Você também pode gostar

- Tds Rate ChartDocumento49 páginasTds Rate ChartSANJEEVAinda não há avaliações

- Accounts & Taxations Interview Related NotesDocumento5 páginasAccounts & Taxations Interview Related NotesRahul Baburao AbhaleAinda não há avaliações

- Tds Rate Chart Fy 2018-19 Ay 2019-20 Tds Deposit-Return Due Dates-Interest-PenaltyDocumento2 páginasTds Rate Chart Fy 2018-19 Ay 2019-20 Tds Deposit-Return Due Dates-Interest-PenaltyNarayanakrishnan RAinda não há avaliações

- TDS - and - TCS Rate Chart 2024Documento5 páginasTDS - and - TCS Rate Chart 2024Taxation KTPL (Kalyani Techpark Taxation)Ainda não há avaliações

- TDS Rate Chart - FY 2021-22Documento3 páginasTDS Rate Chart - FY 2021-22Ram YadavAinda não há avaliações

- TDS and TCS Rate Chart 2023Documento5 páginasTDS and TCS Rate Chart 2023DEEPAK SHARMAAinda não há avaliações

- TDS and TCS-rate-chart-2023 RemovedDocumento4 páginasTDS and TCS-rate-chart-2023 Removeddurgeshsonawane65Ainda não há avaliações

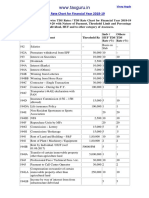

- WWW - Taxguru.in: TDS Rate Chart For Financial Year 2018-19Documento1 páginaWWW - Taxguru.in: TDS Rate Chart For Financial Year 2018-19Sunny NarangAinda não há avaliações

- TDS & TCS Rates Made EasyDocumento2 páginasTDS & TCS Rates Made Easykumar45caAinda não há avaliações

- TDS and TCS Rate Chart 2023Documento3 páginasTDS and TCS Rate Chart 2023praveenAinda não há avaliações

- TDS_and_TCS-rate-chart-2025Documento5 páginasTDS_and_TCS-rate-chart-2025jsparakhAinda não há avaliações

- Commonly used TDS Provisions for payments in IndiaDocumento17 páginasCommonly used TDS Provisions for payments in IndiaSonika GuptaAinda não há avaliações

- Revised TDS Wef 14.05.20Documento7 páginasRevised TDS Wef 14.05.20MANAN KOTHARIAinda não há avaliações

- TDS Rates For The ADocumento1 páginaTDS Rates For The AsadathnooriAinda não há avaliações

- TDS and TCS Rate Chart 2022Documento3 páginasTDS and TCS Rate Chart 2022Ajay ModiAinda não há avaliações

- Tds Rate Chart For Fy 21016Documento2 páginasTds Rate Chart For Fy 21016VedpalAinda não há avaliações

- TDS RATE CHART F.Y. 2019-20 (A.Y. 2020-21) : WWW - Bharatax.inDocumento1 páginaTDS RATE CHART F.Y. 2019-20 (A.Y. 2020-21) : WWW - Bharatax.inGajendra Singh Rajpurohit Chadwas IIIAinda não há avaliações

- Tds Income Tax Rates Fy 2010-11Documento13 páginasTds Income Tax Rates Fy 2010-11Surender KumarAinda não há avaliações

- TDS RATE CHART FY 2021-22-FinalDocumento5 páginasTDS RATE CHART FY 2021-22-FinalLeenaAinda não há avaliações

- TDS Rate Chart: Assessment Year 2011-12Documento1 páginaTDS Rate Chart: Assessment Year 2011-12Saravanan ElumalaiAinda não há avaliações

- TDS Rate Chart 2011 - 12Documento1 páginaTDS Rate Chart 2011 - 12m_y_chavanAinda não há avaliações

- TDS Rate & Tax Provisions For F.Y. 2019-20 (A.Y. 2020-21) : TDS Is Deducted On The Following Types of PaymentsDocumento10 páginasTDS Rate & Tax Provisions For F.Y. 2019-20 (A.Y. 2020-21) : TDS Is Deducted On The Following Types of PaymentsnagallanraoAinda não há avaliações

- TDS Rates Chart Fy 2020 21 Ay 2021 22Documento6 páginasTDS Rates Chart Fy 2020 21 Ay 2021 22Brijendra SinghAinda não há avaliações

- TDS Rate Chart FY 2021-2022: Section Code Nature of Payment Threshold (In RS.) TDS Rate (In %) Indv/HUF OthersDocumento7 páginasTDS Rate Chart FY 2021-2022: Section Code Nature of Payment Threshold (In RS.) TDS Rate (In %) Indv/HUF OthersRajAinda não há avaliações

