Você também pode gostar

- Law of Direct TaxationDocumento4 páginasLaw of Direct TaxationAshwanth M.SAinda não há avaliações

- Principles of TaxationDocumento7 páginasPrinciples of TaxationNishant RajAinda não há avaliações

- Tamil Nadu National Law University: Course Syllabus Law of Indirect Taxation Course ObjectivesDocumento5 páginasTamil Nadu National Law University: Course Syllabus Law of Indirect Taxation Course ObjectivesreshAinda não há avaliações

- Course Outline For Direct Taxation 2022-2Documento7 páginasCourse Outline For Direct Taxation 2022-2JiaAinda não há avaliações

- Course Curriculum For Direct TaxationDocumento10 páginasCourse Curriculum For Direct TaxationAtulya Singh ChauhanAinda não há avaliações

- Modified Syllabus of Law of TaxationDocumento9 páginasModified Syllabus of Law of TaxationRam Kumar YadavAinda não há avaliações

- V Sem It Course Plan 2011Documento4 páginasV Sem It Course Plan 2011Rohith MaheswariAinda não há avaliações

- Income Tax Act Basics: Section A Study Note 1Documento62 páginasIncome Tax Act Basics: Section A Study Note 1amit kathait100% (1)

- Tax 1 Vthsem Module 1,2, and 3Documento97 páginasTax 1 Vthsem Module 1,2, and 3Sahana narayanAinda não há avaliações

- Galgotias University Taxation Law CourseDocumento22 páginasGalgotias University Taxation Law CourseSumit GuptaAinda não há avaliações

- GST Impact on Indian EconomyDocumento70 páginasGST Impact on Indian EconomyMantsha SayyedAinda não há avaliações

- Taxation IIDocumento5 páginasTaxation IIAnandAinda não há avaliações

- I.T.S-Mnagement & I.T. Institute Mohan Nagar, Ghaziabad Learning Objectives & Lesson PlanDocumento5 páginasI.T.S-Mnagement & I.T. Institute Mohan Nagar, Ghaziabad Learning Objectives & Lesson PlanSourav SharmaAinda não há avaliações

- Taxation - 6 SemesterDocumento28 páginasTaxation - 6 SemesterKhalid123Ainda não há avaliações

- Taxation LawDocumento12 páginasTaxation LawYassar KhanAinda não há avaliações

- Principles of Taxation I SyllabusDocumento7 páginasPrinciples of Taxation I SyllabusShreyaAinda não há avaliações

- LAW OF TAXATION-AnanthaDocumento27 páginasLAW OF TAXATION-AnanthaG Vinoda100% (1)

- Principles of TaxationDocumento8 páginasPrinciples of TaxationPratyush ShanindAinda não há avaliações

- 6 TaxationDocumento183 páginas6 TaxationMehraan AhmedAinda não há avaliações

- Taxation BookDocumento490 páginasTaxation BookMukund PatelAinda não há avaliações

- App Dirt Ax 6Documento490 páginasApp Dirt Ax 6Prem Anand KidambiAinda não há avaliações

- Tax Syllabus (Spit) 2015Documento15 páginasTax Syllabus (Spit) 2015Anonymous XvwKtnSrMRAinda não há avaliações

- Law of Taxation AnanthaDocumento28 páginasLaw of Taxation Ananthasumanjaliganti02Ainda não há avaliações

- Law of Taxation Important Questions 6th SemDocumento29 páginasLaw of Taxation Important Questions 6th SemGulshan RaiAinda não há avaliações

- Direct TaxationDocumento760 páginasDirect TaxationCalmguy Chaitu75% (4)

- Direct Tax - 2011Documento494 páginasDirect Tax - 2011vinagoyaAinda não há avaliações

- GST 7th Edition PDFDocumento366 páginasGST 7th Edition PDFUtkarshAinda não há avaliações

- 9 - Naila Shifa Ramadhana - RPS 1 FADocumento9 páginas9 - Naila Shifa Ramadhana - RPS 1 FANaila shifaAinda não há avaliações

- Indian Taxation System Project ReportDocumento59 páginasIndian Taxation System Project Reportniket_dattaniAinda não há avaliações

- Principles of Taxation IDocumento7 páginasPrinciples of Taxation IMayank SrivastavaAinda não há avaliações

