Você também pode gostar

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (120)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- Internal Quality Management System Audit Checklist (ISO/TS 16949:2009)Documento48 páginasInternal Quality Management System Audit Checklist (ISO/TS 16949:2009)sharif1974Ainda não há avaliações

- MS 900T01 Microsoft 365 Fundamentals MCT PDFDocumento158 páginasMS 900T01 Microsoft 365 Fundamentals MCT PDFhernan100% (1)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Slides Business Level StrategyDocumento24 páginasSlides Business Level StrategyThảo PhạmAinda não há avaliações

- 3464172Documento34 páginas3464172Aasri RAinda não há avaliações

- Personality Case StudyDocumento2 páginasPersonality Case StudyShams Ul HayatAinda não há avaliações

- Technology TransferDocumento58 páginasTechnology TransferVaishali YardiAinda não há avaliações

- Citizens State Bank v. Country Wide 949 NE2 1195Documento14 páginasCitizens State Bank v. Country Wide 949 NE2 1195OAITAAinda não há avaliações

- NAILTA Amicus - Edwards v. First AmericanDocumento50 páginasNAILTA Amicus - Edwards v. First AmericanOAITAAinda não há avaliações

- American Escrow Association, Et Al. Amicus Curiae in Edwards v. First AmericanDocumento25 páginasAmerican Escrow Association, Et Al. Amicus Curiae in Edwards v. First AmericanOAITAAinda não há avaliações

- Upreme Eurt Ef: in TheDocumento21 páginasUpreme Eurt Ef: in TheOAITAAinda não há avaliações

- Citizens State Bank v. Country Wide 949 NE2 1195Documento14 páginasCitizens State Bank v. Country Wide 949 NE2 1195OAITAAinda não há avaliações

- Stewart AmicusDocumento30 páginasStewart AmicusOAITAAinda não há avaliações

- OAITA Settlement Preference Survey - Executive SummaryDocumento6 páginasOAITA Settlement Preference Survey - Executive SummaryOAITAAinda não há avaliações

- RESPRO Letter To Fed On QRMDocumento8 páginasRESPRO Letter To Fed On QRMOAITAAinda não há avaliações

- Citizens State Bank v. Country Wide 949 NE2 1195Documento14 páginasCitizens State Bank v. Country Wide 949 NE2 1195OAITAAinda não há avaliações

- Minter Certification Order 05-03-2011Documento81 páginasMinter Certification Order 05-03-2011OAITAAinda não há avaliações

- NAILTA: Why Congress Should Examine HR 2425 and MERS TogetherDocumento6 páginasNAILTA: Why Congress Should Examine HR 2425 and MERS TogetherOAITAAinda não há avaliações

- NAILTA's Position On Private Transfer Fee CovenantsDocumento4 páginasNAILTA's Position On Private Transfer Fee CovenantsOAITAAinda não há avaliações

- ALTA's Amicus Curiae Brief in Support of First American (Edwards v. First American - U.S. Supreme Court Case)Documento37 páginasALTA's Amicus Curiae Brief in Support of First American (Edwards v. First American - U.S. Supreme Court Case)OAITAAinda não há avaliações

- In Re AGARDDocumento37 páginasIn Re AGARDA. CampbellAinda não há avaliações

- Empire Title Complaint 09-30-2010Documento40 páginasEmpire Title Complaint 09-30-2010OAITAAinda não há avaliações

- Amicus Brief of ALTA and The National Title Insurance UnderwritersDocumento10 páginasAmicus Brief of ALTA and The National Title Insurance UnderwritersOAITAAinda não há avaliações

- Amicus Brief of RESPRO, NAR, MBA and The American Escrow AssociationDocumento13 páginasAmicus Brief of RESPRO, NAR, MBA and The American Escrow AssociationOAITAAinda não há avaliações

- ALTA Memorandum On Carter CaseDocumento2 páginasALTA Memorandum On Carter CaseOAITAAinda não há avaliações

- Fidelity National Title Group's Indiana Search StandardsDocumento5 páginasFidelity National Title Group's Indiana Search StandardsOAITAAinda não há avaliações

- Fidelity National Title Group's Indiana Search StandardsDocumento5 páginasFidelity National Title Group's Indiana Search StandardsOAITAAinda não há avaliações

- H.R. 6460 - The Transparency and Security Mortgage Registration Act of 2010Documento13 páginasH.R. 6460 - The Transparency and Security Mortgage Registration Act of 2010OAITA100% (1)

- NAILTA White Paper On MERS & H.R. 6460Documento7 páginasNAILTA White Paper On MERS & H.R. 6460OAITAAinda não há avaliações

- Fifth Third Bank's Motion To Dismiss The Empire Title ComplaintDocumento37 páginasFifth Third Bank's Motion To Dismiss The Empire Title ComplaintOAITAAinda não há avaliações

- NAILTA's Amicus Curiae BriefDocumento36 páginasNAILTA's Amicus Curiae BriefOAITAAinda não há avaliações