- TDS Rates ChartDocumento11 páginasTDS Rates ChartSarat KumarAinda não há avaliações

- TDS (Tax Deducted at Source) Rate Chart For Financial Year 2010-11Documento13 páginasTDS (Tax Deducted at Source) Rate Chart For Financial Year 2010-11av_meshramAinda não há avaliações

- TdsPac RateCard 0910Documento2 páginasTdsPac RateCard 0910Ebanezer PaulrajAinda não há avaliações

- TDS Rates On Payments Other Than Salary and Wages To Residents (Including Domestic Companies)Documento3 páginasTDS Rates On Payments Other Than Salary and Wages To Residents (Including Domestic Companies)Prince RaichandAinda não há avaliações

- C.H. Padliya & Co.: Chartered AccountantsDocumento6 páginasC.H. Padliya & Co.: Chartered AccountantsSarat KumarAinda não há avaliações

- Tds Rate Chart Fy 2021-22Documento3 páginasTds Rate Chart Fy 2021-22Kadambari ShelkeAinda não há avaliações

- C.H. Padliya & Co.: Chartered AccountantsDocumento5 páginasC.H. Padliya & Co.: Chartered AccountantsSarat KumarAinda não há avaliações

- Current Changes of TDS: Presented By, Ghanshyam WatekarDocumento10 páginasCurrent Changes of TDS: Presented By, Ghanshyam Watekarpraful_watekarAinda não há avaliações

- Ssra Tds Rates 2021-2022Documento10 páginasSsra Tds Rates 2021-2022deepu kAinda não há avaliações

- TDS TCSDocumento231 páginasTDS TCSNarinderpal SinghAinda não há avaliações

- Rates of TDSDocumento30 páginasRates of TDSsudhanshu88g1Ainda não há avaliações

- TDS RATE CHART 2012-13Documento3 páginasTDS RATE CHART 2012-13jeet2211Ainda não há avaliações

- TDS Rate Chart For Financial Year 2020 21Documento1 páginaTDS Rate Chart For Financial Year 2020 21Arun RajaAinda não há avaliações

- For Tds On Non SalaryDocumento39 páginasFor Tds On Non SalaryicahimanshumehtaAinda não há avaliações

- Tax Deducted at Source (TDS)Documento7 páginasTax Deducted at Source (TDS)Rupali SinghAinda não há avaliações

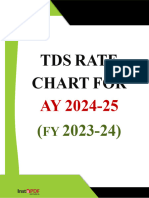

- Instapdf - in Tds Rate Chart Fy 2023 24 Ay 2024 25 355Documento7 páginasInstapdf - in Tds Rate Chart Fy 2023 24 Ay 2024 25 355skassociatetaxconsultantAinda não há avaliações

- TDS Chart FY 23-24Documento6 páginasTDS Chart FY 23-24kuldeep singhAinda não há avaliações

- TDS Rate Chart: (For Assessment Year 2017-18)Documento10 páginasTDS Rate Chart: (For Assessment Year 2017-18)Ajay SimonAinda não há avaliações

- Intro of TdsDocumento6 páginasIntro of Tdsshivani singhAinda não há avaliações

- Tax Deducted at Source UnitDocumento13 páginasTax Deducted at Source Unitsatyanarayan dashAinda não há avaliações

- TDS Rate Chart For FY 2022-2023 (AY 2023-2024) Including Budget 2022 Amendments - Taxguru - inDocumento15 páginasTDS Rate Chart For FY 2022-2023 (AY 2023-2024) Including Budget 2022 Amendments - Taxguru - inSachin GuptaAinda não há avaliações

- Tds Rate Chart Fy 2020Documento4 páginasTds Rate Chart Fy 2020KAUTUK KOLIAinda não há avaliações

- TDS Rate Chart 1Documento1 páginaTDS Rate Chart 1bulu1987Ainda não há avaliações

- TDS chart for FY 2013-14Documento1 páginaTDS chart for FY 2013-14Bharath Kumar JAinda não há avaliações

- Revised TDS Rate Chart (FY 2009-10)Documento1 páginaRevised TDS Rate Chart (FY 2009-10)haldharkAinda não há avaliações

- TDS 3Documento16 páginasTDS 3payal AgrawalAinda não há avaliações

- TDS Tax Challan Filing GuideDocumento3 páginasTDS Tax Challan Filing GuideSURABHI PATRAAinda não há avaliações

- Securities Brokerage Revenues World Summary: Market Values & Financials by CountryNo EverandSecurities Brokerage Revenues World Summary: Market Values & Financials by CountryAinda não há avaliações

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryAinda não há avaliações

- Telecommunications Reseller Revenues World Summary: Market Values & Financials by CountryNo EverandTelecommunications Reseller Revenues World Summary: Market Values & Financials by CountryAinda não há avaliações