- Principles of Taxation Laws Exam GuideDocumento9 páginasPrinciples of Taxation Laws Exam GuideAshish Singh0% (1)

- Taxation Laws Contents Jan 2017Documento4 páginasTaxation Laws Contents Jan 2017charvinAinda não há avaliações

- MinimumWagesAct1948converted 1Documento40 páginasMinimumWagesAct1948converted 1Dhawal RajAinda não há avaliações

- Revised Commerce Indirect TaxexDocumento4 páginasRevised Commerce Indirect Taxexlipsa PriyadarshiniAinda não há avaliações

- MockDocumento18 páginasMockSmarty ShivamAinda não há avaliações

- LL.B. III Term: Paper - LB - 3033 - Taxation-I (Income Tax)Documento9 páginasLL.B. III Term: Paper - LB - 3033 - Taxation-I (Income Tax)Vishnu BajpaiAinda não há avaliações

- Introduction and Basic Concepts TaxDocumento132 páginasIntroduction and Basic Concepts TaxNaman GoyalAinda não há avaliações

- DTL Whole SyllabusDocumento4 páginasDTL Whole Syllabuss58200204Ainda não há avaliações

- Tax Litigation in India OverviewDocumento38 páginasTax Litigation in India Overviewsarthak mohan shuklaAinda não há avaliações

- Tax Litigation in India OverviewDocumento38 páginasTax Litigation in India Overviewsarthak mohan shuklaAinda não há avaliações

- Course Outline IDTDocumento12 páginasCourse Outline IDTcvcvAinda não há avaliações

- BCO 11 Block 03Documento70 páginasBCO 11 Block 03Al OkAinda não há avaliações

- Corporate Tax Management EDU MBA Summer 2020Documento100 páginasCorporate Tax Management EDU MBA Summer 2020Foyez HafizAinda não há avaliações

- DTaxation PDFDocumento808 páginasDTaxation PDFcoolmanzAinda não há avaliações

- Taxation of Corps & Commodities GuideDocumento39 páginasTaxation of Corps & Commodities Guidesap6370Ainda não há avaliações

- Business TaxationDocumento319 páginasBusiness TaxationsiddheshAinda não há avaliações

- Income Tax Part 1 (Theory + MCQ)Documento200 páginasIncome Tax Part 1 (Theory + MCQ)Neha SharmaAinda não há avaliações

- Tax Structure of IndiaDocumento30 páginasTax Structure of Indiaankit singhAinda não há avaliações

- Tax1 Dimaampao Lecture NotesDocumento61 páginasTax1 Dimaampao Lecture NotesSui100% (1)

- WJJ C 7Documento304 páginasWJJ C 7aditya.c122Ainda não há avaliações

- Mapping Property Tax Reform in Southeast AsiaNo EverandMapping Property Tax Reform in Southeast AsiaAinda não há avaliações

- Taxation in Ghana: a Fiscal Policy Tool for Development: 75 Years ResearchNo EverandTaxation in Ghana: a Fiscal Policy Tool for Development: 75 Years ResearchNota: 5 de 5 estrelas5/5 (1)

- Tool Kit for Tax Administration Management Information SystemNo EverandTool Kit for Tax Administration Management Information SystemNota: 1 de 5 estrelas1/5 (1)

- Prospects of Regional Economic Cooperation in South Asia: With Special Studies on indian IndustryNo EverandProspects of Regional Economic Cooperation in South Asia: With Special Studies on indian IndustryAinda não há avaliações

- Public Sector Accounting and Administrative Practices in Nigeria Volume 1No EverandPublic Sector Accounting and Administrative Practices in Nigeria Volume 1Ainda não há avaliações

- Green Products Co. Vs Independent Corn by Products (1997) : Damage Due To Initial Consumer ConfusionDocumento20 páginasGreen Products Co. Vs Independent Corn by Products (1997) : Damage Due To Initial Consumer ConfusionABHIJEETAinda não há avaliações

- GRC Test BankDocumento123 páginasGRC Test Bankshams319100% (8)

- Bill For Compulsory VotingDocumento2 páginasBill For Compulsory VotingABHIJEETAinda não há avaliações

- Supreme Court On Custodial DeathDocumento26 páginasSupreme Court On Custodial DeathAlvy Singer100% (3)

- Socio-Legal Study of Child AbuseDocumento2 páginasSocio-Legal Study of Child AbuseABHIJEETAinda não há avaliações

