Você também pode gostar

- Colorful Chalkboard Classroom Labels and OrganizersNo EverandColorful Chalkboard Classroom Labels and OrganizersAinda não há avaliações

- 2017-03 Country Risk Assessment GBDocumento1 página2017-03 Country Risk Assessment GBRaazia ImranAinda não há avaliações

- P231000887 - Barometre Q3 - 2023 - EN - CarteDocumento1 páginaP231000887 - Barometre Q3 - 2023 - EN - CarteNihad Zaaj El MetmaryAinda não há avaliações

- COFACE BAROMETRE T22022 Carte VGBDocumento1 páginaCOFACE BAROMETRE T22022 Carte VGBJavier Guillén JáureguiAinda não há avaliações

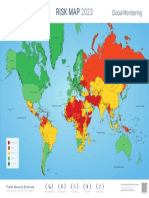

- Country Risk Assessment Map: 162 Countries Under The Magnifying GlassDocumento1 páginaCountry Risk Assessment Map: 162 Countries Under The Magnifying GlassROBERTO ZABALETA TAMAYOAinda não há avaliações

- Coface+Country+Risk+Map Q1-2021 ENG V CHDocumento1 páginaCoface+Country+Risk+Map Q1-2021 ENG V CHOmar PachonAinda não há avaliações

- Country Risk Assessment Map: 162 Countries Under The Magnifying GlassDocumento1 páginaCountry Risk Assessment Map: 162 Countries Under The Magnifying GlassInnovación Comercio Internacional y aduanasAinda não há avaliações

- COFACE BAROMETRE T32022 Carte VGBDocumento1 páginaCOFACE BAROMETRE T32022 Carte VGBMartin Stephan Arias MedinaAinda não há avaliações

- Coface Barometer q3-2021 Carte enDocumento1 páginaCoface Barometer q3-2021 Carte enDuc Anh NguyenAinda não há avaliações

- Mapa Evaluaciones Riesgo País - 3T 2019: 160 Países Bajo La LupaDocumento1 páginaMapa Evaluaciones Riesgo País - 3T 2019: 160 Países Bajo La LupaBRYANRAMIREZAinda não há avaliações

- Map ENG With Text Jan 218 PDFDocumento1 páginaMap ENG With Text Jan 218 PDFChris VegaAinda não há avaliações

- Map With Comment en PDFDocumento1 páginaMap With Comment en PDFyyyAinda não há avaliações

- Esp Mapa Riesgo País Q2 2022Documento1 páginaEsp Mapa Riesgo País Q2 2022Manuel DuarteAinda não há avaliações

- Coface Barometre-T22023 Carte ENDocumento1 páginaCoface Barometre-T22023 Carte ENJorge PHAGOUAPEAinda não há avaliações

- Eulerhermes World Risk Map 2020Documento1 páginaEulerhermes World Risk Map 2020mohamed el amine brahimiAinda não há avaliações

- World00 PDFDocumento1 páginaWorld00 PDFtyiirxbdvolggdkmmoAinda não há avaliações

- BOLETIN 106 ECONOMIA POLITICA Y REVOLUCION JUNIO 2022 - CompressedDocumento15 páginasBOLETIN 106 ECONOMIA POLITICA Y REVOLUCION JUNIO 2022 - CompressedLisyeira ChambucoAinda não há avaliações

- AbortionMap2014 PDFDocumento1 páginaAbortionMap2014 PDFJosefina CerbinoAinda não há avaliações

- Global Mobility Risk Map 2019 en - 3 PDFDocumento1 páginaGlobal Mobility Risk Map 2019 en - 3 PDFqasssdewAinda não há avaliações

- QXP Risk Map q2 2022Documento1 páginaQXP Risk Map q2 2022Farouk AnçaAinda não há avaliações

- World 45Documento1 páginaWorld 45VN PrasadAinda não há avaliações

- Peta Dunia - 3x2m YBM BRI Bright ScholarshipDocumento1 páginaPeta Dunia - 3x2m YBM BRI Bright ScholarshipZahira LailaAinda não há avaliações

- The World Today: Pacific OceanDocumento1 páginaThe World Today: Pacific OceanChickoy RamirezAinda não há avaliações

- Map ContinentDocumento1 páginaMap ContinentRobert SarabiaAinda não há avaliações

- 2022 12 06 A3M Risk Map 2023Documento1 página2022 12 06 A3M Risk Map 2023oauh9uewhAinda não há avaliações

- Trisavo Risk Map 2022Documento1 páginaTrisavo Risk Map 2022friska_arianiAinda não há avaliações

