Escolar Documentos

Profissional Documentos

Cultura Documentos

Business Ethics and Social Responsibility

Enviado por

titoDireitos autorais

Formatos disponíveis

Compartilhar este documento

Compartilhar ou incorporar documento

Você considera este documento útil?

Este conteúdo é inapropriado?

Denunciar este documentoDireitos autorais:

Formatos disponíveis

Business Ethics and Social Responsibility

Enviado por

titoDireitos autorais:

Formatos disponíveis

NIM

NIGERIAN INSTITUTE

OF MANAGEMENT

(CHARTERED)

NIGERIAN INSTITUTE OF MANAGEMENT

(CHARTERED)

BUSINESS ETHICS AND

SOCIAL RESPONSIBILITY

(SMPE 203)

NIM VISION: To be The Source and Symbol of Management Excellence

NIGERIAN INSTITUTE OF MANAGEMENT

(CHARTERED)

STUDY PACK

NIM / NYSC PROGRAMME

BUSINESS ETHICS

AND SOCIAL RESPONSIBILITY

(SMPE 203)

STAGE II

For more information, please contact:

Management House

Plot 22, Idowu Taylor Street

Victoria Island Lagos

P.O. Box 2557

Lagos

Tel. 01 2701017, 2705928

Website: www.managmentnigeria.org

E-mail: mgtedu@managementnigeria.org

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

3

FOREWORD

This study pack covers all the topics and all the basic materials necessary for adequate grasp of the

subject for the Proficiency Certificate in Management Examination of Nigerian Institute of

Management (Chartered).

While expecting candidates, to read as widely as possible on their courses, the Institute's role in

preparing this study pack, is to treat in one publication all the topics covered by the syllabus for this

particular course.

This will enhance focused study on the part of candidate. This pack is written by an expert on the

subject. The writing is reader-friendly while the issues discussed are current with the general

treatment of topics having a contemporary feel.

The topics are treated in a way not only to provide general and theoretical knowledge but to

enhance practice.

Reviewed questions are provided at the end of each pack.

We wish to express our utmost appreciation to our faculty of experts for their invaluable

development and writing of these study pack series.

We also appreciate the support provided by the Directorate of Capacity Building.

MANAGEMENT

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

4

TABLE OF CONTENTS

Page

FOREWORD 4

TABLE OF CONTENTS 5

Lecture 1 The Concept of Ethics 6

Lecture 2 Tools of Ethics (Values, Rights and Duties) 10

Lecture 3 Moral Rules in Human Relations and Common Morality 13

Lecture 4 Situational Factors in Ethical Behaviours in Business 17

Lecture 5 NIM Code of Conduct 20

Lecture 6 The Concept and Impact of Social Responsibility 22

Lecture 7 Social Audit 25

Lecture 8 Issues in Transparency 28

Lecture 9 Corruption and Integrity of Managers including the ICPC Act.39 30

Appendix 39

References 42

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

5

LECTURE 1

THE CONCEPT OF ETHICS

1.10 Learning Objectives

At the end of this lecture, students should be able to:

i. Describe ethics and its importance in ensuring business success.

ii. Explain some ethical rules.

iii. Identify ethical and unethical behaviours in business

1.20 Introduction

Business is a sequence of economic activities, involving the use and exchange of resources for

money. Firms and corporations operate in a social and natural environment and should be

accountable to the society in which they operate and grow. Irrespective of the demands and

pressures upon it, business is built to be ethical, for at least two reasons. Firstly, whatever business

does affects its stakeholders. Secondly, every business action has ethical as well as unethical paths.

We should endeavour to always follow the ethical way-the better way!

1.21 The Concept of Ethics

A. What Are Ethics? They are:

Moral laws and standards which provide necessary boundaries that will ensure fair practices

and opportunities for individuals as they interact with one another in different organizations

The moral rules and standards which serve as guidelines for a group of people with common

goals

The paths business firms ought to take to ensure that the economy and the larger society get

the greatest benefit from their existence

Moral rules and guidelines which enable business organizations to enrich the capacity of the

system in which they are functioning

B. Business Ethics:

Ethics as practised by business organisations is called business ethics.

Specifically, they are moral rules and standards which guide business actions, decisions and

judgements.

Most business actions and choices, decisions and judgements have ethical aspects since they

specifically involve values that help or harm people and indicate character.

Sternberg (2000) argued that, hiring and firing, choosing suppliers, setting prices, establishing

objectives, allocating resources, determining dividends, disciplining workers, planning schedules,

awarding contracts, all involve ethical choices'. Even the most trivial decisions that appear to be

made on purely technical or economic criteria have ethical aspects.

C. Importance of business ethics.

To show stakeholders the necessary ethical boundaries that will ensure that businesses are

carried out with utmost decency

To establish good corporate and personal image and reputation

To build good interpersonal relationships as people would know when and where to draw

the line in relationships

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

6

To be able to deal with grey areas that may come up in the business

To help entrepreneurs and employees know how to conduct themselves

They form the basis of various business decisions, which is why companies have their own

handbooks which detail how every employee is expected to act and behave.

1.22. Issues in Business Ethics

Generally, business ethics are moral laws that involve a

1. High sense of self awareness and management in:

a. Time Management: Time management deals with the ability to utilize effectively

the period during which an activity begins or ends or the duration to accomplish a

task. Time management is an essential ingredient in business ethics because time is

an asset at the disposal of every manager and employee and if not properly managed

it will make the organization to be irresponsible to all its stakeholders. Time

management tools include day planners, diaries, calendars, to do lists, work

schedules and movement itinerary.

b. Life Goals Programming: This deals with the process whereby a firm sets out all its

activities in line with the objectives of the firm and people in its operational

environment. It also entails ensuring that its activities benefit all stakeholders.

c. Personal Grooming and Consciousness: Personal grooming and consciousness

are issues in ethics which relate to individuals, managers and firms believing in

themselves, setting out patterns for developing themselves and following the normal

growth stages. They support setting standards in line with right values in order to

achieve optimum results, without following short cuts.

d. Human Relations: This relates to the guiding principles of office etiquette,

behaving politely with customers, protecting privacy of employees, avoiding

discriminations and kickbacks etc.

e. Striving for Excellence: This is based on the need for businesses to always aspire

to be the best amidst competition. Business firms should build on their strengths,

overcome weaknesses and utilize effective opportunities within their reach. They

should always pursue goals that will improve their image and create goodwill in their

internal and external environments.

f. Self-Discipline: Keeping moral laws requires a high sense of discipline on the part

of the management and employees.

Self discipline is the oil that lubricates the wheel of all moral laws. Without self

discipline, ethical and moral standards would be meaningless and unattainable.