- NAILTA's Position On Private Transfer Fee CovenantsDocumento4 páginasNAILTA's Position On Private Transfer Fee CovenantsOAITAAinda não há avaliações

- NAILTA Foreclosure Memo 10-13-2010Documento4 páginasNAILTA Foreclosure Memo 10-13-2010OAITAAinda não há avaliações

- Cordray Foreclosure LetterDocumento2 páginasCordray Foreclosure LetterOAITAAinda não há avaliações

- Alta - Hud Anpr ResponseDocumento3 páginasAlta - Hud Anpr ResponseOAITAAinda não há avaliações

- Magistrate's Decision in ODI LitigationDocumento21 páginasMagistrate's Decision in ODI LitigationOAITA100% (1)

- Cadbury Project Deliverables RACI ChartDocumento2 páginasCadbury Project Deliverables RACI ChartoraywattAinda não há avaliações

- 10 Practice Problems Monopoly Price DiscrimDocumento12 páginas10 Practice Problems Monopoly Price Discrimphineas12345678910ferbAinda não há avaliações

- 003 SHORT QUIZ - Professional Practice, Standards, and Quality Control System - ACTG411 Assurance Principles, Professional Ethics & Good GovDocumento2 páginas003 SHORT QUIZ - Professional Practice, Standards, and Quality Control System - ACTG411 Assurance Principles, Professional Ethics & Good GovMarilou PanisalesAinda não há avaliações

- Ayan Chakravarty BrandwagonDocumento5 páginasAyan Chakravarty BrandwagonAyan ChakravartyAinda não há avaliações

- (Solved) 1.why Is - People, Planet, Profits - A More Media - Friendly... - Course HeroDocumento3 páginas(Solved) 1.why Is - People, Planet, Profits - A More Media - Friendly... - Course HeroayeshaAinda não há avaliações

- GeM Bidding 4885013Documento4 páginasGeM Bidding 4885013MaheshAinda não há avaliações

- West Teleservice: Case QuestionsDocumento1 páginaWest Teleservice: Case QuestionsAlejandro García AcostaAinda não há avaliações

- BUS 6070 FinalProjectDocumento10 páginasBUS 6070 FinalProjectHafsat Saliu100% (2)

- Internal and External Vacancy Announcement (Laboratory & Logistics Officer)Documento2 páginasInternal and External Vacancy Announcement (Laboratory & Logistics Officer)Phr InitiativeAinda não há avaliações

- Guia AereaDocumento1 páginaGuia AereaLuisa Rios HernandezAinda não há avaliações

- This Study Resource Was: Joyce Ann Clarize GalangDocumento6 páginasThis Study Resource Was: Joyce Ann Clarize GalangYamna HasanAinda não há avaliações

- Pre-Event Networking Preparation - Making The Most From Networking EventsDocumento10 páginasPre-Event Networking Preparation - Making The Most From Networking EventsRob BrownAinda não há avaliações

- 2nd Phase TestDocumento6 páginas2nd Phase TestFaiza OmarAinda não há avaliações

- Lecture Note 3 - Globalization and Role of MNCSDocumento64 páginasLecture Note 3 - Globalization and Role of MNCSgydoiAinda não há avaliações

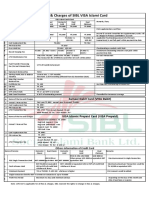

- Fees and Charges of SIBL Islami CardDocumento1 páginaFees and Charges of SIBL Islami CardMd YusufAinda não há avaliações

- Operations Management-Chapter FiveDocumento64 páginasOperations Management-Chapter FiveAGAinda não há avaliações

- Director VP Marketing in Boston MA Resume Jeffrey LawsonDocumento2 páginasDirector VP Marketing in Boston MA Resume Jeffrey LawsonJeffreyLawsonAinda não há avaliações

- Comm3201 Individual Case Study (June 2020)Documento3 páginasComm3201 Individual Case Study (June 2020)Scarlett WangAinda não há avaliações

- EU Transition Timeline Whitepaper PDFDocumento10 páginasEU Transition Timeline Whitepaper PDFWFreeAinda não há avaliações

- ThesisDocumento104 páginasThesisJerry B CruzAinda não há avaliações

- Pelaksanaan Program Pembinaan Koperasi Usaha Mikro Kecil Dan Menengah (Umkm)Documento7 páginasPelaksanaan Program Pembinaan Koperasi Usaha Mikro Kecil Dan Menengah (Umkm)Razief Firdaus 043Ainda não há avaliações

- Assignment of Labor and Organizational Management by Edris AbdellaDocumento14 páginasAssignment of Labor and Organizational Management by Edris AbdellaEdris Abdella NuureAinda não há avaliações

- CAPMDocumento4 páginasCAPMhamza hamzaAinda não há avaliações

- Consignment Agreement (Panjang)Documento3 páginasConsignment Agreement (Panjang)Izzat SyazwanAinda não há avaliações