Você também pode gostar

- Siemens Drives - SINAMICS G110 Operating InstructionsDocumento92 páginasSiemens Drives - SINAMICS G110 Operating Instructionsmelfer100% (3)

- Crearea Unei Lumi Fizice Şi Digitale Conectate Şi Integrate: Servicii, Posibilităţi Şi Tehnologii Generice 6G"Documento64 páginasCrearea Unei Lumi Fizice Şi Digitale Conectate Şi Integrate: Servicii, Posibilităţi Şi Tehnologii Generice 6G"start-up.roAinda não há avaliações

- Cost Benefit Analysis 03Documento8 páginasCost Benefit Analysis 03Shreepathi AdigaAinda não há avaliações

- 08 04 2013biologicalvol1Documento100 páginas08 04 2013biologicalvol1sameditzoAinda não há avaliações

- Manual For LivingDocumento108 páginasManual For LivingJana Vuković100% (1)

- MatrixDocumento12 páginasMatrixeettielaAinda não há avaliações

- Book - Keeping and AccountingDocumento5 páginasBook - Keeping and AccountingAshish DhakalAinda não há avaliações

- Variador Micromaster 6SE9213-6CA40 PDFDocumento42 páginasVariador Micromaster 6SE9213-6CA40 PDFJeyson Castillo MenaAinda não há avaliações

- Despre Vaccin 1917Documento2 páginasDespre Vaccin 1917Sandro PardaileanAinda não há avaliações

- Neuromodulation (2) (Autosaved)Documento35 páginasNeuromodulation (2) (Autosaved)aartiAinda não há avaliações

- Part1 r31Documento217 páginasPart1 r31Prica Petrica IulianAinda não há avaliações

- Transport Phenomena in Nervous System PDFDocumento538 páginasTransport Phenomena in Nervous System PDFUdayanidhi RAinda não há avaliações

- EpigeneticaDocumento11 páginasEpigeneticaIoanaPurrrAinda não há avaliações

- CommunicationDocumento4 páginasCommunicationOanaCanditAinda não há avaliações

- ManipulareDocumento5 páginasManipularemuheecanewAinda não há avaliações

- CV Europass GB FlorinaMoldovanDocumento4 páginasCV Europass GB FlorinaMoldovanmihaicornelAinda não há avaliações

- Acupunctura Mijloc de Recuperare Functionala Tiberiu RaibuletDocumento4 páginasAcupunctura Mijloc de Recuperare Functionala Tiberiu RaibuletLebada IoanAinda não há avaliações

- Fulfilment of The Semester-Market StrategiesDocumento6 páginasFulfilment of The Semester-Market StrategiesDoina ŞerbulAinda não há avaliações

- Dieta 1Documento1 páginaDieta 1Odri BluecatAinda não há avaliações

- Dumitru Ioan Branc Trezirea Spirituala Si Vindecarea Totala in Noua Energie PDFDocumento1 páginaDumitru Ioan Branc Trezirea Spirituala Si Vindecarea Totala in Noua Energie PDFAna Railean100% (1)

- Pressure Transmitters: Tronic LineDocumento4 páginasPressure Transmitters: Tronic LineMohamed ElmakkyAinda não há avaliações

- Captură de Ecran Din 2022-03-01 La 20.59.12Documento1 páginaCaptură de Ecran Din 2022-03-01 La 20.59.12Stefano SerafinoAinda não há avaliações

- MSDS Hygienium Antibacterial Gel DisinfectantDocumento9 páginasMSDS Hygienium Antibacterial Gel DisinfectantPetrica DascaluAinda não há avaliações

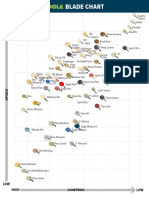

- Joola Blade Comparison PDFDocumento1 páginaJoola Blade Comparison PDFDanielValadãoBastosAinda não há avaliações

- Niculina GheorghitaDocumento7 páginasNiculina GheorghitaAna Popescu100% (1)