2. A high sense of responsibility and loyalty to:

a. One's own roles: Ethics involves looking inwards and examining oneself with

respect to the level of commitment to our duty and the level of honesty and integrity

one upholds in executing assigned tasks. It is asking the question how do I conduct

my affairs?

b. Superior Officers and Subordinates: As a manager, you have superior officers

to whom you report and subordinates who report to you. The manager should be

faithful in discharging his duties to both parties. He should give timely reports,

feedback and respect to the superior officers to build good interpersonal

relationships. He should also carry the subordinates along with utmost open

mindedness.

c. Company's Customers and Suppliers: Management and employees should be

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

7

fair in all their dealings with customers and suppliers. This is because they are dealing

with human beings who have feelings which shouldn't be exploited or abused. There

is a need be very careful in our choice of spoken or written word. Expressions that

may hurt people or leave negative indelible marks in the minds of customers and

suppliers should not be used. Courtesy and consideration should be shown at all

times. Additionally, when engaging in business transaction, it is always good to reach

a win-win rather than a win-lose conclusion.

d. Acquisition and Use of Other Resources:

Organizations do not exist in a vacuum. They use resources within and outside their

environment in the course of producing their products or delivering their services. A

proper and effective use of resources will impact positively on the people in the

community and on the natural environment. There is a need to look at your

organization and see how its business operations affect the people and the

environment. In doing this, the following questions need to be asked and answered;

Does the appearance of the organization premises make the area habitable or

inhabitable?

Does our use of roads have a dilapidating effect on them? If yes, How?

Does our organisation play a role at ensuring that the roads are maintained at regular

intervals?

How much waste material is generated by our business? What are we doing to

reduce it?

Does our company cause atmospheric pollution? If yes, what plans are in place to

control or eliminate it?

Have you applied the principles of environmentally sustainable economics to your

organizational plans?

Are there local projects to embark on, possibly with the cooperation of others in the

community?

e. One's own family, community and nation:

Ethics equally takes into consideration the physiological and social needs of all the

stakeholders in the business organization. As a chief executive or manager of a

business organization, whatever actions you take will directly or indirectly impact on

your family, community and the nation at large.

3. A high sense of probity

a. In dealing with confidential matters. As an employee, you owe the

organization a duty of trust and loyalty in handling confidential matters and making

sure they do not leak to unauthorised persons.

b. In resource utilization.

In reporting the financial condition of the organization, information on the prospects

and difficulties of the organization should also be given. We should be prudent and

thorough in handling all transactions.

Fraud and all forms of financial mismanagement should be avoided.

c. At all occasions and situations those in charge of management should apply

probity with respect to changes and challenges they may encounter in exercising

their authority.

d. and accountability for:

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

8

authority assumed and roles played

resource utilization

life spent

1.3. TUTORIAL QUESTIONS.

i. Observe some managers in action for a day. How ethical are they? Why?

ii. Discuss why managers should behave ethically to subordinates. List 4 such ethical

behaviours.

iii. Do you think Nigeria is generally an ethically barren country? Give your answer

considering the ethical rules in this lecture.

iv. Which Nigerian and foreign companies were liquidated because they breached ethical

rules? Give details of the situation that led to their fall.

1.4. REVISION QUESTIONS

i. What business ethics principles are relevant in the 21st century Nigeria?

ii. Various ethical decisions are based on ethical standards. Discuss.

iii Describe the proper attitude and behaviour of managers to customers.

iv. Why is life grooming an important ethical concept?

v. List 3 definitions of ethics. Which of them do you like best? Why?

vi. How can employees learn self discipline and good human relations?

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

9

LECTURE 2

TOOLS OF ETHICS

2.1 Learning Objectives

At the end of the lecture, students should be able to:

i. Identify at least four tools of ethics

ii. Explain the application of these tools to business

iii. Explain the importance of values in organisations

iv. Differentiate between values and objectives

2.21 Introduction

Tools of ethics are the components or measures adopted to ensure ethical conduct in business. They

include:

1. Values

2. Right

3. Loyalty

4. Fairness

5. Principled behaviour

6. Confidentiality

2.22. Values

A. Definitions of values:

The virtues promoted by an organization.

The primary points of reference which guide the conduct of business in doing the right thing

in order to achieve business goals

Beliefs about what is right and wrong and what is important in life

Values spell out in clear terms what a group of people uphold (whether good or bad)

They are the principles, way of life and beliefs which a group of people abide by in order to

achieve an objective or set of objectives.

A set of principles or standards of behaviour acceptable among all the stakeholders in

business irrespective of the differences in ethnic background, culture, and religion.

B. Examples of values:

An organization's core values e.g. we are committed to providing superior service to our

customers'

Educational institutions are promoted on the basis of the values they espouse. Various

professional bodies espouse different values in line with their practice. For instance, the

medical profession has a set of primary values such as:

Non malfeasance (Do no harm)

Beneficence (Do good)

Autonomy (Respect the dignity of human life)

Justice (seek the common good)

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

10

The 1994 code of values for International Christian, Muslim and Jewish businesses include

Justice (fairness),Mutual respect (love and consideration) Stewardship (trusteeship)

Honesty (truthfulness).

C. Values and Objectives

Values and objectives are closely knit together. They are two sides of the same coin. This is

because

All objectives are value laden.

Values therefore are entrenched in objectives.

As we pursue the objectives of profit maximization, cost minimization and business continuity, it is

equally important to emphasise the values of creativity, personal satisfaction, employee- welfare

and development.

D. Why do we Need Values?

To:

a. help an organization to identify and focus on areas within it that need attention

b. create unity, competitiveness and value maximisation for shareholders

c. help organisations do the right things like obeying laws, providing a high quality work

environment life for people and satisfying customers

d. positively change peoples' attitude and aspirations

e. give positive encouragement to people rather than negative prohibition.

2.23 Right

A. Definitions:

Something that is morally good or correct

To have a moral claim

to get or have something/someone behave in a particular way

The authority to perform or carry out an act

The authority/ claim that people have towards the responsibility and accountability of

organizations to them

2.24. Duties: Duties are the tasks assigned to people. Duties spell out responsibilities of

individuals in the organization. Many such duties form a job.

2.25 Loyalty: This implies an allegiance/commitment of employees to a set of

objectives/management/policies of the organisation.

2.26 Fairness: It is the avoidance of discrimination in dealing with people of diverse

backgrounds, endeavouring to treat all human beings equally and giving each person equal

opportunities notwithstanding cultural, socio-economic and educational backgrounds.

2.27 Principled Behaviour: This is the demonstration of a consistent behaviour in similar

situations that makes one's behaviour predictable. It ensures that the same decision is made

in similar situations.

2.28 Confidentiality: this involves being discreet in dealing with the organisation's publics and

a refusal to divulge official information even in the face of financial inducement or threats.

For example, a refusal of a secretary to divulge names of those to be retrenched before they

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

11

are officially published or to give unauthorised persons the personal information of

managers shows a high sense of confidentiality.

2.3 Tutorial questions.

Visit any organisation of your choice to record the tools of ethics applied in its day to

day operation. Which of the tools is not properly utilised? Why?

Discuss how ethics can help to achieve corporate goals.

With relevant examples, differentiate between i. loyalty and principled behaviour ii.

Duties and values.

2.4 REVISION QUESTIONS

i. Differentiate between values and ethics

ii. List and explain four tools of ethics

iii. Why do we need confidentiality in organizations?

iv. Explain the importance of fairness in conducting business in Nigeria

v. How are values and objectives related?

