Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Fundamental and Technical Analysis of - Dabur IndiaDocumento24 páginasFundamental and Technical Analysis of - Dabur Indiaramji80% (5)

- BudgetDocumento3 páginasBudgetkawalkaurAinda não há avaliações

- Case Study Pakistan State OilDocumento4 páginasCase Study Pakistan State OilDavidparkash Mirza100% (1)

- Factors Attracting Mncs in IndiaDocumento17 páginasFactors Attracting Mncs in Indiarishi100% (1)

- GST TEST 1 by Vivek GabaDocumento3 páginasGST TEST 1 by Vivek GabaAnkit KumarAinda não há avaliações

- BCPC Functionality - Dilg MC 2008-126Documento1 páginaBCPC Functionality - Dilg MC 2008-126Barangay Panoloon100% (1)

- Ray Dalio - The CycleDocumento20 páginasRay Dalio - The CyclePhương LộcAinda não há avaliações

- Walmart Economic IndicatorsDocumento10 páginasWalmart Economic IndicatorsJennifer Scott100% (1)

- VP Director IT Professional Services in Detroit MI Resume Rick PaulDocumento3 páginasVP Director IT Professional Services in Detroit MI Resume Rick PaulRickPaulAinda não há avaliações

- KSB Pumps - Key Officials With ContactsDocumento3 páginasKSB Pumps - Key Officials With ContactsCatherine JovitaAinda não há avaliações

- Establishing A Stock Exchange in Emerging Economies: Challenges and OpportunitiesDocumento7 páginasEstablishing A Stock Exchange in Emerging Economies: Challenges and OpportunitiesJean Placide BarekeAinda não há avaliações

- Catalogo GROFE IngDocumento50 páginasCatalogo GROFE IngAlvaro Antonio Cristobal AtencioAinda não há avaliações

- Welcome To Indian Railway Passenger Reservation EnquiryDocumento2 páginasWelcome To Indian Railway Passenger Reservation EnquiryChhaviAinda não há avaliações

- Ntse Social Science - The Age of IndustrialisationDocumento7 páginasNtse Social Science - The Age of IndustrialisationMohitAinda não há avaliações

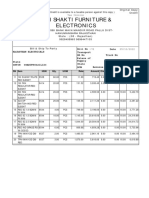

- Shri Shakti Furniture & Electronics: Credit OrginalDocumento1 páginaShri Shakti Furniture & Electronics: Credit OrginalRahul BansalAinda não há avaliações

- BS en 288-4-1992Documento30 páginasBS en 288-4-1992CocaCodaAinda não há avaliações

- Boq 3Documento2 páginasBoq 3China AlemayehouAinda não há avaliações

- Bangalore Architects and Builders 2014-15 Edition - ArchitectsDocumento4 páginasBangalore Architects and Builders 2014-15 Edition - ArchitectsAnisha LaluAinda não há avaliações

- AttachmentDocumento34 páginasAttachmentSiraj ShaikhAinda não há avaliações

- Multiple Choice Questions Distrubution Logistic PDFDocumento14 páginasMultiple Choice Questions Distrubution Logistic PDFYogesh Bantanur50% (2)

- 08 LSF - Load Momment IndicatorDocumento4 páginas08 LSF - Load Momment IndicatorenharAinda não há avaliações

- Agreement For Use of NABL Accredited CAB Combined ILAC MRA MarkDocumento2 páginasAgreement For Use of NABL Accredited CAB Combined ILAC MRA MarkKiranAinda não há avaliações

- Paper One Exam Practice Questions - Tragakes 1Documento12 páginasPaper One Exam Practice Questions - Tragakes 1api-260512563100% (1)

- Capg English - 2Documento5 páginasCapg English - 2Anurag UpadhyayAinda não há avaliações

- Bir Hisar Reject Kharif 2022 Insured PolicyDocumento2 páginasBir Hisar Reject Kharif 2022 Insured PolicyJ StudioAinda não há avaliações

- Studi Kasus LorealDocumento3 páginasStudi Kasus LorealDesni0% (1)

- Panama Natural ResourcesDocumento80 páginasPanama Natural Resourcesgreat2readAinda não há avaliações

- CRUDIFY - The Best Crude Oil Intraday Trading StrategyDocumento11 páginasCRUDIFY - The Best Crude Oil Intraday Trading StrategyRajeswaran DhanagopalanAinda não há avaliações

- Barbados Co-opLIFE Credit Union Funeral InsuranceDocumento11 páginasBarbados Co-opLIFE Credit Union Funeral InsuranceKammie100% (1)

- Maybank Annual Report 2011Documento555 páginasMaybank Annual Report 2011rizza_jamahariAinda não há avaliações