- Credit Analysis Partener Prompt 1 - Linie CreditDocumento15 páginasCredit Analysis Partener Prompt 1 - Linie CredityayaAinda não há avaliações

- RO10 ProposalDocumento21 páginasRO10 ProposalDan EnicaAinda não há avaliações

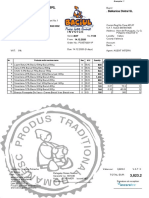

- Nr. Crt. Denumirea Produselor Sau A Serviciilor U.M. Cant Pret Unitar Valoarea Valoarea T.V.ADocumento1 páginaNr. Crt. Denumirea Produselor Sau A Serviciilor U.M. Cant Pret Unitar Valoarea Valoarea T.V.AGeorge B-gAinda não há avaliações

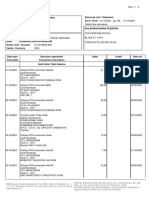

- Factura FACTURA SVS 006520 SVS 006520: Furnizor ClientDocumento1 páginaFactura FACTURA SVS 006520 SVS 006520: Furnizor Clientlaumany2012Ainda não há avaliações

- SC Meridian Agroind SRL: - Balkanica Distral SLDocumento2 páginasSC Meridian Agroind SRL: - Balkanica Distral SLMeridian AgroindAinda não há avaliações

- SV38850342000 2023 07Documento3 páginasSV38850342000 2023 07evelinaioanaAinda não há avaliações

- Pe Perioada: 01-09-2023 - 30-09-2023 EXTRAS DE CONT Nr. 4 Din Data: 20-01-2024Documento11 páginasPe Perioada: 01-09-2023 - 30-09-2023 EXTRAS DE CONT Nr. 4 Din Data: 20-01-2024chitoiu.razAinda não há avaliações

- F 39343900 ngs0404 30-11-2022 30112022 134801Documento1 páginaF 39343900 ngs0404 30-11-2022 30112022 134801Reta BulardaAinda não há avaliações

- FCO KRISHNAAG BUSINESS ENTERPRISE LLC DUBAI L Icumsa Cane Sugar 300 K CIF UAE TOTS 01.09 BebDocumento5 páginasFCO KRISHNAAG BUSINESS ENTERPRISE LLC DUBAI L Icumsa Cane Sugar 300 K CIF UAE TOTS 01.09 BebLAXMI PRASAD RAO VINJAMURIAinda não há avaliações

- SV39786361600 2023 10Documento6 páginasSV39786361600 2023 10ioanateodorabaisanAinda não há avaliações

- 2104 Agenda To UploadDocumento10 páginas2104 Agenda To Uploadapi-320633238Ainda não há avaliações

- Factura Proforma: Nr. CRT Denumirea Produselor Sau A Serviciilor U.M. Cant. Pret Unitar - Lei-Valoarea - LeiDocumento1 páginaFactura Proforma: Nr. CRT Denumirea Produselor Sau A Serviciilor U.M. Cant. Pret Unitar - Lei-Valoarea - LeiAdrian OlteanuAinda não há avaliações

- TOBACCODocumento3 páginasTOBACCODesire JoshuaAinda não há avaliações

- SV22108422500 2023 09Documento4 páginasSV22108422500 2023 09ileaalina6Ainda não há avaliações

- Iunie 2020: Payu Emag - Ro/MarketDocumento3 páginasIunie 2020: Payu Emag - Ro/MarketNicu TudosăAinda não há avaliações

- Your TM Bill: Page 1 of 6 Level 51, Menara TM, 50672 Kuala Lumpur ST ID: W10-1808-31001554Documento6 páginasYour TM Bill: Page 1 of 6 Level 51, Menara TM, 50672 Kuala Lumpur ST ID: W10-1808-31001554Cikgu Jorasmin IsaAinda não há avaliações

- Pe Perioada: 01-02-2023 - 12-02-2023 EXTRAS DE CONT Nr. 3 Din Data: 12-02-2023Documento6 páginasPe Perioada: 01-02-2023 - 12-02-2023 EXTRAS DE CONT Nr. 3 Din Data: 12-02-2023wyrdnt6yg4Ainda não há avaliações