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

12

LECTURE 3

MORAL RULES IN HUMAN RELATIONS AND COMMON MORALITY

3.1 Learning Objectives

At the end of the lecture the students should be able to:

i. Identify the need for good relationship among employees in organizations

ii. Explain the need for moral rules in organizations

iii. Apply the principles of human relations in enforcing moral rules in organizations

iv. Identify and describe some theories of human relations

v. Assess the effectiveness of human relations in organizations.

3.20 Introduction

The manager often experiences his most uncomfortable moments when he has to deal with

differences among people.

The best possible way to deal with these differences is to build good human relations with the

employees. When good human relationships are entrenched, conflicts hardly arise, and if they do,

they do not get out of hand and are easily resolved

3.21 What are human relations?

A body of knowledge through which workers and management get things done

cooperatively.

According to Halloran (1978) human relations involve all the interactions that occur among

people, whether they are conflicts or cooperative behaviours.

The study of how people can work effectively in groups in order to satisfy both

organizational goals and personal needs.

Stan (1978) observed that, human relations are concerned with the 'why' of the people and

their groups.

Human relations are also concerned with what can be done to anticipate, prevent, or

resolve conflicts among organization members''.

They are all about building good interpersonal relations between management and

employees and among employees of an organization.

3.22 Philosophy of Human Relations

Human relations ensure that people with whom we work are treated importantly, responsibly and

sympathetically whenever they come up with any complaints. John Adair believed that if groups of

people are to have cohesion, morale and motivation, they must seek each other's cooperation.

Douglas McGregor (1960) listed the following as the basis of human relations:

i. The loyalty and cooperation of individual in an organization must be earned, won and

supported.

ii. The individual employee with his status, rights, prospects for advancement and economic

well-being, is linked with the success of the enterprise to which he is employed

iii. The basic relationship of the individual should not be jeopardized by government, union

and management activities.

iv. Personnel policies and practices must be designed and implemented in such a manner as to

promote and safeguard the rights and well being of the workers.

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

13

v. Organizations must strive to provide for the economic and social security of their employees

vi. The society must be free and ready to safeguard its own rights and privileges.

Building or creating good interpersonal relationship should not be limited to management and

employees, but spread through all the persons the organization carries out transactions with and

those who have interest in the organization such as the customers, suppliers, competitors and the

general public.

3.23 Human Relations Effectiveness

A. One way to measure Human relations effectiveness is our thoughtfulness in interpersonal

communication.

As a professional, bear in mind that those you are dealing with are human beings with

feelings. Therefore, utmost care should be taken in our choice and use of words in order to

avoid ethical scandals in which people frequently feel attacked, insulted, and demeaned.

Even when we are upset or displeased, we should be very careful about our choice and use

of words.

B. Other issues that border on human relations effectiveness are motivation, leadership and

empathy. Kossen, (1978) gave the following rules on the use of words in promoting human

relations:

1. The least important word is I

2. the most important word is we

3. The two most important words are thank you

4. The three most important words are if you please

5. The four most important words are what is your opinion

6. The five most important words are you did a good job

7. The six most important words are I admit I made a mistake

3.24 Steps in Re-Establishing Long-Term Relationships between Organization and

Employees:

Step One Re-establish code and policies for sustainability

Step Two Re-establish justice

Step Three Re-establish fairness

Step Four Re-establish practices of honesty

3.25 Common Morality

1. Dignity

Apologize for delay

Extend personal restitution to the victim

2. Honesty

Stop the spiral of lies and denials

Implement full and immediate disclosure of relevant information

Facilitate access to information and persons.

Respond openly and promptly to all queries

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

14

3. Fairness

Ensure compensation is commensurate with any loss

Accelerate reconciliation as much as possible and as quickly as possible

Encode and practice lessons in fairness to benefit future transactions

4. Auditing

Establish formal framework for monitoring ethical orientation

Report ethical progress alongside financial progress

Report progress of plans to employees, industry association, and the community.

5 Updating

Begin planning for ethical mandate beyond resolution of the present issue

Report ethical progress and plans to the community, employees and industry

association.

3.26 Some examples of ethical rules.

"One should not tell lies,"

"One should keep all expressed and implied promises,"

"One should respect bosses, elders and parents",

"One should help people in distress" etc

3.27 A commentary on lying and ethics.

Many ethical rules are controversial. For example, while some people would agree that in most

situations, one should not tell lies; there may be exceptions to the rule.

Assume for instance that a very angry man brandishing a cutlass asked you whether your sister was

in the house. You would reasonably fear for the life of your sister and tell a lie to protect her. Does

the rule that you should not lie cover this situation?

Thus for example, in the case of the angry man with the cutlass, one could reason that one should

tell no lie, because (i). Telling lies is a way of harming the people one deceives, and (ii) it tends to

undermine mutual trust among people. If these were the complete justification of the rule against

telling lies (which is not the case), it would follow that the rule did not apply in this case. By telling

the madman that your sister was not at home, you would not be harming him in anyway. On the

contrary, you would be preventing him from doing something that, once he recovers his sanity, he

would greatly regret. In addition you will not undermine trust among people by lying to him.

3.28 Principles of business ethics.

According to Elegido (1996) the following are independent and ultimate principles of business

ethics.

i. Principle of Solidarity: We must be concerned with promoting the wellbeing of all human

beings, not only our own. In so far as we fail to do so, we undermine our own fulfilment.

ii Principle of Rationality: One should always strive to act intelligently.

iii. Principle of Fairness or Impartiality: We should apply the same standards in judging our own

actions, those of people who are dear to us and those of strangers

iv. Principle of Efficiency: In trying to promote human fulfilment, good intentions are not

enough: one must endeavour to use effective and efficient means.

v Principle of Refraining from willingly harming other human being: One should never

choose to harm another human being directly or indirectly.

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

15

vi. Principle of Role Responsibility: One does not have responsibility for all the aspects of the

well-being of all human beings. One's special circumstance, capacities, roles and

commitments give one a priority

responsibility for only certain aspects of the well being of certain people.

3.3 Tutorial questions.

i. Assess the practical benefits of McGregor's view of human relations to the Nigerian manager.

ii. According to Koseen (1978) what key words should all good human relations practitioners

learn and apply?

iii. What steps would you take to re-establish good relationship with others?

iv. Why should we admit and apologise when we are wrong?

v. Should we apologise to customers for situations we didn't cause personally?

3.4 REVISION QUESTIONS

i. What is the study of Human Relations?

ii. Good human relations in organizations assist in ensuring that rules are obeyed in

organizations. To what extent is this true?

iii. Human relationship is all about ensuring that people with whom we work are

treated well. Explain.

I Identify four elements of common morality

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

16

LECTURE 4

SITUATIONAL FACTORS IN ETHICAL BUSINESS BEHAVIOURS

4.1 Learning Objectives

At the end of this lecture, students should be able to:

i. Identify situational factors in unethical behaviour.

ii. Explain the meaning of ethical audit

iii Identify ways in conducting ethical audit in organization

iv identify tempting situations in organisations.

4.20 Introduction.

Ethical issues vary from person to person, from time to time and from organization to organization.

The method of tackling them should also vary.

