Você também pode gostar

- Goods and Services Tax (GST) in India: A Presentation by KRISHNA SHUKLADocumento30 páginasGoods and Services Tax (GST) in India: A Presentation by KRISHNA SHUKLAKrishna ShuklaAinda não há avaliações

- GST PPT TaxguruDocumento30 páginasGST PPT TaxgurupraveerAinda não há avaliações

- Understanding Goods and Services TaxDocumento23 páginasUnderstanding Goods and Services TaxTEst User 44452Ainda não há avaliações

- Tally AssignmentDocumento28 páginasTally Assignmentsenthil kumar100% (1)

- Material - GSTDocumento18 páginasMaterial - GSTDeepak NimmojiAinda não há avaliações

- GST Entries For Every Month SalesDocumento3 páginasGST Entries For Every Month SalesGiri Sukumar100% (1)

- GST Section ListDocumento7 páginasGST Section ListRahul ThapaAinda não há avaliações

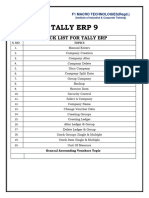

- Tally Erp 9 Practise Set 1Documento28 páginasTally Erp 9 Practise Set 1Anusha ShettyAinda não há avaliações

- Goods and Service Tax (GST)Documento19 páginasGoods and Service Tax (GST)Saurabh Kumar SharmaAinda não há avaliações

- GST Module 1 Compiled PDFDocumento285 páginasGST Module 1 Compiled PDFRahul DoshiAinda não há avaliações

- GST Oct 17Documento23 páginasGST Oct 17himanAinda não há avaliações

- GST in India: Prepared By:-Shubham SharmaDocumento57 páginasGST in India: Prepared By:-Shubham Sharmamurali140Ainda não há avaliações

- GST PPT Tkil FinalDocumento53 páginasGST PPT Tkil FinalVikas SharmaAinda não há avaliações

- GST BookDocumento100 páginasGST BookNaman ChopraAinda não há avaliações

- Reading Material AccountantDocumento123 páginasReading Material Accountantsatyanweshi truthseeker100% (1)

- CS - EXE - Income Tax - Notes - Combined PDFDocumento437 páginasCS - EXE - Income Tax - Notes - Combined PDFRam Iyer100% (1)

- Tally - ERP9 Book With GSTDocumento1.843 páginasTally - ERP9 Book With GSThatimAinda não há avaliações

- Test 3Documento7 páginasTest 3info view0% (1)

- Bank of India Fund BasedDocumento33 páginasBank of India Fund Basedhariram v choudharyAinda não há avaliações

- List of Ledgers and It's Under Group in TallyDocumento5 páginasList of Ledgers and It's Under Group in Tallyrachel KujurAinda não há avaliações

- GST ManualDocumento19 páginasGST ManualSubhaAinda não há avaliações

- List of Sections GST: CA Yachana Mutha Bhurat 09669357770Documento5 páginasList of Sections GST: CA Yachana Mutha Bhurat 09669357770SreelakshmiMinnalaAinda não há avaliações

- GST Practical Record 40-50Documento48 páginasGST Practical Record 40-50Aditya raj ojhaAinda não há avaliações

- GST - Last Day Revision Notes PDFDocumento98 páginasGST - Last Day Revision Notes PDFShubham PathakAinda não há avaliações

- Dr. Shakuntala Misra National Rehabilitation University: Lucknow Faculty of LawDocumento9 páginasDr. Shakuntala Misra National Rehabilitation University: Lucknow Faculty of LawVimal SinghAinda não há avaliações

- 59journal Solved Assignment 13 14Documento7 páginas59journal Solved Assignment 13 14Monica SainiAinda não há avaliações

- Tally Prime Course PayrollDocumento7 páginasTally Prime Course PayrollElakiyaaAinda não há avaliações

- GST Practical Test 1Documento1 páginaGST Practical Test 1Amir KhanAinda não há avaliações

- List of Ledgers: S.No Ledger Name Under: GroupDocumento5 páginasList of Ledgers: S.No Ledger Name Under: GroupSuraj KumarAinda não há avaliações

- Calculation of GSTDocumento13 páginasCalculation of GSTSukanta PalAinda não há avaliações

- GST Book PDFDocumento606 páginasGST Book PDFsaddamAinda não há avaliações

- 40 Final Accounts FormatDocumento3 páginas40 Final Accounts FormatAditya GowdaAinda não há avaliações

- What Is GST?: Multi-StageDocumento10 páginasWhat Is GST?: Multi-StagexyzAinda não há avaliações

