Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Guide To Case AnalysisDocumento14 páginasGuide To Case Analysisheyalipona100% (1)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- Contract Law of BangladeshDocumento35 páginasContract Law of Bangladeshruhi100% (5)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Fareast Islami Life Insurance Internship ReportDocumento61 páginasFareast Islami Life Insurance Internship ReportConnorLokman100% (2)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (894)

- 1 Harvard Sample Cover PageDocumento3 páginas1 Harvard Sample Cover PageRosaerioAinda não há avaliações

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Finance Terminologies: 1. Abnormal ReturnDocumento29 páginasFinance Terminologies: 1. Abnormal ReturnruhiAinda não há avaliações

- Full Faa PDFDocumento392 páginasFull Faa PDFruhi100% (1)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- Business Report and Proposal WritingDocumento42 páginasBusiness Report and Proposal WritingruhiAinda não há avaliações

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Fraud, internal controls and cashDocumento35 páginasFraud, internal controls and cashruhiAinda não há avaliações

- 1.ad As BasicDocumento50 páginas1.ad As BasicruhiAinda não há avaliações

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (265)

- Test Bank For Principles of Risk Management and Insurance 12th Edition by RejdaDocumento10 páginasTest Bank For Principles of Risk Management and Insurance 12th Edition by Rejdajames90% (10)

- Full Faa PDFDocumento392 páginasFull Faa PDFruhi100% (1)

- BBDocumento2 páginasBBruhiAinda não há avaliações

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- CashFlow With SolutionsDocumento82 páginasCashFlow With SolutionsHermen Kapello100% (2)

- Fixed Income Chapter1Documento29 páginasFixed Income Chapter1ruhiAinda não há avaliações

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- 01 ITF Tutorial Review QuestionsDocumento4 páginas01 ITF Tutorial Review QuestionsNusrat AliAinda não há avaliações

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- How business processes, transaction systems, and enterprise applications improve organizational performanceDocumento7 páginasHow business processes, transaction systems, and enterprise applications improve organizational performanceahmedsalem2012Ainda não há avaliações

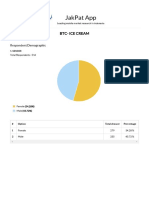

- PDF Report BTC - Ice Cream 3149 PDFDocumento87 páginasPDF Report BTC - Ice Cream 3149 PDFruhiAinda não há avaliações

- PDF Report BTC - Ice Cream 3149 PDFDocumento87 páginasPDF Report BTC - Ice Cream 3149 PDFruhiAinda não há avaliações

- How business processes, transaction systems, and enterprise applications improve organizational performanceDocumento7 páginasHow business processes, transaction systems, and enterprise applications improve organizational performanceahmedsalem2012Ainda não há avaliações

- 01 ITF Tutorial Review QuestionsDocumento4 páginas01 ITF Tutorial Review QuestionsNusrat AliAinda não há avaliações

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- NaDocumento5 páginasNaruhiAinda não há avaliações

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2219)

- OB - Situations - May 09, 2016Documento10 páginasOB - Situations - May 09, 2016ruhiAinda não há avaliações

- Macroeconomic AnalysisDocumento5 páginasMacroeconomic AnalysisruhiAinda não há avaliações

- Macroeconomic AnalysisDocumento5 páginasMacroeconomic AnalysisruhiAinda não há avaliações

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Remington Jensen Dutch Bros Application PDFDocumento3 páginasRemington Jensen Dutch Bros Application PDFremingtonjensenAinda não há avaliações

- Bunag, JR v. CA 211 SCRA 441 (1992)Documento37 páginasBunag, JR v. CA 211 SCRA 441 (1992)Ruab PlosAinda não há avaliações

- PEOPLE V SYLVESTRE AND ATIENZA G.R. No. L-35748 PDFDocumento2 páginasPEOPLE V SYLVESTRE AND ATIENZA G.R. No. L-35748 PDFJM CamposAinda não há avaliações

- Peoria County Jail Booking Sheet For July 9 2016Documento10 páginasPeoria County Jail Booking Sheet For July 9 2016Journal Star police documentsAinda não há avaliações

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (119)

- PAM Contract 2006 (Without Quantities)Documento54 páginasPAM Contract 2006 (Without Quantities)Kj LeeAinda não há avaliações