The fact that so many notable corporate bodies and individuals in Nigeria are repeat offenders is

due to the fact that ethics is viewed narrowly as a one time problem rather than in the context of the

national psyche. Many organizations hire sound individuals to manage their affairs without giving

them the required training and exposure. Managers need to understand the dynamics that

contribute to an error of ethical judgement. One of them is the situational factor in ethical

behaviour.

4.21 Situational factors.

Situation factors that need to be considered with respect to ethical behaviour in business are stated

below:

1. An understanding of the scope and scale of temptations to be unethical. In doing this, the

following questions need to be answered:

a. What moral or legal issues have raised ethical concerns in the past?

b. How can these issues change and test the behaviour of business organizations and

individual employees?

c. What are the new pressure points created by changes in technology or global

competition?

d. How well equipped are organisations for dealing constructively with new

temptations created by the new technology?

2. The moral strength and weaknesses of the business organization for withstanding and

overcoming the temptations. These entail an audit of past ethical performance and an

evaluation of the ethical concerns of the employees.

4.23 Ethical Auditing

Ethical audit is a powerful technique used in recent years to give detailed reports to ethical

stakeholders or the general public on the ethical performance of an organization over a period of

time. Ethical audit is usually carried out by independent external auditors. According to Murray

(1997) the following points are considered in carrying out ethical audit.

1. Clarity of purpose: The reason for embarking on the audit should be spelt out e.g. Do you

want to audit in order to obtain information which will help you steer the ethical

development of the organization? Or to persuade critics that, you are not as bad as they say?

Or to follow a current fashion in management (sadly not uncommon with new

methodology)? Or to meet demands from a customer or client?

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

17

2. Type of topic: What kind of audit do you want to carry out?

Varieties of Ethical Audit

Audit of the existence of policies and procedures.

Audit of compliance with policies and procedures.

Audit of actual performance (external impact)

Audit of staff perceptions

Audit of staff aspirations and concerns

Audit of customer and other stakeholder perceptions

Audit of customer and other stakeholders aspirations/concerns

Audit of specific issues or problem areas

Audit of legislative/regulatory compliance

Audit comparison with reference scales, peers or benchmarks

You have to choose. How will you determine what topics to include or whether to start with a

small subset? Will you keep to auditing compliance with the rule book or attitudes towards

corporate environmental impact, or understanding of health hazards? Or do you w a n t t o

explore in depth the values of your people relative to all major categories of stakeholders?

3. Context: In what managerial context is the audit being carried out? Is the organization

accustomed to audits for other purposes? Is there commitment from the top to act on the

findings? What pressures are there and will there be, to do so?

4. Process: What process will you use? Will it be paper based questionnaires? If so, do you

have access to expert questionnaire design skills? Will it include technical assessments, and

do you have access to the skills and equipment needed? Will it include face-to-face

interviews? Do you have experienced interviewers for sensitive topics and areas?

5. People: Be careful not to use only specialists in ethics. You need people who can

communicate intelligently with the people they are working with.

6. Analysis and reporting: Do you have the capacity to process the data yourselves? Or will

you use an outside agency? How will the various levels of report be produced, approved and

published?

7. Follow-Up: What follow-up do you intend? Clearly, you can't know exactly what will be

required, but do you have at least outline plans for discussion and developing action

programmes? To conduct an audit raises expectations. If you have accepted people's

cooperation in the conduct of the audit you will be betraying a trust if you subsequently do

nothing about the findings.

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

18

4.3 TUTORIAL QUESTIONS.

What situational factors should reduce the punishment for corruption in organisations?

Are corrupt government officials in Nigeria and the United Kingdom equally guilty? Explain

your answer.

Study the ethical audit report of any organisation.. How did it explain and reduce unethical

behaviours in the organisation?

4.4 REVISION QUESTIONS

i. What constitutes unethical conduct in the oil business?

ii. Explain the salient features of an ethical audit.

iii. How can ethical auditing be conducted in an organization?

Iv What methods can be used to ensure the accuracy of ethical audits?

iv. Ethical issues vary from time to time and from one organization to another. Discuss

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

19

LECTURE 5

NIM CODE OF CONDUCT

5.1 Learning Objectives

At the end of this lecture, students should be able to:

i. State the meaning of code of conduct

ii. Recite from memory, the NIM code of conduct

iii Mention some benefits of a Code of Conduct

iv Explain the criteria of a good code of conduct

v. Design a code of conduct for their organisation.

5.21 Introduction

A code of conduct is

A list of ethical principles and moral rules for members of an organisation

The set of dos and don'ts of workers\professionals

A set of guiding principles which puts a manager's action in a moral perspective.

A brake, a control that prevents employees from unethical behaviour.

5.22 IMPORTANCE OF A CODE OF CONDUCT.

It communicates corporate purposes explicitly.

It expressly identifies corporate policy about controversial matters.

It clarifies which stakeholder expectations are legitimate.

It eliminates ignorance as an excuse for unethical behaviour.

It is an effective tool for sharpening business accountability and improving corporate

governance.

It attracts customers and gives them the confidence to patronize the organisation

It enhances corporate goal attainment and employee job satisfaction

5.23 CRITERIA/ CONDITIONS OF A GOOD CODE OF CONDUCT.

It must be properly structured and outlined.

It may not reflect the prevailing values or culture of the organization. When the existing

culture is less than perfect, enshrining it in a code merely reinforces bad practice. For a code

of conduct to improve organizational conduct; what it prescribes must be better than the

existing norm.

It is necessary to consult shareholders, especially employees to determine what situations

are genuinely problematic and the stringency of the standards.

Employees should be involved in the code-making process to improve understanding of

and compliance with the code.

There must be active support of business directors and senior executives.

5.24 The Nigerian Institute of Management Code of Conduct is as follows:

1. That I, as a professional manager will put service above self and will ever seek to find and

employ more efficient and more economical ways of getting things done.

2. That I, as a professional manager, accept the most scrupulous and transparently honest and

ethical process of thought for all decisions in my daily work and be myself free of any

fraudulent and/or corrupt practices and within my scope of authority treat all persons as

being equal and refuse to give special favours or privileges to anyone.

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

20

5.25 Summary of a general code of conduct for managers.

A manager should:

Create a clear, simple, reality-based customer-focused vision, and be able to communicate it

straight forwardly to all constituencies.

Understand accountability and commitment and be decisive. He should set and meet

aggressive targets with unyielding integrity.

Love excellence, hate bureaucratic red tape and all its deficiencies.

Have the self-confidence to empower others, love team work and be committed to efficient

work-output.

Stimulate and relish change as an opportunity, not a threat. He should not be frightened and

paralyzed by it.

Have enormous energy, the ability to energise and invigorate others and understand that

speed is a competitive advantage.

5.3 TUTORIAL QUESTIONS

i. What gap did you notice in the NIM Code of Conduct? Suggest appropriate provisions to

make it more comprehensive.

ii Assess the effectiveness of a code of conduct in corruption prevention.

iii. Design a code of conduct for corps members on primary assignment. Suggest strategies for

enforcing it.

iv Recite the NIM Code of Conduct. Compare it with the code of conduct of another

professional body. Which of them will encourage better conduct and behaviour? Why?

5.4 REVISION QUESTIONS

i. What is a code of conduct? Why do you think all professional bodies should have a

code of conduct for members?

ii. List 5 features of a good code of conduct.