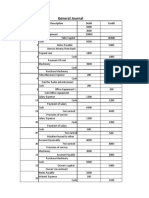

- General Journal: Date Description Debit CreditDocumento7 páginasGeneral Journal: Date Description Debit CreditAmanuel DemekeAinda não há avaliações

- Tax FinalDocumento23 páginasTax FinalJitender ChaudharyAinda não há avaliações

- Goods and Service Tax (GST)Documento17 páginasGoods and Service Tax (GST)Manav SethiAinda não há avaliações

- List of Important Sections - GST May 2023 by CA Kishan KumarDocumento5 páginasList of Important Sections - GST May 2023 by CA Kishan KumarNarayan choudharyAinda não há avaliações

- Ap (Accounts Payable) ProcessDocumento10 páginasAp (Accounts Payable) ProcessRabin DebnathAinda não há avaliações

- STUDY MATERIAL AccountingcomClass XIDocumento144 páginasSTUDY MATERIAL AccountingcomClass XImalathi SAinda não há avaliações

- GST RoadmapDocumento14 páginasGST Roadmapsiddhumesh1Ainda não há avaliações

- Test 2Documento10 páginasTest 2himanshuAinda não há avaliações

- Six Day in Tally Class (What Is Ledger and How To Create Ledger in Tally)Documento9 páginasSix Day in Tally Class (What Is Ledger and How To Create Ledger in Tally)Kamlesh KumarAinda não há avaliações

- Set 1 & 3 PDFDocumento6 páginasSet 1 & 3 PDFCorona VirusAinda não há avaliações

- Tally Sample Paper With GST Feb 2023Documento3 páginasTally Sample Paper With GST Feb 2023Bhumi NavtiaAinda não há avaliações

- GST Pracital Class 2Documento7 páginasGST Pracital Class 2Nayan JhaAinda não há avaliações

- Accounting and Finance Numericals Problems and AnsDocumento11 páginasAccounting and Finance Numericals Problems and AnsPramodh Kanulla0% (1)

- Tally Practical (B) - 1Documento3 páginasTally Practical (B) - 1Bhaavya GuptaAinda não há avaliações

- Accounting Entries Under GST For Different SituationsDocumento42 páginasAccounting Entries Under GST For Different Situationsamit chavariaAinda não há avaliações

- Cost of Project and Means of Finance Cost of Project Amount (RS)Documento9 páginasCost of Project and Means of Finance Cost of Project Amount (RS)Manish AgarwalAinda não há avaliações

- Assignment 1 ACCOUNTANCYDocumento3 páginasAssignment 1 ACCOUNTANCYCHINMAY AGRAWALAinda não há avaliações

- AMFI - Investor Awareness Presentation - Jul'23Documento69 páginasAMFI - Investor Awareness Presentation - Jul'23padmaniaAinda não há avaliações

- Questions On Trial Balance To StudentsDocumento6 páginasQuestions On Trial Balance To Studentsveraji3735Ainda não há avaliações

- Tally Assignment Yash ComDocumento9 páginasTally Assignment Yash Comraj S.NAinda não há avaliações

- Accounting BasicsDocumento21 páginasAccounting BasicsasifparwezAinda não há avaliações

- GSTDocumento9 páginasGSTCelina AlexAinda não há avaliações

- Tally E Book 2Documento154 páginasTally E Book 2anjali44499Ainda não há avaliações

- Key Words: Multiple Choice QuestionsDocumento7 páginasKey Words: Multiple Choice QuestionsMOHAMMED AMIN SHAIKHAinda não há avaliações

- Tally AssignmentDocumento25 páginasTally AssignmentHimanshu YadavAinda não há avaliações

- Goods & Services Tax: Are You Ready For The Change?Documento3 páginasGoods & Services Tax: Are You Ready For The Change?Ashish PandeyAinda não há avaliações

- Summer Trainning PresentationDocumento20 páginasSummer Trainning PresentationUnpacked MusicAinda não há avaliações

- Ai & IotDocumento7 páginasAi & IotPiyush BhirudAinda não há avaliações

- Bouquet Type Quantity Unit Price Sales Value: Total 2069 $34,920.37Documento1 páginaBouquet Type Quantity Unit Price Sales Value: Total 2069 $34,920.37Piyush BhirudAinda não há avaliações

- Practice WorkbookDocumento12 páginasPractice WorkbookPiyush BhirudAinda não há avaliações

- Glossary May 02Documento20 páginasGlossary May 02Vikas SuryavanshiAinda não há avaliações