- SV90483973000 2023 09Documento9 páginasSV90483973000 2023 09Alina DinuAinda não há avaliações

- Citybank StatementDocumento4 páginasCitybank StatementrampidrabbitmoulikAinda não há avaliações

- Pro Forma Vietnam DPDocumento4 páginasPro Forma Vietnam DPAfanAinda não há avaliações

- Sprintzproducts. CLCDocumento3 páginasSprintzproducts. CLCOim IbrahimAinda não há avaliações

- Documentación - Olha Hurkina Es - en TJDocumento23 páginasDocumentación - Olha Hurkina Es - en TJOlha HurkinaAinda não há avaliações

- Pe Perioada: 01-02-2023 - 15-02-2023 EXTRAS DE CONT Nr. 2 Din Data: 15-02-2023Documento3 páginasPe Perioada: 01-02-2023 - 15-02-2023 EXTRAS DE CONT Nr. 2 Din Data: 15-02-2023Alex Nicolaie IvanAinda não há avaliações

- Company Profile PT. Osa Bumi MemoriesDocumento19 páginasCompany Profile PT. Osa Bumi MemoriesAndika Dwi Rendra GrahaAinda não há avaliações

- SV10415631400 2024 02Documento6 páginasSV10415631400 2024 02anghelalin19Ainda não há avaliações

- EuropumpDocumento1 páginaEuropumpConstantinAinda não há avaliações

- Wuthiphong ChueasukDocumento5 páginasWuthiphong ChueasukITAinda não há avaliações

- StatementDocumento1 páginaStatementdaria melnykAinda não há avaliações

- 2011 Agenda To UploadDocumento15 páginas2011 Agenda To Uploadapi-320633238Ainda não há avaliações

- F 28898662 Ihc03974 25-08-2021 25082021 082137Documento1 páginaF 28898662 Ihc03974 25-08-2021 25082021 082137Sena DraceaAinda não há avaliações

- A Business in The Lake Resorts in RomaniaDocumento34 páginasA Business in The Lake Resorts in RomaniavaleriaAinda não há avaliações

- F - Robot LegumeDocumento1 páginaF - Robot LegumeEmanuel PaunAinda não há avaliações

- Invoice Flomih & Vio Bussines SRL: CX Ref: 18969800 Invoice No.: 151140-837 Invoice Date: 28 Nov 2019Documento1 páginaInvoice Flomih & Vio Bussines SRL: CX Ref: 18969800 Invoice No.: 151140-837 Invoice Date: 28 Nov 2019calinmusceleanuAinda não há avaliações

- Subject: Risk and Risk Analysis Company: Pomina Steel CompanyDocumento17 páginasSubject: Risk and Risk Analysis Company: Pomina Steel CompanyBii HeeAinda não há avaliações

- Kompania "KOLOSIAN KRISTAL" Sh.p.k,. ALBANIA Business Plan: Tirane, April 2022Documento3 páginasKompania "KOLOSIAN KRISTAL" Sh.p.k,. ALBANIA Business Plan: Tirane, April 2022ShefkiAinda não há avaliações

- Cash & Cash Equivalents (Viajar Basis)Documento38 páginasCash & Cash Equivalents (Viajar Basis)Nicole Daphne FigueroaAinda não há avaliações

- Ingles Tecnico I - OracionesDocumento3 páginasIngles Tecnico I - OracionesJuan CuadrosAinda não há avaliações

- Detailed StatementDocumento2 páginasDetailed Statementnisha.yusuf.infAinda não há avaliações

- Banking Law Notes 11Documento4 páginasBanking Law Notes 11Afiqah IsmailAinda não há avaliações

- People Vs Puig and PorrasDocumento1 páginaPeople Vs Puig and Porraskarl doceoAinda não há avaliações