- Mapa Mundi - : Josias Isaac Churata ArcheDocumento1 páginaMapa Mundi - : Josias Isaac Churata ArcheJose ChurataAinda não há avaliações

- Map - The World in 1945Documento1 páginaMap - The World in 1945cartographica96% (27)

- WALM Poster - 3 1 2024Documento1 páginaWALM Poster - 3 1 2024YouTubeAinda não há avaliações

- Catalogue MacraneDocumento8 páginasCatalogue MacraneGokhan CetinkayaAinda não há avaliações

- Global War 2025 MapDocumento1 páginaGlobal War 2025 Maplupus00Ainda não há avaliações

- Growing Tobaccco AtlasDocumento1 páginaGrowing Tobaccco Atlasfrank_rizzo1ukAinda não há avaliações

- Oceano Ártico Oceano Ártico: RussiaDocumento1 páginaOceano Ártico Oceano Ártico: RussiaRosa Isabel LopesAinda não há avaliações

- United MapDocumento1 páginaUnited MapeducationvAinda não há avaliações

- Atradius Country Risk MapDocumento1 páginaAtradius Country Risk MapKaninAinda não há avaliações

- Marpol Annex Vi: Countries and Territories That Have RatifiedDocumento1 páginaMarpol Annex Vi: Countries and Territories That Have RatifiedMostafa ShaheenAinda não há avaliações

- Country Risk RatingDocumento1 páginaCountry Risk Ratingjsykqyyhz4Ainda não há avaliações

- Mapa MundiDocumento1 páginaMapa MundiAdolfo MolinaAinda não há avaliações

- OGM Office 1-1Documento1 páginaOGM Office 1-1John Kenneth Del ValleAinda não há avaliações

- Global Tobacco Consumption MapDocumento1 páginaGlobal Tobacco Consumption Maptanmaypurohit100% (2)

- Department of Public Works and HighwaysDocumento4 páginasDepartment of Public Works and HighwaysRazul DaranginaAinda não há avaliações

- Peta Dunia - 3x2mDocumento1 páginaPeta Dunia - 3x2mMuhamad FikriAinda não há avaliações

- Europe 230825Documento1 páginaEurope 230825VedaWarlockAinda não há avaliações

- World Map 4651 Oct22 115%Documento1 páginaWorld Map 4651 Oct22 115%VooDooLily Publishing HouseAinda não há avaliações

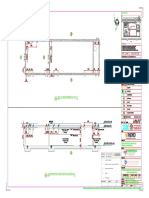

- A1 - Baguio Project - DentalDocumento1 páginaA1 - Baguio Project - DentalNeil AldousAinda não há avaliações

- 05Documento1 página05SLPlanner PlannerAinda não há avaliações

- Janshakti FPC - 04.09.2022-OPTION-02Documento1 páginaJanshakti FPC - 04.09.2022-OPTION-02Shekhar PhaseAinda não há avaliações

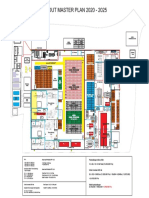

- Layout Master Plan 2020 - 2025: Jalur ForkliftDocumento1 páginaLayout Master Plan 2020 - 2025: Jalur ForkliftIanAinda não há avaliações

- French 10 12 Nov 2Documento26 páginasFrench 10 12 Nov 2Bright kashitaAinda não há avaliações

- Notes:: Key PlanDocumento1 páginaNotes:: Key PlanSLPlanner PlannerAinda não há avaliações

- Notes:: Key PlanDocumento1 páginaNotes:: Key PlanSLPlanner PlannerAinda não há avaliações

- 2017 140 Schengen A1 WebDocumento1 página2017 140 Schengen A1 WebjmpedrazoAinda não há avaliações

- Canada at A GlanceDocumento6 páginasCanada at A GlanceInvestInCanadaAinda não há avaliações

- Electrical Drawing For 2BHK HouseDocumento1 páginaElectrical Drawing For 2BHK HousesmallhouseconstructionsAinda não há avaliações

- Girl's Hostel (View-2)Documento1 páginaGirl's Hostel (View-2)keshav chaturvediAinda não há avaliações

- BLGF Site Development Plan RevisedDocumento1 páginaBLGF Site Development Plan Revisedthethird20Ainda não há avaliações

- Notes:: Key PlanDocumento1 páginaNotes:: Key PlanSLPlanner PlannerAinda não há avaliações

- PLN003 Sh1of1Documento1 páginaPLN003 Sh1of1Rodney ZephaniaAinda não há avaliações

- Rig2-Ee-100 - 103-Ee-100Documento1 páginaRig2-Ee-100 - 103-Ee-100Shamim ImtiazAinda não há avaliações

