Você também pode gostar

- AGISDocumento31 páginasAGISPadmanabha Narayan100% (2)

- About The AuthorDocumento11 páginasAbout The AuthorYassi CurtisAinda não há avaliações

- Accounting Information Systems 13th Edition Romney Solutions Manual Full Chapter PDFDocumento68 páginasAccounting Information Systems 13th Edition Romney Solutions Manual Full Chapter PDFStephenBowenbxtm100% (16)

- Cash Management RMS WhitepaperDocumento12 páginasCash Management RMS WhitepapertanbetAinda não há avaliações

- Debt ManagementDocumento38 páginasDebt ManagementhemaguruAinda não há avaliações

- Best Practice Bank Feed WorkflowsDocumento6 páginasBest Practice Bank Feed Workflowsvanosoy19Ainda não há avaliações

- Petty Cash FundDocumento4 páginasPetty Cash Fundraa.aceroAinda não há avaliações

- Cash and Marketable Securities ManagementDocumento53 páginasCash and Marketable Securities ManagementRaza SamiAinda não há avaliações

- MARIA M Case Study03..Documento3 páginasMARIA M Case Study03..Charrie Faye Magbitang HernandezAinda não há avaliações

- AR Training Manual - Basic Concepts - PDFDocumento93 páginasAR Training Manual - Basic Concepts - PDFAlaa Mostafa100% (14)

- Wire TransferDocumento20 páginasWire TransfernomaanahmadshahAinda não há avaliações

- A Beginners Guide to QuickBooks Online: The Quick Reference Guide for Nonprofits and Small BusinessesNo EverandA Beginners Guide to QuickBooks Online: The Quick Reference Guide for Nonprofits and Small BusinessesAinda não há avaliações

- Chapter 13Documento40 páginasChapter 13Diandra OlivianiAinda não há avaliações

- 10 Exercises BE Solutions-1Documento40 páginas10 Exercises BE Solutions-1loveliangel0% (2)

- 8 Critical Success Factors For Credit and CollectionsDocumento16 páginas8 Critical Success Factors For Credit and CollectionsRhap Sody0% (1)

- Introduction To Financial Accounting 11th Edition Horngren Solutions Manual 1Documento49 páginasIntroduction To Financial Accounting 11th Edition Horngren Solutions Manual 1carolyn100% (43)

- Introduction To Financial Accounting 11Th Edition Horngren Solutions Manual Full Chapter PDFDocumento36 páginasIntroduction To Financial Accounting 11Th Edition Horngren Solutions Manual Full Chapter PDFmargaret.clark112100% (13)

- Advance Banking SkillsDocumento65 páginasAdvance Banking SkillsHumberto PortilloAinda não há avaliações

- Steps To Switch: From Spreadsheets To Cloud-Based Expense ManagemenDocumento22 páginasSteps To Switch: From Spreadsheets To Cloud-Based Expense ManagemenBuddy VeAinda não há avaliações

- Reasons To Automate ExpensesDocumento16 páginasReasons To Automate ExpensesBharat KhiaraAinda não há avaliações

- Suggested Answers To Discussion Questions 12.1Documento9 páginasSuggested Answers To Discussion Questions 12.1kkmoopAinda não há avaliações

- ch7 Allowance Method For UncollectableDocumento12 páginasch7 Allowance Method For UncollectablemartinAinda não há avaliações

- Cash & Internal ControlDocumento17 páginasCash & Internal Controlginish12Ainda não há avaliações

- PorterSM03final FinAccDocumento60 páginasPorterSM03final FinAccGemini_0804100% (1)

- The Controller's Function: The Work of the Managerial AccountantNo EverandThe Controller's Function: The Work of the Managerial AccountantAinda não há avaliações

- AP/AR Netting: 1.define Netting Control AccountDocumento11 páginasAP/AR Netting: 1.define Netting Control AccountVijay SharmaAinda não há avaliações