Iii Why do you think managers should consult with employees when designing a code of

conduct?

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

21

LECTURE 6

THE CONCEPT AND IMPACT OF SOCIAL RESPONSIBILITY

6.1 Learning Objectives

At the end of this lecture, students should be able to:

i. Define the concept of Corporate Social Responsibility.

ii. Highlight the ways organizations can be socially responsible

iii. State the impact of corporate social responsibility on different stakeholders.

iv. Explain the case some people have against corporate social responsibility.

6.20 Definitions of Corporate Social Responsibility.

A process through which business organizations deploy their resources to uplift the general

welfare of the residents in the community in which they carry out their activities.

It is the private sector's way of integrating the economic, social and environmental

imperatives of their activities.

It is about an organization caring for the community in which it operates.

An intelligent management of the expectations and needs of the community

6.21 Socially Responsibility strategies

Initiating/supporting worthy community initiatives like building and equipping schools,

universities, hospitals, museums and sports centres

Helping to protect the environment by ensuring all manner of pollution is reduced.

Creation of employment

Making provisions for employment of physically challenged persons.

Fairness, equity, justice in all its employment and other policies.

Working towards the common good of all the residents of the community

Obeying relevant rules and regulations e.g. paying taxes.

6.22 Impact of Corporate Social Responsibility on Business

i. Increased profitability ratio

ii. Promotion of organizational goodwill

iii. Increased corporate patronage

iv. The company's product can become a household name

v. Enhanced business sustainability

vi. Improved competitiveness in every area of business.

Vii Corporate peace and tranquillity.

6.23 Impact of Corporate Social Responsibility on Society

i. Increased physical and mental development e.g. more asphalt- roads, pipe borne water,

education etc.

ii. Builds corporate goodwill in the society

iii. Reduces crime, promotes sports, arts and culture, cares for the disadvantaged and the

forgotten etc.

iv. Helps in discovering new talents in music etc e.g. the Maltina Dance Show, the Peak Talent

Hunt

vii. Increases maintenance culture and life span of a lot of infrastructural facilities such as roads,

drainages hospitals etc.

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

22

viii. Helps to increase social welfare

ix. Increases community health and life expectancy ratio

6.24 Professor Friedman's Position

Prof. Friedman, the famous monetary economist argued in favour of the thesis that an

organization has only one responsibility: maximizing profits for its shareholders while operating

within the limits set by the law. He set out his main arguments for this position in a famous and

often quoted article entitled: The Social Responsibility of Business is to Increase its Profits.

In Friedman's view, it is certainly a responsibility of organizations to respect all the laws which

protect the public interest. But going beyond this would amount to having socially responsible

executives functioning as redistributors who would take other people's money and spend it on what

these executives themselves defined as the general social interest, as if they were some sort of self

appointed tax collectors.

It is Friedman's contention that it will be better for everybody if business executives concentrated on

maximizing profit, for in this way, they will more effectively be led by an invisible hand to promote

the good of the society.

In fairness to Friedman, it should be emphasized that he was in no way against charity and giving to

the needy. He was against giving other people's money to the needy. His view was that if an

organization spent money supporting worthy causes instead of redistributing that money among its

shareholders, it would prevent the latter from supporting the causes they prefer.

6.25 Some limitations of Social Responsibility (CSR)

Indiscriminate use of corporate resources in CSR may reduce investment funds and

shareholders' gain.

Government may offload its responsibilities on the private sector. CRS should complement

and not replace government.

Corruption in the public service will thrive if public duties are performed by private

organisations.

The limited ability of the private sector in social welfare.

CSR can also be diversionary; managers may lose focus from fundamental business goals.

6.3 TUTORIAL QUESTIONS.

1. Evaluate the CSR of any organisation you are familiar with. What activities did they

undertake? How were they selected?

2. Do you believe there can be too much CSR? What does it mean?

3. Do you think it is fair for corporate Nigeria to provide social amenities in their host

communities after paying taxes?

4. Imagine a Nigeria without CSR. How will things look like?

5. Learn from your community elders about on-going and completed CSR projects in your

area.

How were they selected?

Are they what the community required?

How have the sponsors benefitted from each project?

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

23

6.4 REVISION QUESTIONS

i. An organization's corporate social responsibility is important for its survival and

success. Discuss

ii. What is corporate social responsibility?

iii. Why should organizations embrace corporate social responsibility?

i. Why do some firms reject social responsibility?

ii. Suggest 10ways the NIM can show greater social responsibility in Nigeria.

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

24

LECTURE 7

SOCIAL AUDIT

7.1 Learning Objectives

At the end of this lecture, students should be able to:

i. Define the term social audit

ii. State the objectives of social audit

iii. Identify the challenges of social audit and how to resolve them.

iv. Describe the methodology of social audit

7.21 Introduction

Social audit as a term was first used in the 1950s. Social audit is similar to financial audit in many

ways except that it is about everything else that an organization does apart from money.

In our own case we are dealing with auditing a social 'system' which survives in the long term only

through being alive to feedback from both the internal (sub-system) and external (super-system)

environments.

7.22 A. Definitional Issues

Below are some definitions of social audit.

According to Bateman (2005), Social audit is a process which enables organizations and

agencies to assess and demonstrate their social, community and environmental benefits a n d

limitations. It is a way to measure the extent to which an organization lives up to the

shared values and objectives it has committed itself to promote.

It is the process whereby an organization accounts for its social performance, reports on

and improves that performance.

It assesses the social impact and ethical behaviour of an organization in relation to its aims

and those of its stakeholders.

Social audit is an organizational strategy of planning, managing and measuring non-

financial activities and monitoring both the internal and external consequences of the

organization's social and commercial operations.

A social audit is a way of measuring, understanding, reporting and ultimately improving an

organization's social and ethical performance.

It is a technique used to understand, measure, verify, report and improve on the social

performance of the organization.

Social auditing is a multi-stakeholder-driven, participatory evaluation process that tracks a

number of different impacts and outcomes. It is a multi-stakeholder process because it

begins by identifying the organization's stakeholder groups those involved in, or affected

by the organization such as service recipients, suppliers, volunteers, employees, funders and

the community (Rittenberg and Schweiger, 2005)

B. Advantages of Social Audit:

Trains the community on participatory local planning

Encourages local democracy and accountability.

Encourages community participation

Benefits disadvantaged groups

Promotes collective decision making and sharing responsibilities

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

25

Develops human resources and social capital.

Promotes corporate ethics and values.

7.23 Requisites of Social Audit

Before a social audit can take place, the following have to be in place:

Clear organizational objectives.

Clear action plans

Clear mode of recording and measuring performance.

Involvement of stakeholders

Intermittent but clear time commitment from top management.

Information sharing among different stakeholders.

7.24 Objectives of Social Audit

Assessing the physical and financial gaps between needs and resources available for local

development

Creating awareness among beneficiaries and providers of local, social and productive

services

Increasing the efficiency and the effectiveness of local development programmes

Scrutiny of various policy decisions, keeping in view stakeholder interests and priorities

Estimation of the opportunity cost for stakeholders of not getting timely access to public

service

7.25 Challenges of Social Audit

i. It is difficult to prepare a social audit report which will be simultaneously fair and objective to

the society, the implementers of the programme and its designers.

ii. Not all social welfare programmes are well designed or based on valid assumptions

iii. An absence of a well conceived information system as part and parcel of a social welfare

programme

iv. Individual programmes pose their own specific problems to the social auditor.