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)No EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Nota: 3.5 de 5 estrelas3.5/5 (17)

- How to Do a 1031 Exchange of Real Estate: Using a 1031 Qualified Intermediary (Qi) 2Nd EditionNo EverandHow to Do a 1031 Exchange of Real Estate: Using a 1031 Qualified Intermediary (Qi) 2Nd EditionAinda não há avaliações

- Wired Telecommunications Carrier Lines World Summary: Market Values & Financials by CountryNo EverandWired Telecommunications Carrier Lines World Summary: Market Values & Financials by CountryAinda não há avaliações

- World Bank Project Business Opportunities for ICAI MembersDocumento15 páginasWorld Bank Project Business Opportunities for ICAI MembersSanjayThakkarAinda não há avaliações

- Exide Consumer Warranty - (Pro Rata Warranty - Pre Oct. 2012)Documento10 páginasExide Consumer Warranty - (Pro Rata Warranty - Pre Oct. 2012)SanjayThakkarAinda não há avaliações

- GST PMT-06 Payment Challan Form DetailsDocumento1 páginaGST PMT-06 Payment Challan Form DetailsSanjayThakkarAinda não há avaliações

- ICAI - Love U ZindagiDocumento18 páginasICAI - Love U ZindagiSanjayThakkarAinda não há avaliações

- RFPDocumento9 páginasRFPSanjayThakkarAinda não há avaliações

- Ussor 2012 Ecr CS-1 (BMK)Documento291 páginasUssor 2012 Ecr CS-1 (BMK)prasagnihotri100% (3)

- Number Item Name UnitDocumento1 páginaNumber Item Name UnitSanjayThakkarAinda não há avaliações

- Deemed Exports in GSTDocumento3 páginasDeemed Exports in GSTBharat JainAinda não há avaliações

- Cement - OPC 53 GST Rate ED 12.5% Rate (In RS.) Qty. Used (In Tonnes) Value (In RS.) GST Amount (In RS.) Base Value (Without GST)Documento13 páginasCement - OPC 53 GST Rate ED 12.5% Rate (In RS.) Qty. Used (In Tonnes) Value (In RS.) GST Amount (In RS.) Base Value (Without GST)SanjayThakkarAinda não há avaliações

- Wedding InvitationDocumento4 páginasWedding InvitationSanjayThakkarAinda não há avaliações

- StatementDocumento1 páginaStatementSanjayThakkarAinda não há avaliações

- Update On Changes Made in Real Estate SectorDocumento1 páginaUpdate On Changes Made in Real Estate SectorSanjayThakkarAinda não há avaliações

- Computer Generated Tm-Search ReportDocumento1 páginaComputer Generated Tm-Search ReportSanjayThakkarAinda não há avaliações

- ScriptDocumento1 páginaScriptSanjayThakkarAinda não há avaliações

- Whitepaper DragonDocumento26 páginasWhitepaper DragonSanjayThakkar100% (1)

- CST - Requirements and CST Requirements and Practical IssuesDocumento43 páginasCST - Requirements and CST Requirements and Practical IssuesSanjayThakkarAinda não há avaliações

- Partnership Deed Yug Spa & SalonDocumento8 páginasPartnership Deed Yug Spa & SalonSanjayThakkar0% (1)

- Board Resolution For Office UsageDocumento1 páginaBoard Resolution For Office UsageSanjayThakkarAinda não há avaliações

- Service Tax Notification No.09/2014 Dated 11th July, 2014Documento2 páginasService Tax Notification No.09/2014 Dated 11th July, 2014stephin k jAinda não há avaliações

- Class 40Documento2 páginasClass 40SanjayThakkarAinda não há avaliações

- Book redBus Ticket Ahmedabad to AnjarDocumento2 páginasBook redBus Ticket Ahmedabad to AnjarSanjayThakkarAinda não há avaliações

- Report of the Comptroller and Auditor General of India on Revenue Receipts for the year ended 31 March 2012Documento172 páginasReport of the Comptroller and Auditor General of India on Revenue Receipts for the year ended 31 March 2012SanjayThakkarAinda não há avaliações

- Form ST - 3Documento12 páginasForm ST - 3SanjayThakkarAinda não há avaliações

- CST - Requirements and CST Requirements and Practical IssuesDocumento43 páginasCST - Requirements and CST Requirements and Practical IssuesSanjayThakkarAinda não há avaliações

- Pre Marriage CouncelingDocumento21 páginasPre Marriage CouncelingSanjayThakkarAinda não há avaliações

- A Comprehensive Note On Input Tax Credit Under Gujarat VATDocumento42 páginasA Comprehensive Note On Input Tax Credit Under Gujarat VATSanjayThakkarAinda não há avaliações