- VENGALA NEERAJA DEVI SULBD-ModelDocumento1 páginaVENGALA NEERAJA DEVI SULBD-Modelarun kumarAinda não há avaliações

- DS11 Uw - 0Documento2 páginasDS11 Uw - 013421301508Ainda não há avaliações

- A Beginner's Introduction To Typesetting With LATEX de Peter FlynnDocumento275 páginasA Beginner's Introduction To Typesetting With LATEX de Peter FlynnAnderson Soares AraujoAinda não há avaliações

- Kawasaki Gas Turbine PDFDocumento45 páginasKawasaki Gas Turbine PDF13421301508100% (1)

- BrochureDocumento13 páginasBrochure13421301508Ainda não há avaliações

- 4-4. 37 Flared Tube Fittings For SAE J514 2015-Rev.1Documento56 páginas4-4. 37 Flared Tube Fittings For SAE J514 2015-Rev.113421301508Ainda não há avaliações

- The Visual L Tex Faq: 1 Magna CondimentumDocumento33 páginasThe Visual L Tex Faq: 1 Magna Condimentumppedro07Ainda não há avaliações

- The Not So Short Introduction To L Tex 2Ε: Orl Tex 2Ε In MinutesDocumento171 páginasThe Not So Short Introduction To L Tex 2Ε: Orl Tex 2Ε In Minuteslexes26Ainda não há avaliações

- PIM130B1 - Honeywell AGT1500 Archived 03 2009 PDFDocumento10 páginasPIM130B1 - Honeywell AGT1500 Archived 03 2009 PDF13421301508Ainda não há avaliações

- H JDocumento146 páginasH Japi-26146280Ainda não há avaliações

- EpslatexDocumento124 páginasEpslatexJaimeHoAinda não há avaliações

- 316 - 316l 不锈钢参数 PDFDocumento7 páginas316 - 316l 不锈钢参数 PDF13421301508Ainda não há avaliações

- Wxglade Manual PDFDocumento57 páginasWxglade Manual PDF13421301508Ainda não há avaliações

- APUDocumento211 páginasAPURups Mats100% (6)

- 1981GN08Documento90 páginas1981GN0813421301508Ainda não há avaliações

- Pt6t Gearbox PDFDocumento117 páginasPt6t Gearbox PDF13421301508Ainda não há avaliações

- Latex IntroductionDocumento1 páginaLatex IntroductioniordacheAinda não há avaliações

- Ams5662 PDFDocumento11 páginasAms5662 PDF13421301508Ainda não há avaliações

- L TEX: An Unofficial Reference ManualDocumento109 páginasL TEX: An Unofficial Reference ManualAritra BhattacharjeeAinda não há avaliações

- LaTeX - Modifying LaTeXDocumento7 páginasLaTeX - Modifying LaTeXgiunghiAinda não há avaliações

- Usr GuideDocumento33 páginasUsr GuidebettyKaloAinda não há avaliações

- EASA Arrius 2 Series EnginesDocumento14 páginasEASA Arrius 2 Series Engines13421301508Ainda não há avaliações

- PW 100Documento3 páginasPW 100subir12bd100% (1)

- Honeywell AGT1500Documento10 páginasHoneywell AGT150013421301508Ainda não há avaliações

- PWC 150A Capabilities Vector 10.16Documento1 páginaPWC 150A Capabilities Vector 10.1613421301508Ainda não há avaliações

- Building A Model Steam Engine From Scratch Chapter 1, 150 121Documento19 páginasBuilding A Model Steam Engine From Scratch Chapter 1, 150 121Liam Clink100% (2)

- Description:: AWS A5.4 E308-16 JIS Z3221 ES308-16 EN 1600 E 19 9 R 1 2 Covered Electrodes For Stainless SteelDocumento1 páginaDescription:: AWS A5.4 E308-16 JIS Z3221 ES308-16 EN 1600 E 19 9 R 1 2 Covered Electrodes For Stainless Steel13421301508Ainda não há avaliações

- Ams 5608Documento8 páginasAms 560813421301508Ainda não há avaliações

- Birzeit University Department of Economics Public Finance, ECON 434Documento2 páginasBirzeit University Department of Economics Public Finance, ECON 434Dina OdehAinda não há avaliações

- JAIIB 2024 BrochureDocumento13 páginasJAIIB 2024 BrochureSUBRAMANIAN NAGAAinda não há avaliações