- CRPC ProjectDocumento26 páginasCRPC ProjectNidhi Malhotra100% (3)

- National Bank For Agriculture and Rural Devlopment (Nabard) : Chapter-I: IntroductionDocumento2 páginasNational Bank For Agriculture and Rural Devlopment (Nabard) : Chapter-I: IntroductionABHIJEETAinda não há avaliações

- The Compulsory Voting Bill, 2014: S Introduced IN OK AbhaDocumento7 páginasThe Compulsory Voting Bill, 2014: S Introduced IN OK AbhaABHIJEETAinda não há avaliações

- Dr. Swapan Kumar Roy, Rural Development in India: What Roles Do Nabard & Rrbs Play?Documento19 páginasDr. Swapan Kumar Roy, Rural Development in India: What Roles Do Nabard & Rrbs Play?ABHIJEETAinda não há avaliações

- European Commission On Voting RightsDocumento17 páginasEuropean Commission On Voting RightsABHIJEETAinda não há avaliações

- Section 304-B AnalysisDocumento12 páginasSection 304-B AnalysisABHIJEETAinda não há avaliações

- Taxation of Capital Gains - A Comparative StudyDocumento28 páginasTaxation of Capital Gains - A Comparative StudyABHIJEETAinda não há avaliações

- Abhi 11Documento1 páginaAbhi 11ABHIJEETAinda não há avaliações

- Abhi 11Documento1 páginaAbhi 11ABHIJEETAinda não há avaliações

- Union of India vs Azadi Bachao Andolan: Analysis of Double Taxation Avoidance AgreementsDocumento4 páginasUnion of India vs Azadi Bachao Andolan: Analysis of Double Taxation Avoidance AgreementsAditi Bhaniramka0% (2)

- Law of Direct Taxation Unit III Problem Set 2Documento1 páginaLaw of Direct Taxation Unit III Problem Set 2ABHIJEETAinda não há avaliações

- AssignmentDocumento3 páginasAssignmentABHIJEETAinda não há avaliações

- Stamp ActDocumento3 páginasStamp ActABHIJEETAinda não há avaliações

- Preventing Custodial Violence and TortureDocumento13 páginasPreventing Custodial Violence and TortureArun Bala100% (1)

- BA0140001 CPC ProjectDocumento20 páginasBA0140001 CPC ProjectABHIJEETAinda não há avaliações

- Dr. Ram Manohar Lohiya National Law University, LucknowDocumento12 páginasDr. Ram Manohar Lohiya National Law University, LucknowABHIJEETAinda não há avaliações

- Inherent Powers of Courts to Reduce Delay in Civil CasesDocumento1 páginaInherent Powers of Courts to Reduce Delay in Civil CasesABHIJEETAinda não há avaliações

- Ace - SHA - Comments of Promoters (261115)Documento9 páginasAce - SHA - Comments of Promoters (261115)ABHIJEETAinda não há avaliações

- Courts' Inherent Powers and Avoiding Delay in Civil CasesDocumento2 páginasCourts' Inherent Powers and Avoiding Delay in Civil CasesABHIJEETAinda não há avaliações

- School of Oriental and African Studies Journal of African LawDocumento32 páginasSchool of Oriental and African Studies Journal of African LawABHIJEETAinda não há avaliações

- Lease: Premium, and The Money, Share, Service or Other Thing To Be So Rendered Is Called The RentDocumento6 páginasLease: Premium, and The Money, Share, Service or Other Thing To Be So Rendered Is Called The RentABHIJEETAinda não há avaliações

- Labour Law-II Syllabus KGDocumento3 páginasLabour Law-II Syllabus KGABHIJEETAinda não há avaliações

- Review of LiteratureDocumento5 páginasReview of LiteratureABHIJEETAinda não há avaliações

- 3 Other Void Ag Quasi To PrintDocumento27 páginas3 Other Void Ag Quasi To PrintABHIJEETAinda não há avaliações

- A Global Guide To M&A - India: by Vivek Gupta and Rohit BerryDocumento14 páginasA Global Guide To M&A - India: by Vivek Gupta and Rohit BerryvinaymathewAinda não há avaliações

- Theoritical Framework &literature ReviewDocumento27 páginasTheoritical Framework &literature ReviewGelani PradipAinda não há avaliações