- Contributory NegligenceDocumento12 páginasContributory Negligencesai kiran gudisevaAinda não há avaliações

- #1 Filed ComplaintDocumento31 páginas#1 Filed ComplaintScott Magruder100% (1)

- Case Digest - Week 5.3Documento85 páginasCase Digest - Week 5.3Van John MagallanesAinda não há avaliações

- Legal Glossary Inttraduk Ingles-EspañolDocumento6 páginasLegal Glossary Inttraduk Ingles-EspañolAlexis WhiteAinda não há avaliações

- Civil Procedure Code Project Topics ListDocumento6 páginasCivil Procedure Code Project Topics ListArthi GaddipatiAinda não há avaliações

- TH e Question of Land Value in TanzaniaDocumento3 páginasTH e Question of Land Value in TanzaniaPraygod ManaseAinda não há avaliações

- 4th IMS Unision Moot MemoDocumento48 páginas4th IMS Unision Moot MemoAman Uniyal83% (6)

- Cases - Reserva TroncalDocumento14 páginasCases - Reserva TroncalSam ReyesAinda não há avaliações

- Unidad 5 - Present ProgressiveDocumento8 páginasUnidad 5 - Present Progressivedianis721Ainda não há avaliações

- Wiretapping 1Documento83 páginasWiretapping 1Tyler MaginnisAinda não há avaliações

- Assignment and Nomination Under Insurance PoliciesDocumento5 páginasAssignment and Nomination Under Insurance PoliciesNasma AbidiAinda não há avaliações

- SolOil, Inc. vs. PCA (G.R. No. 174806, August 11, 2010)Documento10 páginasSolOil, Inc. vs. PCA (G.R. No. 174806, August 11, 2010)Fergen Marie WeberAinda não há avaliações

- III. Void MarriagesDocumento149 páginasIII. Void MarriagesSophia Nicole Marquilencia FajardoAinda não há avaliações

- Arreza vs. ToyoDocumento1 páginaArreza vs. ToyoDawn Pocholo SantosAinda não há avaliações

- Transfer Risk Sale GoodsDocumento5 páginasTransfer Risk Sale GoodsVishal BothraAinda não há avaliações

- G.R. No. 178467. April 26, 2017. - Carbonell vs. Metropolitan Bank and Trust CompanyDocumento2 páginasG.R. No. 178467. April 26, 2017. - Carbonell vs. Metropolitan Bank and Trust CompanyFrancis Coronel Jr.100% (1)

- La Razon v. Union Insurance (Insurance Digest)Documento3 páginasLa Razon v. Union Insurance (Insurance Digest)Francisco Ashley AcedilloAinda não há avaliações

- Right to Legal Representation in Domestic EnquiriesDocumento19 páginasRight to Legal Representation in Domestic EnquiriesdivyavishalAinda não há avaliações

- Case Laws BDocumento2 páginasCase Laws Bmuhammad zainAinda não há avaliações

- Liblik and Others v. Estonia: ECtHR judgment on secret surveillance and length of criminal proceedingsDocumento42 páginasLiblik and Others v. Estonia: ECtHR judgment on secret surveillance and length of criminal proceedingsAnaGeoAinda não há avaliações

- Teacher marriage to student upheld but dismissal allowedDocumento20 páginasTeacher marriage to student upheld but dismissal allowedJerick HernandezAinda não há avaliações

- Table of ContentsDocumento5 páginasTable of ContentsKristina KarenAinda não há avaliações

- SECURITIES FRAUD CASEDocumento2 páginasSECURITIES FRAUD CASERonnieEngging100% (1)

- Premiere Development Bank V FloresDocumento3 páginasPremiere Development Bank V FloresLUNAAinda não há avaliações

- Quotation: Item Part No. Superceded by Make Description QTY UOM Unit Extended DeliveryDocumento4 páginasQuotation: Item Part No. Superceded by Make Description QTY UOM Unit Extended DeliveryhamadaabdelgawadAinda não há avaliações

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingNo EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingNota: 4.5 de 5 estrelas4.5/5 (97)

- Buffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorNo EverandBuffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorNota: 4.5 de 5 estrelas4.5/5 (132)

- Getting Through: Cold Calling Techniques To Get Your Foot In The DoorNo EverandGetting Through: Cold Calling Techniques To Get Your Foot In The DoorNota: 4.5 de 5 estrelas4.5/5 (63)