- Guidance For The 2023 Reporting of Capital and Financial Condition Testing For Life and Health, P&C and Mortgage InsurersDocumento19 páginasGuidance For The 2023 Reporting of Capital and Financial Condition Testing For Life and Health, P&C and Mortgage InsurersCalvinAinda não há avaliações

- August 2023 BOLTDocumento93 páginasAugust 2023 BOLTADITI VAISHNAVAinda não há avaliações

- Art. Internationalization Processes of Emerging Economy MNEs PDFDocumento23 páginasArt. Internationalization Processes of Emerging Economy MNEs PDFjcgarriazoAinda não há avaliações

- Ecuador's Ministry of Tourism's Seeks Foreign Investment in The Galapagos IslandsDocumento4 páginasEcuador's Ministry of Tourism's Seeks Foreign Investment in The Galapagos IslandsSalvaGalapagosAinda não há avaliações

- BAM Certificate Eng One PagerDocumento1 páginaBAM Certificate Eng One PagerWalid El AmineAinda não há avaliações

- Examen Final 2023 Ingles 3Documento4 páginasExamen Final 2023 Ingles 3Mariano F DiazAinda não há avaliações

- CTET Math Study MaterialDocumento4 páginasCTET Math Study MaterialManisha KandiyalAinda não há avaliações

- ModuleDocumento10 páginasModuleDiane Gutierrez100% (1)

- SDMC Volume II Project Information Memorandum - SWM - VF PDFDocumento192 páginasSDMC Volume II Project Information Memorandum - SWM - VF PDFRWA JhuljhuliAinda não há avaliações

- ComparitiveDocumento6 páginasComparitivesanath vsAinda não há avaliações

- India: Population Rank Growth RateDocumento2 páginasIndia: Population Rank Growth RateKaruna PatilAinda não há avaliações

- BY Wankar Sir: Indian Railways Group A ServiceDocumento14 páginasBY Wankar Sir: Indian Railways Group A Servicekshitij vaidyaAinda não há avaliações

- Abdul Majeed - MBA CS #3 Emirates AirlineDocumento7 páginasAbdul Majeed - MBA CS #3 Emirates AirlineSufi MajeedAinda não há avaliações

- TCW (Task For Finals)Documento2 páginasTCW (Task For Finals)Alyson GregorioAinda não há avaliações

- Beijing Declaration 2018Documento4 páginasBeijing Declaration 2018Celyn Cemine MapulaAinda não há avaliações

- Indifference Curves Between Goods Bads & Neuters PDFDocumento10 páginasIndifference Curves Between Goods Bads & Neuters PDFHarshvardhan Kothari100% (1)

- UntitledDocumento54 páginasUntitledMyla AlulodAinda não há avaliações

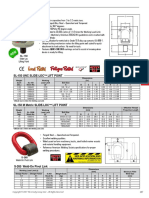

- Lifting Points: Slide-Loc Lifting PointDocumento1 páginaLifting Points: Slide-Loc Lifting PointAnonymous hHWOMl4FvAinda não há avaliações

- Solutions Manual Managing Business Process Flows 3rd Edition by Ravi Anupindi SampleDocumento12 páginasSolutions Manual Managing Business Process Flows 3rd Edition by Ravi Anupindi Sampleمحمد مصطفى0% (1)

- All Alerts For 17 Jan - ChartinkDocumento17 páginasAll Alerts For 17 Jan - Chartinkkashinath09Ainda não há avaliações

- Why Do Local Governments Return Money To The Treasury?Documento1 páginaWhy Do Local Governments Return Money To The Treasury?African Centre for Media ExcellenceAinda não há avaliações

- Valuation Lucky CementDocumento2 páginasValuation Lucky CementAhsan KhanAinda não há avaliações

- FSA Chapter 7Documento3 páginasFSA Chapter 7Nadia ZahraAinda não há avaliações

- Instance VRB 2021-22.xmlDocumento147 páginasInstance VRB 2021-22.xmlSarah AliceAinda não há avaliações

- Merchant Merchant Mobile S No Shop Name Shop Address City 83 Abhijeet Saha 99065620Documento167 páginasMerchant Merchant Mobile S No Shop Name Shop Address City 83 Abhijeet Saha 99065620Delta PayAinda não há avaliações

- Ratio Analysis - Mining IndustriesDocumento30 páginasRatio Analysis - Mining IndustriesKaustubh TiwaryAinda não há avaliações

- Invoice Zoom YKB 2022Documento2 páginasInvoice Zoom YKB 2022Dian ElgaAinda não há avaliações

- Operation and Maintenance Manual: Belt DiverterDocumento38 páginasOperation and Maintenance Manual: Belt DiverterTinTunNaingAinda não há avaliações