7.26 The Way Out

Seek clarifications from the implementing agency about any decision-making activity,

scheme, income and expenditure incurred by the agency.

Clearly consider and scrutinize existing schemes and local activities of the agency

Access registers and documents relating to all development activities undertaken by the

implementing agency or by other government departments

Sell the programme to all stakeholders to ensure their cooperation and participation.

7.27 Social Audit Methodology

Gather background information about the organisational activities

Use social indicators to measure social effectiveness of corporate activities However

excessive reliance on social indicators can lead to a mechanical report

Check compliance with safety and statutory provisions

Prepare a social accounting document

7.28 Conclusion and Recommendations

Social audit is predicated on the principle that it should be carried out as far as possible with

the consent and understanding of all concerned.

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

26

In summary, the following recommendations will make social audit a regular and effective strategy

to promote the culture of transparency and accountability:

Clarity of purpose and goal.

Identification of stakeholders with a focus on their specific roles and duties

Definition of performance indicators

Regular meetings of stakeholders to review and discuss data/information on performance

indicators

Follow-up on social audit meetings

Establishment of a partnership with trusted local people

Findings of the social audit should be shared with all local stakeholders

7.3 TUTORIAL QUESTIONS

i. Why do you think social audit is not popular in Nigeria?

ii. Select an organisation of your choice and answer the following questions:

How many social audits did they conduct in the past 5 years?

What were the findings of their most recent social audit?

How did the audit benefit the organisation and other stake holders?

What problems were encountered in the audit process? How were they solved?

7.4 REVISION QUESTIONS

i. What is a social audit?

ii. List four objectives of social audit?

iii. What are the problems that may be encountered in carrying out social audit in

an organization?

iv. Describe the methodology of social audit

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

27

LECTURE 8

ISSUES IN TRANSPARENCY

8.1 Learning Objectives

At the end of this lecture, students should be able to:

List and discuss salient issues in transparency in Nigeria

Explain Transparency International Standards of Conduct.

8.20 Introduction

Transparency International Standards of Conduct reflect the conviction that large scale corruption

subverts economic and social development. Transparency International is a coalition of

governments, private sector participants and international aid and financing agencies, designed to

counter corruption in international business transactions. Their standards apply to the coalition

partners and take account of past initiatives by such organizations as the International Chamber of

Commerce and the United Nations. The issues discussed here though from Transparency

International (TI) are very relevant to Nigeria, one of its coalition partners.

8.21 THE STANDARDS.

Article I: Respect for Laws and Standards.

All parties to international business transactions should respect and conform to all

relevant laws and regulations and observe their letter and spirit.

Article II: Improper Inducements

1. No party to an international business transaction should request, demand, offer, or take a gift

in any form, or extend any other advantage to or for the benefit of any public official or as he

or she may direct (and whether directly or indirectly) as an inducement for action or inaction

by the official.

2. All parties should take measures reasonably within their power to ensure that no part of any

payment made in connection with an international business transaction is received directly

or indirectly by or for the benefit of a public official with decision making responsibility or

influence or by their relatives or business associates.

3. All parties should take measures reasonably within their power to ensure that subcontracts

and purchase orders relating to international business transactions are not used to channel

payments or other benefits directly or indirectly to or for the personal benefit of public

officials with decision making responsibility or influence, or to their relatives, or business

associates.

Article III: Agents & Consultants

1. All parties should take measures reasonably within their power to ensure that any

commission or remuneration paid to any agent, consultant, intermediary, represents no

more than appropriate compensation for legitimate service; and that no part of any such

payment is passed on by an agent, consultant or others

2. All parties should take appropriate measures to ensure that agents, consultants, and other

intermediaries are not employed to gain any improper influence in connection with

obtaining or retaining any business.

Article IV: Financial Disclosure

All parties should maintain accounting systems in accordance with best international accounting

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

28

practices under which all financial transactions should be properly and fairly recorded in

appropriate books of accounts which should be available for inspection by boards of directors,

auditors and other authorized persons. In this context there should be no off the book or secret

accounts or any documents issued which do not properly and fairly record the transactions to which

they relate.

Article V: Political Contributions

Contributions to political parties or committees or to individual politicians (or to other persons or

entities at their direction), should only be made or solicited in accordance with applicable national

laws, and all requirements for public disclosure of such contributions should be complied with fully

and promptly. Even when permitted, they should not be made in circumstances, where given their

magnitude or timing, they could reasonably be constituted as exercising influence aimed at

securing a special advantage with respect to an international business transaction.

Article VI: Definition

These standards should be construed widely and in accordance with their spirit. In particular, the

expressions of all parties include national government, national and international agencies

involved in international lending and aid-granting activities; corporations and other enterprises

involved in international business transactions of all kinds, agents, marketing consultants and other

consultants, individuals or firms providing service, or goods in connection with international

business transaction.

8.22. SOME IMPORTANT COMMENTS.

We should do more to monitor, resist and reject corruption.

Nigerian businesses need to increase their transparency skills

Professional institutes should do more to regulate the ethical performance of their members.

Givers and takers of bribes and other illegal inducements are equally guilty. The government

says 'don't give, don't receive '.

Unless corruption is stoutly tackled, Nigeria might become a failed state or an economic

pariah nation.

8.3 TUTORIAL QUESTIONS

i. Why are we using TI standards in this lecture and in Nigeria?

ii. Besides the ones mentioned in the lecture, what other transparency issues are relevant in

Nigeria?

iii. Rate the transparency level of any organisation of your choice on the basis of the issues

listed in the lecture.

iv. Which of the transparency issues raised in this lecture do you find most difficult to accept?

Why?

v. Do you think our accounting and auditing practices meet TI standards? Give reasons for

8.4 REVISION QUESTIONS

i Is the bank manager who allowed his wife to bid for a contract in his bank

guilty of any ethical malfeasance?

ii Why is advance-fee fraud an offence in Nigeria and abroad?

iii. Advise business consultants on how to remain ethical and transparent

iv Mention 10 salient issues in transparency in Nigeria.

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

29

LECTURE 9

CORRUPTION, INTEGRITY OF MANAGERS INCLUDING

THE ICPC ACT

9.1 Learning Objectives

At the end of this lecture, students should be able to:

i. Define the concept of corruption

ii. Discuss the elements of corrupt practices

iii. Explain some punitive measures for corruption

iv. State the meaning of Integrity

v. Discuss the need for managers to possess integrity

vi. Discuss Business Integrity with respect to the Nigerian society

vii. Identify various offences and penalties as stated in the ICPC Act 1999

viii. State the causes of corruption in Nigeria

ix. Identify the negative effects of corruption

9.20 What is Corruption?

Gray and Kaufman define corruption as the abuse of public office for private gain. Thus it

refers to the use of position of power to seek personal advantage either by performing an act

or omission of the expected performance or duty.

