avaliações

- Haitoglou BrosDocumento25 páginasHaitoglou BrosEva MercedesAinda não há avaliações

- Advantages and Disadvantages of Free Public Transport ServicesDocumento14 páginasAdvantages and Disadvantages of Free Public Transport ServicessamuelioAinda não há avaliações

- 2 ND Bit Coin White PaperDocumento17 páginas2 ND Bit Coin White PaperReid DouthatAinda não há avaliações

- Excel 19Documento6 páginasExcel 19debojyotiAinda não há avaliações

- New Ebook .How To Invest in Private Placement ProgramsDocumento30 páginasNew Ebook .How To Invest in Private Placement ProgramsVicente Piqueras100% (2)

- Zimbabwe Booklet May 2012Documento73 páginasZimbabwe Booklet May 2012Willem Dirk KadijkAinda não há avaliações

- Annex II E3h2 Gencond enDocumento19 páginasAnnex II E3h2 Gencond ensdiamanAinda não há avaliações

- Ecb-Public: Christine LAGARDEDocumento3 páginasEcb-Public: Christine LAGARDEaldhibahAinda não há avaliações

- Top 100 Aerospace & Defence CompaniesDocumento14 páginasTop 100 Aerospace & Defence Companieschintanvisharia40% (5)

- Comcast and NBC Merger/acquisitionDocumento15 páginasComcast and NBC Merger/acquisitionManoj KapoorAinda não há avaliações

- CFA1 2019 Mock3 QuestionsDocumento44 páginasCFA1 2019 Mock3 QuestionsmajedmoghadamiAinda não há avaliações

- Carinska Pravila - Po Zemljama - Import Regulation - by CountriesDocumento90 páginasCarinska Pravila - Po Zemljama - Import Regulation - by CountriesvoodoonsAinda não há avaliações

- FinACt 5 Foreign Currency TransactionsDocumento2 páginasFinACt 5 Foreign Currency TransactionsBedynz Mark Pimentel100% (2)

- Solution To MBA Question 25Documento7 páginasSolution To MBA Question 25tallyho2906Ainda não há avaliações

- 16-F-324-Eurocurrency Markets & Syndicated Credits PDFDocumento22 páginas16-F-324-Eurocurrency Markets & Syndicated Credits PDFDhaval ShahAinda não há avaliações

- LTD Offer 2019 EurDocumento2 páginasLTD Offer 2019 EurkatariamanojAinda não há avaliações

- 1 Euro To Usd Chart - Google SearchDocumento1 página1 Euro To Usd Chart - Google Searchkojlr2020Ainda não há avaliações

- Transition To 21st Century Socialism in The European Union: Paul Cockshott, Allin Cottrell, Heinz DieterichDocumento20 páginasTransition To 21st Century Socialism in The European Union: Paul Cockshott, Allin Cottrell, Heinz DieterichSpeckled JimAinda não há avaliações

- The Rising Euro Hammers Auto Parts ManufacturersDocumento7 páginasThe Rising Euro Hammers Auto Parts ManufacturersDavis Nadakkavukaran Santhosh100% (1)

- Euro DisneylandDocumento13 páginasEuro DisneylandSoumabrata GangulyAinda não há avaliações

- Automotive Industry in GermanyDocumento20 páginasAutomotive Industry in GermanyJon LeonAinda não há avaliações

- EY Oil and Gas Eye Q4 2011Documento12 páginasEY Oil and Gas Eye Q4 2011EY VenezuelaAinda não há avaliações

- BloombergDocumento100 páginasBloombergMentor RexhepiAinda não há avaliações

- Exam Questions Fina4810Documento9 páginasExam Questions Fina4810Bartholomew Szold75% (4)