- 1z0-506 Questions and Answers HTTP WWW - Testsnow.net TXT 1 1288 14182.HTMLDocumento102 páginas1z0-506 Questions and Answers HTTP WWW - Testsnow.net TXT 1 1288 14182.HTMLmurali0% (1)

- Bank Reconciliation Case StudyDocumento52 páginasBank Reconciliation Case StudyParth Desai100% (4)

- Bizmanualz Accounting Policies and Procedures SampleDocumento8 páginasBizmanualz Accounting Policies and Procedures SamplePaulo LindgrenAinda não há avaliações

- Accounts Payable Balance Sheet Entries: How Do They Show Up?Documento9 páginasAccounts Payable Balance Sheet Entries: How Do They Show Up?atia fawzyAinda não há avaliações

- R12 Oracle PayablesDocumento50 páginasR12 Oracle PayablesCGAinda não há avaliações

- C2CDocumento14 páginasC2Cinguides IndiaAinda não há avaliações

- ACYASR 1 Essay 2Documento4 páginasACYASR 1 Essay 2JasperAinda não há avaliações

- QB Using Bank FeedsDocumento6 páginasQB Using Bank Feedsvanosoy19Ainda não há avaliações

- Horizontal Analysis - Horizontal Analysis Is Used in Financial Statement Analysis To CompareDocumento3 páginasHorizontal Analysis - Horizontal Analysis Is Used in Financial Statement Analysis To CompareShanelle SilmaroAinda não há avaliações

- Best Practices CashDocumento7 páginasBest Practices CashMichelle GoAinda não há avaliações

- Working Capital ManagementDocumento6 páginasWorking Capital ManagementMike TyagiAinda não há avaliações

- Auditing and Assurance Services A Systematic Approach 9th Edition Messier Solutions ManualDocumento11 páginasAuditing and Assurance Services A Systematic Approach 9th Edition Messier Solutions Manualdubitateswanmarkm4nvo100% (23)

- Oracle AP Closing ProceduresDocumento12 páginasOracle AP Closing ProcedureshupatelAinda não há avaliações

- PWC ArDocumento11 páginasPWC Aramulya_malleshAinda não há avaliações

- Treasury Alliance Cash Pooling White PaperDocumento16 páginasTreasury Alliance Cash Pooling White PaperShilpa KogantiAinda não há avaliações

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineNo EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineAinda não há avaliações

- PayPie WhitepaperDocumento23 páginasPayPie WhitepaperDesvaroAinda não há avaliações

- 13 NAW To Be - Bank ReconciliationDocumento11 páginas13 NAW To Be - Bank ReconciliationsivasivasapAinda não há avaliações

- Sap C - Fsutil - 60 - 80 QaDocumento32 páginasSap C - Fsutil - 60 - 80 QaKushal SharmaAinda não há avaliações

- Bank Statement To Cash Reconciliation: EMO CriptDocumento24 páginasBank Statement To Cash Reconciliation: EMO CriptsmohammedsaadAinda não há avaliações

- Proactive Collections Management: Using Artificial Intelligence To Predict Invoice Payment Dates By: Sonali NandaDocumento22 páginasProactive Collections Management: Using Artificial Intelligence To Predict Invoice Payment Dates By: Sonali NandaLautaro PainevilAinda não há avaliações

- Bizmanualz Accounting Policies and Procedures SampleDocumento9 páginasBizmanualz Accounting Policies and Procedures SampleIndraAinda não há avaliações

- Auditing and Assurance Services A Systematic Approach 11Th Edition Messier Solutions Manual Full Chapter PDFDocumento34 páginasAuditing and Assurance Services A Systematic Approach 11Th Edition Messier Solutions Manual Full Chapter PDFrickeybrock6oihx100% (14)

- Illustrative Audit Case: Keystone Computers & Networks, IncDocumento6 páginasIllustrative Audit Case: Keystone Computers & Networks, Incvaratvai0% (3)

- Accounting Information System: September 2015Documento20 páginasAccounting Information System: September 2015Ermi ManAinda não há avaliações