- New Microsoft Excel WorksheetDocumento4 páginasNew Microsoft Excel WorksheetPiyush BhirudAinda não há avaliações

- Apple Case ReportDocumento2 páginasApple Case ReportAwa SannoAinda não há avaliações

- Islamic StudyDocumento80 páginasIslamic StudyWasim khan100% (1)

- Women and Globalization PDFDocumento12 páginasWomen and Globalization PDFrithikkumuthaAinda não há avaliações

- Accounting Concepts and Conventions MCQs Financial Accounting MCQs Part 2 Multiple Choice QuestionsDocumento9 páginasAccounting Concepts and Conventions MCQs Financial Accounting MCQs Part 2 Multiple Choice QuestionsKanika BajajAinda não há avaliações

- Cambridge IGCSE™: Information and Communication Technology 0417/12Documento9 páginasCambridge IGCSE™: Information and Communication Technology 0417/12Ibrahim Abdi ChirwaAinda não há avaliações

- US Internal Revenue Service: Irb04-43Documento27 páginasUS Internal Revenue Service: Irb04-43IRSAinda não há avaliações

- Motion For Re-RaffleDocumento3 páginasMotion For Re-RaffleJoemar CalunaAinda não há avaliações

- AcadinfoDocumento10 páginasAcadinfoYumi LingAinda não há avaliações

- Managing Transaction ExposureDocumento34 páginasManaging Transaction Exposureg00028007Ainda não há avaliações

- DMDocumento12 páginasDMDelfin Mundala JrAinda não há avaliações

- Hho Dry DiagramDocumento7 páginasHho Dry Diagramdesertbloom100% (2)

- 121 Diamond Hill Funds Annual Report - 2009Documento72 páginas121 Diamond Hill Funds Annual Report - 2009DougAinda não há avaliações

- Standard Oil Co. of New York vs. Lopez CasteloDocumento1 páginaStandard Oil Co. of New York vs. Lopez CasteloRic Sayson100% (1)

- Professionals and Practitioners in Counselling: 1. Roles, Functions, and Competencies of CounselorsDocumento70 páginasProfessionals and Practitioners in Counselling: 1. Roles, Functions, and Competencies of CounselorsShyra PapaAinda não há avaliações

- WukolumDocumento2 páginasWukolumHammed OkusiAinda não há avaliações

- Hazing in The PhilippinesDocumento24 páginasHazing in The PhilippinesEdz Votefornoymar Del Rosario100% (2)

- Student Copy of Function OperationsDocumento8 páginasStudent Copy of Function OperationsAnoop SreedharAinda não há avaliações

- Definition of ConsiderationDocumento3 páginasDefinition of ConsiderationZain IrshadAinda não há avaliações

- Tallado V. ComelecDocumento3 páginasTallado V. ComelecLorelain ImperialAinda não há avaliações

- Application For DiggingDocumento3 páginasApplication For DiggingDhathri. vAinda não há avaliações

- Bba - Fa Ii - Notes - Ii Sem PDFDocumento40 páginasBba - Fa Ii - Notes - Ii Sem PDFPRABHUDEVAAinda não há avaliações

- The Earliest Hospitals EstablishedDocumento3 páginasThe Earliest Hospitals EstablishedJonnessa Marie MangilaAinda não há avaliações

- Questionnaire DellDocumento15 páginasQuestionnaire Dellkumarrohit352100% (2)

- "Land Enough in The World" - Locke's Golden Age and The Infinite Extension of "Use"Documento21 páginas"Land Enough in The World" - Locke's Golden Age and The Infinite Extension of "Use"resperadoAinda não há avaliações

- What Is Ecocroticism - GlotfeltyDocumento3 páginasWhat Is Ecocroticism - GlotfeltyUmut AlıntaşAinda não há avaliações

- Case Digest - WitnessDocumento9 páginasCase Digest - WitnessEmmagine E EyanaAinda não há avaliações

- BIOETHICSDocumento4 páginasBIOETHICSSherylou Kumo SurioAinda não há avaliações

- Cement SegmentDocumento18 páginasCement Segmentmanish1895Ainda não há avaliações

- HSE RMO and Deliverables - Asset Life Cycle - Rev0Documento4 páginasHSE RMO and Deliverables - Asset Life Cycle - Rev0Medical Service MPIAinda não há avaliações

- Bharat Prachin Eanv Aadhunik Shiksha Pranali: Ek Gahan AdhyayanDocumento6 páginasBharat Prachin Eanv Aadhunik Shiksha Pranali: Ek Gahan AdhyayanAnonymous CwJeBCAXpAinda não há avaliações