Você também pode gostar

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Travel and Expense PolicyDocumento6 páginasTravel and Expense PolicyLee Cogburn100% (1)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- FL0322696960Documento1 páginaFL0322696960AshwaniAinda não há avaliações

- Abw Invoice 19672430Documento1 páginaAbw Invoice 19672430M TalhaAinda não há avaliações

- CIR v. PAL (Ortega)Documento5 páginasCIR v. PAL (Ortega)Peter Joshua OrtegaAinda não há avaliações

- Guest AccountingDocumento8 páginasGuest Accountingjhen01gongonAinda não há avaliações

- Hotel Confirmation TemplateDocumento2 páginasHotel Confirmation TemplateantonytechnoAinda não há avaliações

- Original For Recipient Duplicate For Transporter Triplicate For SupplierDocumento1 páginaOriginal For Recipient Duplicate For Transporter Triplicate For SupplierKarthik TAinda não há avaliações

- GL Code CSI Mania-4Documento10 páginasGL Code CSI Mania-4Abhishek ParasharAinda não há avaliações

- Bill - 6095Documento2 páginasBill - 6095vidyamotors27Ainda não há avaliações

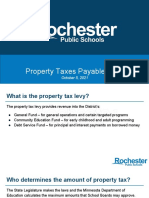

- Property Tax Levy 2022Documento10 páginasProperty Tax Levy 2022inforumdocsAinda não há avaliações

- Psa Membership Application Form April 2022Documento1 páginaPsa Membership Application Form April 2022geraldlekotaAinda não há avaliações

- DocumentDocumento2 páginasDocumentNorelkis Thais Perez ArangurenAinda não há avaliações

- Pay Slip Components: Covance Pty LimitedDocumento1 páginaPay Slip Components: Covance Pty LimitedAndrés PatiñoAinda não há avaliações

- Corporate Installment Guide T7b-Corp-18eDocumento30 páginasCorporate Installment Guide T7b-Corp-18eMartin McTaggartAinda não há avaliações

- How To Find If A Wage Type Is Taxable or Not - SAP Q&ADocumento4 páginasHow To Find If A Wage Type Is Taxable or Not - SAP Q&AMurali MohanAinda não há avaliações

- Money Transfer API Service ProposalDocumento6 páginasMoney Transfer API Service ProposalAnagh RajAinda não há avaliações

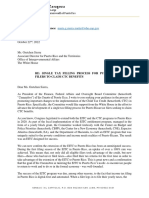

- 10.20.22 Letter Gretchen Sierra CTC PRDocumento2 páginas10.20.22 Letter Gretchen Sierra CTC PRMetro Puerto RicoAinda não há avaliações

- Lesson One - Banking Partners PDFDocumento2 páginasLesson One - Banking Partners PDFJOHN MENDOZA GALLEGOSAinda não há avaliações

- Name: in This Lesson, You Will Learn To:: InstructionsDocumento4 páginasName: in This Lesson, You Will Learn To:: InstructionsEthan JohnsonAinda não há avaliações

- EFT Payments and Receipts Ex. 21 - 30Documento14 páginasEFT Payments and Receipts Ex. 21 - 30Derick du ToitAinda não há avaliações

- Suture Al Wali 13-1Documento1 páginaSuture Al Wali 13-1Arsal Ghulam MustafaAinda não há avaliações

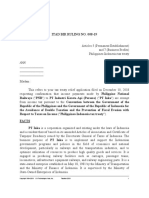

- ITAD BIR Ruling 008-19 PE - Rep OfficeDocumento14 páginasITAD BIR Ruling 008-19 PE - Rep OfficeKathyrn Ang-ZarateAinda não há avaliações

- Oct 2023Documento5 páginasOct 2023AnkitAinda não há avaliações

- Agreeya Solutions (India) Private Limited: Earnings DeductionsDocumento1 páginaAgreeya Solutions (India) Private Limited: Earnings DeductionsGirnar studioAinda não há avaliações

- Research On Taxation PracticeDocumento51 páginasResearch On Taxation Practicehinsene begnaAinda não há avaliações

- PMHPANYD23020003Documento2 páginasPMHPANYD23020003ashishAinda não há avaliações

- Sedo GMBH Im Mediapark 6 50670 Cologne GermanyDocumento1 páginaSedo GMBH Im Mediapark 6 50670 Cologne Germanypaul deaunaAinda não há avaliações

- Final Income Tax Rates: Short-Term Interest or Yield Long-Term Interest or YieldDocumento4 páginasFinal Income Tax Rates: Short-Term Interest or Yield Long-Term Interest or YieldJulie Mae Caling MalitAinda não há avaliações

- UDAYA - One Year Classroom ProgramDocumento3 páginasUDAYA - One Year Classroom ProgramAmish RaiAinda não há avaliações

- Annotated BibliographyDocumento4 páginasAnnotated BibliographyJBizz0Ainda não há avaliações