- WhitePaper - Guide To Adopting Best Practices & Digitalisation of Accounts PayableDocumento17 páginasWhitePaper - Guide To Adopting Best Practices & Digitalisation of Accounts PayableJayant JoshiAinda não há avaliações

- Chapter 13Documento61 páginasChapter 13frq qqr70% (20)

- Auditing A Risk Based Approach To Conducting A Quality Audit Johnstone 10th Edition Solutions ManualDocumento57 páginasAuditing A Risk Based Approach To Conducting A Quality Audit Johnstone 10th Edition Solutions ManualRichardThomasrfizy100% (38)

- Rais12 SM CH12Documento46 páginasRais12 SM CH12Chris Search100% (1)

- شابتر ٧Documento36 páginasشابتر ٧Hamza MahmoudAinda não há avaliações

- Record KeepingDocumento11 páginasRecord Keepingr.jeyashankar9550Ainda não há avaliações

- AFLI Meeting Minutes - Taal Eruption Response PlanDocumento16 páginasAFLI Meeting Minutes - Taal Eruption Response PlanMark CentenoAinda não há avaliações

- List of Financial Management Dissertation Topics: Money Measurement ConceptsDocumento3 páginasList of Financial Management Dissertation Topics: Money Measurement ConceptsMark CentenoAinda não há avaliações

- Compressed Air JournalDocumento12 páginasCompressed Air JournalMark Centeno100% (1)

- A Simple Guide To Gemba Walk Ebook - PD PDFDocumento12 páginasA Simple Guide To Gemba Walk Ebook - PD PDFMark CentenoAinda não há avaliações

- Seapac Philippines Case StudyDocumento21 páginasSeapac Philippines Case StudyMark CentenoAinda não há avaliações

- Ebara PumpDocumento25 páginasEbara PumpMark CentenoAinda não há avaliações

- HACCP DetailsDocumento3 páginasHACCP DetailsMark CentenoAinda não há avaliações

- Controllership Case StudyDocumento50 páginasControllership Case StudyMark CentenoAinda não há avaliações

- T-42 PDDocumento2 páginasT-42 PDMark CentenoAinda não há avaliações

- Organizational - STRAMADocumento30 páginasOrganizational - STRAMAMark CentenoAinda não há avaliações

- Hy Andritz Pumps Portfolio en - PDDocumento45 páginasHy Andritz Pumps Portfolio en - PDMark CentenoAinda não há avaliações

- Water Maintenance ChecklistDocumento1 páginaWater Maintenance ChecklistMark CentenoAinda não há avaliações

- FAC-2012-002 (Genset)Documento14 páginasFAC-2012-002 (Genset)Mark CentenoAinda não há avaliações

- IIAR Traininig GuideDocumento26 páginasIIAR Traininig GuideMark Centeno100% (4)

- True or False Conceptual Framework Set 2Documento2 páginasTrue or False Conceptual Framework Set 2Demi Pardillo100% (1)

- Aud Quiz No.3Documento3 páginasAud Quiz No.3Clarice GonzalesAinda não há avaliações

- Unity University College School of Distance and Continuing Education Worksheet For Auditing II (Acct 412)Documento3 páginasUnity University College School of Distance and Continuing Education Worksheet For Auditing II (Acct 412)ዝምታ ተሻለAinda não há avaliações

- Journal Home GridDocumento1 páginaJournal Home Grid03217925346Ainda não há avaliações

- Acc 201 - Final Project Workbook-DeSKTOP-5TE6TIFDocumento34 páginasAcc 201 - Final Project Workbook-DeSKTOP-5TE6TIFTera McKnight95% (19)

- V & Vi Bcom Regular Syllabus Final Nep 17-9-2023 Bos ApprovedDocumento48 páginasV & Vi Bcom Regular Syllabus Final Nep 17-9-2023 Bos ApprovedChethan MallikarjunAinda não há avaliações

- Auditing Theory - Audit ReportDocumento26 páginasAuditing Theory - Audit ReportCarina Espallardo-RelucioAinda não há avaliações

