Você também pode gostar

- A Practical Guide to ETF Trading Systems: A systematic approach to trading exchange-traded fundsNo EverandA Practical Guide to ETF Trading Systems: A systematic approach to trading exchange-traded fundsNota: 5 de 5 estrelas5/5 (1)

- Case Background: Bhupesh Kumar (B18018)Documento7 páginasCase Background: Bhupesh Kumar (B18018)Bhupesh KumarAinda não há avaliações

- Stock Price Analysis Through Statistical And Data Science Tools: an OverviewNo EverandStock Price Analysis Through Statistical And Data Science Tools: an OverviewAinda não há avaliações

- Assignment No2Documento14 páginasAssignment No2sarvesh patilAinda não há avaliações

- Ratio Analysis: S.ClementDocumento32 páginasRatio Analysis: S.ClementJugal ShahAinda não há avaliações

- Portfolio Analysis To Determine Which Mutual Fund To Buy: ObjectiveDocumento8 páginasPortfolio Analysis To Determine Which Mutual Fund To Buy: ObjectiveAmey PataleAinda não há avaliações

- Balkrishna Industries - SharanDocumento4 páginasBalkrishna Industries - Sharanshaaqib mansuriAinda não há avaliações

- Bottom Up BetaDocumento8 páginasBottom Up Betamuthu_theone6943Ainda não há avaliações

- List of 30 Highest Dividend Paying Stocks in IndiaDocumento5 páginasList of 30 Highest Dividend Paying Stocks in IndiaPankajAinda não há avaliações

- Investment Portfolio Management: Final AssignmentDocumento7 páginasInvestment Portfolio Management: Final AssignmentShahzeb AliAinda não há avaliações

- Bajaj Finserv Arbitrage Fund - One Pager-1Documento2 páginasBajaj Finserv Arbitrage Fund - One Pager-1padmaniaAinda não há avaliações

- Running Head: Mutual FundsDocumento9 páginasRunning Head: Mutual FundsCarlos AlphonceAinda não há avaliações

- NIFTY 100: Index Returns (%) QTD YTD 1 Year 5 Years Since InceptionDocumento4 páginasNIFTY 100: Index Returns (%) QTD YTD 1 Year 5 Years Since InceptionYash SonkarAinda não há avaliações

- Analysis of Stocks of Small Companies: Amit V. Kanneshwar, F2, SS 08 - 10, IIPM BangaloreDocumento17 páginasAnalysis of Stocks of Small Companies: Amit V. Kanneshwar, F2, SS 08 - 10, IIPM BangalorekanneamitAinda não há avaliações

- Estimating Risk Parameters and Costs of Financing: Solutions To Investment ValuationDocumento9 páginasEstimating Risk Parameters and Costs of Financing: Solutions To Investment ValuationqazxswAinda não há avaliações

- BBMF 2093 Corporate FinanceDocumento6 páginasBBMF 2093 Corporate FinanceXUE WEI KONGAinda não há avaliações

- DSP Dec 2021Documento97 páginasDSP Dec 2021RUDRAKSH KARNIKAinda não há avaliações

- Basicsofsharemarket 170327071022 PDFDocumento33 páginasBasicsofsharemarket 170327071022 PDFHEROKAinda não há avaliações

- End Game: Number of Firms Beta Cost of Equity D/ (D+E)Documento15 páginasEnd Game: Number of Firms Beta Cost of Equity D/ (D+E)carminatAinda não há avaliações

- Ishares Msci Usa Momentum Factor Etf: Fact Sheet As of 03/31/2021Documento3 páginasIshares Msci Usa Momentum Factor Etf: Fact Sheet As of 03/31/20215ty5Ainda não há avaliações

- Risk and ReturnDocumento6 páginasRisk and ReturnKaushlesh KumarAinda não há avaliações

- Fin 435 Investment Theory Section-9 Semester: Spring 2019 Submitted To: Sayba Kamal Athoi (SBK) Group Project Phase 1Documento5 páginasFin 435 Investment Theory Section-9 Semester: Spring 2019 Submitted To: Sayba Kamal Athoi (SBK) Group Project Phase 1Robin Rahman 1711948030Ainda não há avaliações

- Altman's Z-ScoreDocumento15 páginasAltman's Z-ScoreVipul BhagatAinda não há avaliações

- Risk ReturnDocumento17 páginasRisk ReturnNikhil TurkarAinda não há avaliações

- FM Final ProjectDocumento21 páginasFM Final Projectharsh guptaAinda não há avaliações

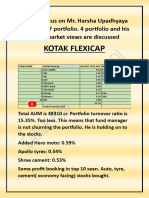

- Kotak Harsha Upadhyaya PortfolioDocumento8 páginasKotak Harsha Upadhyaya PortfoliomiddlecricketwarriorsAinda não há avaliações

- CH 4 SolnsDocumento6 páginasCH 4 SolnsAnindita SahaAinda não há avaliações

- UnleveredDocumento7 páginasUnleveredMohammadOmarFaruqAinda não há avaliações

- Name Wt. / Stock (%) : Primario FundDocumento2 páginasName Wt. / Stock (%) : Primario FundRakshan ShahAinda não há avaliações

- A Case Study On COkeDocumento6 páginasA Case Study On COkeDulon DuttaAinda não há avaliações

- BMO Equal Weight U.S. Health Care Hedged To CAD Index ETF: Data As of Mar 29, 2018Documento2 páginasBMO Equal Weight U.S. Health Care Hedged To CAD Index ETF: Data As of Mar 29, 2018Ramandeep ChauhanAinda não há avaliações