Corruption could also be seen as various offences by public officials or corporate executives,

such as receiving gifts from suppliers or any other form of gratification before or after

carrying out assigned task and responsibility, sale of office equipment or granting of

contracts to favoured firms and individuals and granting of land or franchise in return for

monetary reward.

Corruption also entails diversion of funds and resources to other personal uses outside the

original purpose for which such funds are allocated.

9.21 SOME FACTS ON CORRUPTION

Corrupt uneconomic practices are referred to as the underground economy and in 1982,

accounted for about 14% of the global Gross Domestic Product.

A Global Financial Integrity (GFI) report revealed that Africa lost $854bn. ( N128.27trn) to

illicit financial outflows during the last 38 years.

The report further showed that illicit capital outflows, including proceeds from bribery, theft,

human trafficking, drugs and tax evasion grew at an average of 11.9 percent between 1970

and 2008.

It also showed that illicit financial outflows from the entire region outpaced official

development assistance going into the region at a ratio of at least 2:1. The hundreds of

billions lost through the process, according to G.F.I., could have been used for poverty

alleviation and economic development.

More recently, corrupt practices bordering on crime have been uncovered in large

corporations like Enron, World Com. and Halliburton.

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

30

In the former Soviet Union, corruption was referred to as 'na levo, meaning 'on the left'

(OLE) economy.

Transparency International, a Berlin Based International non-governmental organization

(NGO), has been measuring corruption as seen by business people, risk analysts and the

general public. The Transparency International Corruption Index (TICI) ranges from one to

ten, with ten reflecting highly corrupt'.

In 2003, Nigeria was rated the second most corrupt country after Bangladesh, while Finland

was the most incorrupt country followed by Singapore, Britain, Hong-Kong, Germany and

United States.

Between 1998 and 2001, TICI, focusing on African countries showed that corruption

tended to be less in Botswana, Namibia and South Africa while it was consistently high in

Nigeria, Uganda, Kenya and Cameroon (Umo J.U. 2007).

9.22 Net Gains from Corruption

Umo (2007) defined net gains from corruption as the difference between the benefits and

direct cost of corruption. If the net gain is positive, corruption will take place. The higher the

net gain, the higher the degree of corruption in any given society. It should be noted that net

gains from corruption may be monetary, non-monetary or psychological. Thus some of the

gains can be quantified but a good number of them cannot.

Nigeria

Uganda

Kenya

Cameroon

Tanzania

Cote dIvoire

Zimbabwe

Senegal

Ghana

Egypt

Mauritius

South Africa

Namibia

Botswana

0

1 2 3 4 5 6 7

Figure 9.1: Net Gains from Corruption

Source: Transparency International, cited by OECD, African Economic

Outlook 2001/2002 Abidjan in Umo 2007. p. 259.

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

31

9.23 Causes of Corruption

1. Inequitable distribution of income

2. Low level of individual income

3. Poor level of education

4. Misguided social values

5 Greed

6 Weak law enforcement

7 Ignorance of the effects of corruption.

9.24 Negative Effects of Corruption

Aina (2007) listed eight ways in which corruption is harmful to societies. They are as follows:

Corruption causes lowering of the quality of the goods and services available to the public

Corruption tends to discourage honest efforts; the rush for easy money makes fools of those

who do honest work,

Corruption tends to discourage economic initiative. The tangle of red tape strangles would-

be entrepreneurs and the economy suffers

The more corruption becomes common, the more people tend to mistrust the motive of

others and resistance to authority becomes inevitable

As corruption becomes prevalent, those in positions of responsibility lose the ability to

implement policies

A generalized climate of corruption encourages officials to misdirect scarce resources

Corruption tends to discourage investment

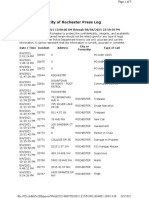

Sm

P

Price Sc

Pm M1

P0 M0

Pe M2 e

Dm

Q

Qc Qe (Stockfish)

Fig. 10.2: Economic incentives for corruption: case of allocation

of import licences for stockfish

Source: J.U. Umo (2007): Economics an Africa Perspective. Pg. 262

9.25 Demand for Corruption

Demand for corruption is a direct function of net gains. As net gains from corruption increase, more

of it will be demanded by individuals in a given society, all things being equal.

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

32

Dc

Quantity

of

Corruption

O Net gains (benefits cost)

Figure 10.2: Demand for Corruption and net gains

Source: J.U. Umo (2007): Economics an Africa Perspective. Pg. 261

9.26 Punitive Measures for Corruption

Since corruption is often a criminal act, it is punishable directly by law. Corruption could also

attract indirect punishment such as heavenly disapproval, social disapproval and disgrace.

A rational corrupt official will, therefore, assess the potential punishment, if and when

apprehended, on the following bases

i. The severity

ii. The probability

Thus, the higher the severity and probability of punishment, the lower the incentive to be corrupt.

For example, financial corruption including tax illegal deals is punishable by death in China. This

does not absolutely eliminate this type of corruption but the probability of its occurrence has

reduced drastically. The implication of the above hypothesis is that corrupt officials are often

tempted to carry out other illegal acts as a means to cover up and eliminate the probability of

punishment or at least minimize its severity. Such illegal acts include attempts to bribe law

enforcement agents.

A weak law enforcement agency in a state promotes corruption because the severity and

probability of punishment are low. There is serious need to fight against unethical business practices

in Nigeria- the giant of Africa.

9.27 Integrity of Managers

A What is integrity?

The will and willingness to do what one knows/ought to do (Solomon 1993)

The will and willingness to stand openly against what one believes to be wrong.

Observing the ethics of an organisation or profession.

According to Solomon

When one willingly joins an organization, agrees to act on its behalf and in its

interests, and agrees with its aims and values, obedience and loyalty are part and

parcel of integrity.

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

33

But when one comes to disagree with those aims and values, integrity requires

disobedience and disloyalty, at least in the form of resignation

B Effects of Poor Integrity

Poor international/corporate image and relations.

An unhealthy economy

Increased unemployment and social vices

Brain drain to developed economies

Misapplied and misappropriated funds

Poor industrial utilisation

Lack of confidence of the citizens/ employees/in leaders and managers.

C. The Way Out

Everyone should be involved in the battle against corruption

The productive sector of the economy should be strengthened

Upholding new standards of truth, civility and accountability

Monitoring and reporting on integrity in business and public entities.

Researching and consulting on integrity-enhancement procedures

Conducting the integrity rating of entities and rewarding integrity heroes.

Training entities on integrity-enhancement via workshops, seminars and other

enlightenment media

Ensuring that a comprehensive Code of Ethics for business and public entities is researched,

developed and adopted a standard.

D. Virtues in Business Integrity.

Managers should display the following virtues to all stake holders:

Fairness. Honesty, Trust, Toughness in competition. Loyalty to stake holders. Care and

compassion, Openness and transparency, justice.