- Chapter 22Documento61 páginasChapter 22Tim LeeAinda não há avaliações

- Downloadfile 30 PDFDocumento114 páginasDownloadfile 30 PDFYianniAnd Sophia0% (1)

- Premature Manipulator With Kyler Quin, Diego Perez, Armani Black, Lukas King Brazzers OfficialDocumento1 páginaPremature Manipulator With Kyler Quin, Diego Perez, Armani Black, Lukas King Brazzers Officialmarko.ilic.ns08Ainda não há avaliações

- The Cash Transactions and Cash Balances of Banner Inc ForDocumento1 páginaThe Cash Transactions and Cash Balances of Banner Inc Foramit raajAinda não há avaliações

- Case Study: 3.1. Monograph AccountingDocumento6 páginasCase Study: 3.1. Monograph AccountingAlex UrdeaAinda não há avaliações

- iGB Personal Bank Account Fee Information Document 31mar2023Documento2 páginasiGB Personal Bank Account Fee Information Document 31mar2023chen jam (1314)Ainda não há avaliações

- CIR V CA and GCLDocumento2 páginasCIR V CA and GCLWilliam SantosAinda não há avaliações

- Baste 2010 Final Examination Questions - Tax 2Documento2 páginasBaste 2010 Final Examination Questions - Tax 2Judith AlisuagAinda não há avaliações

- Account Statement SummaryDocumento5 páginasAccount Statement SummaryManthan BeladiyaAinda não há avaliações

- Vavdiya Mahesh ChanneiDocumento1 páginaVavdiya Mahesh ChanneiANISH SHAIKHAinda não há avaliações

- BFCI FINAL ENGAGEMENT PROPOSAL Silver FernDocumento2 páginasBFCI FINAL ENGAGEMENT PROPOSAL Silver FernGeram ConcepcionAinda não há avaliações

- 77Documento2 páginas77Arian AmuraoAinda não há avaliações

- ConfirmationDocumento2 páginasConfirmationAntoinette SantosAinda não há avaliações

- Wholesale Credit AppDocumento3 páginasWholesale Credit AppReload GamingAinda não há avaliações

- Navin Fluorine Advanced Sciences LTD - 346 - 22-11-2021Documento1 páginaNavin Fluorine Advanced Sciences LTD - 346 - 22-11-2021Pragnesh PrajapatiAinda não há avaliações

- Bar Questions in Taxation 1987-2001Documento62 páginasBar Questions in Taxation 1987-2001Carlos Ryan RabangAinda não há avaliações

- Bir Ruling (Da 146 04)Documento4 páginasBir Ruling (Da 146 04)cool_peachAinda não há avaliações

- Anak Mami PenangDocumento1 páginaAnak Mami PenangAnonymous fE2l3DzlAinda não há avaliações

- Aparna Western MeadowsDocumento9 páginasAparna Western Meadowsa_veerenderAinda não há avaliações

- Account Statement As of 05-06-2020 12:14:26 GMT +0530Documento9 páginasAccount Statement As of 05-06-2020 12:14:26 GMT +0530Arun VeeraniAinda não há avaliações

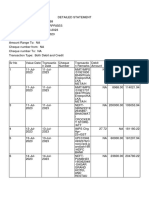

- Detailstatement - 19 7 2023@15 21 27Documento2 páginasDetailstatement - 19 7 2023@15 21 27aarti RwtAinda não há avaliações

- Mutation CertificateDocumento1 páginaMutation CertificateGD CONSULTANCYAinda não há avaliações

- Invoice for Pharmaceutical ProductsDocumento1 páginaInvoice for Pharmaceutical Productskeylor moraAinda não há avaliações

- T - Codes (Sap-Fico)Documento5 páginasT - Codes (Sap-Fico)AJAinda não há avaliações

- File Return On TimeDocumento7 páginasFile Return On TimeAmanat AhmedAinda não há avaliações

- Revenue Regulations No. 01-99: Rule 1.coverageDocumento24 páginasRevenue Regulations No. 01-99: Rule 1.coveragesaintkarriAinda não há avaliações

- Monese Statement 01 May 2023 - 23 August 2023Documento12 páginasMonese Statement 01 May 2023 - 23 August 2023Andrea SarocoAinda não há avaliações

- Booktopia ChargingDocumento1 páginaBooktopia CharginguzairAinda não há avaliações