- 1592827567uestions On Scale 0 To 1 Exam of UBGBDocumento16 páginas1592827567uestions On Scale 0 To 1 Exam of UBGBUmesh DewanganAinda não há avaliações

- Church Street Health Management Bankruptcy Docket 3:12-bk-01573Documento62 páginasChurch Street Health Management Bankruptcy Docket 3:12-bk-01573Dentist The MenaceAinda não há avaliações

- Software Project PlanDocumento6 páginasSoftware Project PlanMohamed Abdallah ZaghlolAinda não há avaliações

- Rail E-Ticket NR251272595406 PNR 8148697124 LTT-HUPDocumento2 páginasRail E-Ticket NR251272595406 PNR 8148697124 LTT-HUPParshu SaduwalaAinda não há avaliações

- Diploma in Nautical Sciences: February 2020Documento8 páginasDiploma in Nautical Sciences: February 2020From My CamAinda não há avaliações

- Deloitte Economic Outlook 2010Documento40 páginasDeloitte Economic Outlook 20103bandhuAinda não há avaliações

- Movimientos HistoricosDocumento22 páginasMovimientos HistoricosVerónica RodAinda não há avaliações

- Preweek Handouts in Business Law May 2014 BatchDocumento8 páginasPreweek Handouts in Business Law May 2014 BatchPhilip CastroAinda não há avaliações

- Lotto Payment Verification FormDocumento1 páginaLotto Payment Verification Formfandhi100% (17)

- Banks Cannot Own PropertyDocumento1 páginaBanks Cannot Own Propertythenjhomebuyer50% (2)

- Digest Revised: Au Amwao Full DescriptionDocumento1 páginaDigest Revised: Au Amwao Full DescriptionMackie SaidAinda não há avaliações

- Mt2014 01 Virtual CurrencyDocumento5 páginasMt2014 01 Virtual CurrencydinbitsAinda não há avaliações

- BIN Checker, Online BIN List Lookup From Free BIN DatabaseDocumento1 páginaBIN Checker, Online BIN List Lookup From Free BIN DatabaseROMEO PEPNIKUAinda não há avaliações

- PartnershipDocumento28 páginasPartnershipAdi Murthy100% (2)

- Irctcs E-Ticketing Service Electronic Reservation Slip (Personal User)Documento2 páginasIrctcs E-Ticketing Service Electronic Reservation Slip (Personal User)Sanjit SenAinda não há avaliações

- AmarBill - Online Flexiload Bangladesh - Grameenphone, Banglalink, Airtel, Robi, Citycell Mobile RechargeDocumento6 páginasAmarBill - Online Flexiload Bangladesh - Grameenphone, Banglalink, Airtel, Robi, Citycell Mobile RechargeJm RedwanAinda não há avaliações

- BucurestiDocumento84 páginasBucurestiDaniel MihailaAinda não há avaliações

- SecuritizationDocumento146 páginasSecuritizationSaurabh ParasharAinda não há avaliações

- Chap 008Documento17 páginasChap 008Ela PelariAinda não há avaliações

- DfggyuujjDocumento2 páginasDfggyuujjJornel MandiaAinda não há avaliações

- Financial Statement Analysis of Habib BankDocumento87 páginasFinancial Statement Analysis of Habib Bankhelperforeu56% (9)

- AssignmentDocumento4 páginasAssignmentMahamAinda não há avaliações

- A Study On Factors Influencing Use of Credit Cards in Context of Kathmandu ValleyDocumento56 páginasA Study On Factors Influencing Use of Credit Cards in Context of Kathmandu ValleyPrajjwol Bikram Khadka100% (2)

- Declaration of Deposit Capitalix enDocumento1 páginaDeclaration of Deposit Capitalix enYORDAN YAFFET ARAUJO ARAUJOAinda não há avaliações

- Chapter 20 - The Exchange Rate System and The Balance of Payments (Part 2)Documento8 páginasChapter 20 - The Exchange Rate System and The Balance of Payments (Part 2)ohyeajcrocksAinda não há avaliações