9.28 A SUMMARY OF THE ICPC ACT 1999

A Offences and penalties

1 (1) Any public officer who:

a. Corruptly asks for, receives or obtains any property or benefit of any

kind for himself or for any other person: or

b. Corruptly agrees or attempts to receive or obtain any property or benefit of any kind for

himself or for any other person, on account of;

i. any job already done or omitted to be done, or for any favour or disfavour already

shown to any person by himself in the discharge of his official duties, in relation to

any matter connected with the functions, affairs or business of a government

department, public body or other organization or institution in which he is serving as

a public officer, or

ii. anything to be afterwards done or omitted to be done, or any favour or disfavour

to be afterwards shown to any person, by himself in the discharge of his duties or in

relation to any such matter aforesaid, is guilty of the felony of official

corruption and is liable to imprisonment for seven years.

2. If in any proceedings for an offence under this section, it is proved that any property or

benefit of any kind, or any promised thereof, was received by a public officer, or by some

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

34

other person at the instance of a public officer from a person

a. holding or seeking to obtain a contract, licence, permit, employment or anything

whatsoever from a government department, public body or other organisation or

institution in which that public officer is serving as such;

b. concerned; or likely to be concerned, in any proceeding or business transacted

before or by that public officer or a government department, public body or other

organisation or institution in which that public officer is serving as such.

c. Acting on behalf or related to such a person,

the property, benefit or promise shall, unless the contrary is proved, be

presumed to have been received corruptly on account of such a past or

future act, omission, favour or disfavour as is mentioned in subsection (1)

(a) or (b).

3. In any proceedings for an offence to which subsection (1) (b) is relevant, it shall not be a

defence to show that the accused;

a. Did not subsequently do, make the act, omission; favour or disfavour in question; or

b. never intended to do, make or show the act, omission, favour or disfavour

4. Without prejudice to section (3), where a Police Officer or other public officers whose official

duties include the prosecution, detection or punishment of offenders is charged with an

offence under this section arising from

a. the arrest, detention or prosecution of any person for an alleged offence; or

b. an omission to arrest, detain or prosecute a person for an alleged offence or

c. the investigation of an alleged offence.

It shall not be necessary to prove that the accused believed that the offence mention in

paragraph (a), (b) or (c), or any other offences had been committed.

5 (1) Any person who

a. corruptly gives, confesses to or procures any property or benefit of any kind to, on or for a

public officer or to, on or for any other person, or

b. corruptly promises or offers to give, confer, procure or attempt to procure any property or

benefit of any kind to, on or for a public officer or any other person, on account of any such

act, omission, favour or disfavour to be done shall on

6. Any person who

a. Corruptly asks for, receives or obtains any property or benefit of any kind for himself or for

any other person; or corruptly agrees or attempts to receive or obtain any property or benefit

of any kind for himself or for any other person, on account of;

i. anything already done or omitted to be done, or for any favour or disfavour already shown

to any person by a Public Officer in the discharge of his official duties or in relation to any

matter connected with the functions, affairs or business of a government department, public

body or other organization or institution in which the public officer is serving as such; or

ii. anything to be afterwards done or omitted, or any favour or disfavour to be afterwards

shown to any such person; and person by a public officer in the discharge or his official

duties or in relation to any such matter aforesaid, is guilty of the felony of official

corruption and shall on conviction be liable to imprisonment for (7) seven years.

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

35

7. Any person who being employed in the public service, knowingly acquires or holds, directly

or indirectly, otherwise than as a member of a registered joint stock company consisting of

more than twenty (20) persons, a private interest in any contract, agreement or investment

emanating from or connected with the department or office in which he is employed or

which is made on account of the public service, is guilty of a felony, and shall on

conviction be liable to imprisonment for three years.

8. Any person who receives anything which has been obtained by means of any felony or

misdemeanour, or by means of any act done at a place outside Nigeria, which if it had been

done in Nigeria would have constituted a felony or misdemeanour, and which is an offence

under the laws in force in the place where it was done, knowing the same to have been so

obtained, is guilty of felony.

9. If the offence by means of which the thing was obtained is a felony, the offender shall on

conviction be liable to imprisonment for three (3) years, except the thing so obtained was

a postal matter, or any chattel, money or valuable security contained therein, in which case

the offender shall on conviction be liable to imprisonment for seven (7) years.

10. Any person who, with intent to defraud or conceal a crime or frustrate the commission in its

investigation of any suspected crime of corruption under this Act or under any other law;

a. destroys, alters. mutilates, or falsifies any book document,

valuable security, account, computer system, diskette, computer printout or other

electronic device, or is privy to any such act; or

b. Omits, or is privy to omitting, any material particular from any such book,

document, account or electronic record; is guilty of felony, and shall on

conviction be liable to seven (7) years imprisonment.

11. Any person who, being an officer charged with the receipt, custody or use of money or

property received by him or entrusted to his care, or of any balance of money or property in

his possession or under his control, misapplies, misuses or steals it, is guilty of an offence, and

shall on conviction be liable to two (2) years imprisonment.

12. Any person who:

a. as agent corruptly accepts, obtains or agrees to accept or obtain or attempts to obtain from

any person for himself or for any other person, any gift or consideration as an inducement or

reward for doing, forbearing to do or for having done or forborne to do, any act or thing;

b. Corruptly gives or agrees to give or offers any gift or consideration to any agent as an

inducement or reward for doing or forbearing to do, or for having done, or forborne to do,

any act or thing in relation to his principal's affairs or business;

c. Knowingly gives to any agent, or being an agent knowingly uses with

intent to deceive his principal, any receipt, account or other document in respect of which

the principal is interested and which contains any statement which is false or erroneous or

defective in any material particular, and which, to his knowledge, is intended to

mislead his principal or any other person, is guilty of a misdemeanour and shall

on conviction be liable to two (2) years imprisonment or to a fine of ten

thousand naira or to both such imprisonment and fine.

For the purposes of this section, the expression "consideration" includes valuable consideration of

any kind; the expression -"principal" includes an employer.

BUSINESS ETHICS AND SOCIAL RESPONSIBILITY PAGE

36

13. Any person who offers to any public officer. or being a public officer solicits, counsels or

accepts any gratification as an inducement or a reward for:

a. Voting or abstaining from voting at any meeting of the public body in favour of or

against any measure, resolution or question submitted to the public body;

b. Performing or abstaining from performing or aiding in procuring, expediting,

delaying, hindering or preventing the performance of any official act;

c. Aiding in procuring or preventing the passage of any vote or granting of any

contract, award, recognition or advantage in favour of any person; or

d. Showing or forbearing to show any favour or disfavour in his capacity as such officer

shall, notwithstanding that the officer did not have the power, right or opportunity so

to do, or that the inducement or reward was not in relation to the affairs of the public

body, shall be guilty of an offence and shall on conviction be liable to three

(3) years imprisonment with hard labour.

14 (i) Any person who makes or causes any other person to make to an officer of the

commission or to any other Public Officer, in the course of the exercise by such Public

officer of the duties of his office, any statement which to the knowledge of the person

making the statement, or causing the statement to be made.

a. is false, or intended to mislead or is untrue in any material particularly; or

b. is not consistent with any other statement previously made by

such person to any other person having authority or power under any law to receive,

or require to be made such other statement is not under any legal or other obligation

to tell the truth, shall be guilty of an offence and shall on conviction be liable

to fine not exceeding one hundred thousand naira or to imprisonment for