- Lesson 6 Accounting For Merchandising Business Part 2 ExercisesDocumento9 páginasLesson 6 Accounting For Merchandising Business Part 2 ExercisesTalented Kim SunooAinda não há avaliações

- Accounting-Financial Statements of Companies-1653399167327513Documento37 páginasAccounting-Financial Statements of Companies-1653399167327513Badhrinath ShanmugamAinda não há avaliações

- bài tập tổng hợp 1Documento10 páginasbài tập tổng hợp 1Hoàng Bảo TrâmAinda não há avaliações

- Solution Manual Auditing Chapter 14 Boynton 8th Ed.Documento18 páginasSolution Manual Auditing Chapter 14 Boynton 8th Ed.OlgaAinda não há avaliações

- Theory of Accounts-ReviewerDocumento27 páginasTheory of Accounts-ReviewerJeane BongalanAinda não há avaliações

- CH 06Documento4 páginasCH 06flrnciairnAinda não há avaliações

- IFRS 13 Fair Value Measurement FCPA Dr. James McFie 2017Documento59 páginasIFRS 13 Fair Value Measurement FCPA Dr. James McFie 2017Rafik BelkahlaAinda não há avaliações

- Example SDN BHDDocumento9 páginasExample SDN BHDputery_perakAinda não há avaliações

- New Government Accounting System NGASDocumento20 páginasNew Government Accounting System NGASIsiah Jarrett Trinidad Abille100% (1)

- Annual Report 2016-17 PDFDocumento83 páginasAnnual Report 2016-17 PDFRicha MandyaniAinda não há avaliações

- Tutorial 9Documento2 páginasTutorial 9Muntasir AhmmedAinda não há avaliações

- Test Bank MillanDocumento55 páginasTest Bank MillanBusiness MatterAinda não há avaliações

- Opening Balance Sheet As At: Total AssetsDocumento8 páginasOpening Balance Sheet As At: Total Assetsviji88mbaAinda não há avaliações

- Auditing and Assurance Services 15th Edition Chapter 3 Homework AnswersDocumento5 páginasAuditing and Assurance Services 15th Edition Chapter 3 Homework AnswersPenghui Shi50% (2)

- Ratio Analysis 1Documento2 páginasRatio Analysis 1yogeshgharpureAinda não há avaliações

- Chapter 4 Test BanksDocumento7 páginasChapter 4 Test BanksNineteen AùgùstAinda não há avaliações

- Al Khidmat Foundation Pakistan Audit & Compliance DepartmentDocumento2 páginasAl Khidmat Foundation Pakistan Audit & Compliance DepartmentFarooq Maqbool100% (1)

- 02 J. Amernic - A Case Study in Corporate Financial Reporting - Massey-Ferguson's Visible Accounting Decisions 1970-1987Documento43 páginas02 J. Amernic - A Case Study in Corporate Financial Reporting - Massey-Ferguson's Visible Accounting Decisions 1970-1987Fabian QuincheAinda não há avaliações

- EUROPEAN FLAX Checklist For Processors V2.0 October 2019 1Documento1 páginaEUROPEAN FLAX Checklist For Processors V2.0 October 2019 1Isabel MarquesAinda não há avaliações

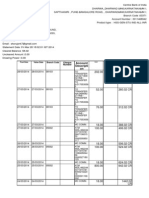

- Account Descripti On: Cheque NumberDocumento12 páginasAccount Descripti On: Cheque NumberSrujan KulkarniAinda não há avaliações

- MCQ Financial Management B Com Sem 5 PDFDocumento17 páginasMCQ Financial Management B Com Sem 5 PDFRadhika Bhargava100% (2)

- ACCO 101 Partnership Formation For Practice SolvingDocumento2 páginasACCO 101 Partnership Formation For Practice SolvingFionna Rei DeGaliciaAinda não há avaliações

- Module 1 Auditing ConceptsDocumento21 páginasModule 1 Auditing ConceptsDura LexAinda não há avaliações