- Enabling GVAT PracticeDocumento34 páginasEnabling GVAT PracticeSanjayThakkarAinda não há avaliações

- Ca. Pathik B. Shah: Value Added Tax Act 2003Documento36 páginasCa. Pathik B. Shah: Value Added Tax Act 2003SanjayThakkarAinda não há avaliações

- Applied Economics PPT 3Documento9 páginasApplied Economics PPT 3Angel AquinoAinda não há avaliações

- Research Methodology ProjectDocumento54 páginasResearch Methodology ProjectShaantanu Chhoker100% (2)

- Avarta WhitepaperDocumento33 páginasAvarta WhitepaperTrần Đỗ Trung MỹAinda não há avaliações

- Regulating Collective Investment Schemes in ZimbabweDocumento16 páginasRegulating Collective Investment Schemes in Zimbabwemsamala09Ainda não há avaliações

- ECON 1012 - ProductionDocumento62 páginasECON 1012 - ProductionTami GayleAinda não há avaliações

- 2019 Mid-Semester Mock Exam SolutionDocumento11 páginas2019 Mid-Semester Mock Exam SolutionMichael BobAinda não há avaliações

- Introduction To SBP-BSC and Vacancy AnnouncedDocumento2 páginasIntroduction To SBP-BSC and Vacancy AnnouncedAqeel AbbasAinda não há avaliações

- QuizDocumento13 páginasQuizMolay SharmaAinda não há avaliações

- LT bill details for mobile towerDocumento2 páginasLT bill details for mobile towerAMolAinda não há avaliações

- Signature Not VerifiedDocumento4 páginasSignature Not VerifiedMech RowdyAinda não há avaliações

- Acco Nov 2009 Eng MemoDocumento19 páginasAcco Nov 2009 Eng Memosadya98Ainda não há avaliações

- DOTgazette - Aug06 - July08.Documento196 páginasDOTgazette - Aug06 - July08.M Munir Qureishi100% (1)

- Journalizing TransactionsDocumento19 páginasJournalizing TransactionsChristine Paola D. LorenzoAinda não há avaliações

- Older Adults and BankruptcyDocumento28 páginasOlder Adults and BankruptcyvictorAinda não há avaliações

- Ministry of Finance and Financiel Services Joint Communiqué On Mauritius LeaksDocumento4 páginasMinistry of Finance and Financiel Services Joint Communiqué On Mauritius LeaksION NewsAinda não há avaliações

- Test 10 MDocumento9 páginasTest 10 MritikaAinda não há avaliações

- Profit and Loss Statement Template V11Documento24 páginasProfit and Loss Statement Template V11Rahul agarwal100% (4)

- BERLE Theory of Enterprise 1947Documento17 páginasBERLE Theory of Enterprise 1947Sofia DavidAinda não há avaliações

- Hajj Rituals - Ayatullah Sayyid Ali Al-Hussaini As-Sistani (Seestani) - XKPDocumento140 páginasHajj Rituals - Ayatullah Sayyid Ali Al-Hussaini As-Sistani (Seestani) - XKPIslamicMobilityAinda não há avaliações

- Man Acc Qs 1Documento6 páginasMan Acc Qs 1Tehniat Zafar0% (1)

- S Glass Limited: Working Capital Management INDocumento34 páginasS Glass Limited: Working Capital Management INtanu srivastava50% (2)

- Tata Motors' Acquisition of Jaguar Land RoverDocumento9 páginasTata Motors' Acquisition of Jaguar Land Roverajinkya8400Ainda não há avaliações

- Thesis Proposal For MbsDocumento5 páginasThesis Proposal For Mbsdpknvhvy100% (2)

- Option Pricing Models - BinomialDocumento10 páginasOption Pricing Models - BinomialSahinAinda não há avaliações

- Accounting NSC P1 MG Sept 2022 Eng GautengDocumento13 páginasAccounting NSC P1 MG Sept 2022 Eng GautengSweetness MakaLuthando LeocardiaAinda não há avaliações

- Chapter 2Documento58 páginasChapter 2Aminul Islam AmuAinda não há avaliações

- Sample Data - Canada Set 1 Form Field Name API NameDocumento12 páginasSample Data - Canada Set 1 Form Field Name API NameJuan David GarzonAinda não há avaliações

- Strategic Management 1Documento112 páginasStrategic Management 1Aashish Mehra0% (1)

- Car firms merger talks benefits and challengesDocumento3 páginasCar firms merger talks benefits and challengessamgosh100% (1)

- Ibm - WK - Co-Om - IbmDocumento57 páginasIbm - WK - Co-Om - IbmAnonymous 0xdva5uN2Ainda não há avaliações