- Final Submission MANAC - Group 8 - Sec DDocumento33 páginasFinal Submission MANAC - Group 8 - Sec DShilpi KumariAinda não há avaliações

- BAC3684 Tutorial 6QDocumento6 páginasBAC3684 Tutorial 6Q1191103342Ainda não há avaliações

- V MartDocumento2 páginasV Martsaarthak srivastavaAinda não há avaliações

- Minimum Volatility 3Q 2022Documento4 páginasMinimum Volatility 3Q 2022ag rAinda não há avaliações

- ICICI Prudential Discovery Fund Does Just That. by Exploiting TheDocumento6 páginasICICI Prudential Discovery Fund Does Just That. by Exploiting TheMohammed Khurshid GauriAinda não há avaliações

- Ishares Msci Emerging Markets Etf: Fact Sheet As of 03/31/2021Documento3 páginasIshares Msci Emerging Markets Etf: Fact Sheet As of 03/31/2021hkm_gmat4849Ainda não há avaliações

- A Technical and Fundamental Analysis of Two Indian StocksDocumento7 páginasA Technical and Fundamental Analysis of Two Indian StockselizabethAinda não há avaliações

- SPDR S&P Midcap 400 ETF Trust: Fund Inception Date Cusip Key Features About This BenchmarkDocumento2 páginasSPDR S&P Midcap 400 ETF Trust: Fund Inception Date Cusip Key Features About This BenchmarkmuaadhAinda não há avaliações

- Effect of Liquidity On Size PremiumDocumento39 páginasEffect of Liquidity On Size PremiumfulconAinda não há avaliações

- Tata Motors LTD Class A: Nse: TatamtrdvrDocumento4 páginasTata Motors LTD Class A: Nse: TatamtrdvrHimanshu SinghAinda não há avaliações

- Case-Midland - C5Documento4 páginasCase-Midland - C5sumeet kumarAinda não há avaliações

- Abhi-Asmi International Private Limited-02232012Documento4 páginasAbhi-Asmi International Private Limited-02232012hesham zakiAinda não há avaliações

- Fooling The PeopleDocumento4 páginasFooling The PeopleManoj PadmanabhanAinda não há avaliações

- Bba 2011-2Documento17 páginasBba 2011-2xiaoM93Ainda não há avaliações

- Nifty Low VolatilityDocumento2 páginasNifty Low VolatilityRajesh KumarAinda não há avaliações

- Portfolio Assingment Arbitrage Fund 2Documento9 páginasPortfolio Assingment Arbitrage Fund 2Mayank AggarwalAinda não há avaliações

- End Game: Number of Firms Beta ROE Cost of Equity (Roe - Coe) BV of Equity Equity EVA ROCDocumento18 páginasEnd Game: Number of Firms Beta ROE Cost of Equity (Roe - Coe) BV of Equity Equity EVA ROCCinthiaAinda não há avaliações

- Group 3 FM Project IT IndustryDocumento13 páginasGroup 3 FM Project IT IndustryPS KannanAinda não há avaliações

- Tata Whole Life Mid Cap Equity FundDocumento1 páginaTata Whole Life Mid Cap Equity FundK Dviya VennelaAinda não há avaliações

- Assignment QuestionsDocumento5 páginasAssignment QuestionsRAJAT BANSAL0% (1)

- Daily Stock Market Report SampleDocumento2 páginasDaily Stock Market Report SampleVikash GoelAinda não há avaliações

- A Study On Optimal Portfolio Construction Using Sharpes Single Index Model With Special Preference To Selected Sectors Listed in NSEDocumento4 páginasA Study On Optimal Portfolio Construction Using Sharpes Single Index Model With Special Preference To Selected Sectors Listed in NSEsur yonoAinda não há avaliações

- CBM Practical 3 - 109 - 156 - 244 - 270Documento9 páginasCBM Practical 3 - 109 - 156 - 244 - 270Sandeep MishraAinda não há avaliações

- SAPM AssignmentDocumento12 páginasSAPM Assignmentshobhitkhare1984Ainda não há avaliações

- Asia Media Group Berhad - Proposed Rights Issue of Shares With Warrants - 130814Documento2 páginasAsia Media Group Berhad - Proposed Rights Issue of Shares With Warrants - 130814zseyo1Ainda não há avaliações

- Pricing Strategies Are A SometimesDocumento2 páginasPricing Strategies Are A SometimesAshish KhandelwalAinda não há avaliações

- FINA 410 Exercises NOV PDFDocumento7 páginasFINA 410 Exercises NOV PDFDrSwati BhargavaAinda não há avaliações

- FIN 6060 Module 3 Worksheet (Milestone 1)Documento5 páginasFIN 6060 Module 3 Worksheet (Milestone 1)r.olanibi5550% (2)

- Applied Corporate Finance Project For M/s. Titan Company LTDDocumento14 páginasApplied Corporate Finance Project For M/s. Titan Company LTDLuther KingAinda não há avaliações

- CP Cropping Pattern Self NotesDocumento21 páginasCP Cropping Pattern Self NotesAshok ChakravarthyAinda não há avaliações

- Valuation of Crossborder M&ADocumento55 páginasValuation of Crossborder M&AAshok ChakravarthyAinda não há avaliações

- Social AccountabilityDocumento53 páginasSocial AccountabilityAshok Chakravarthy100% (1)

- Rupee Depreciation - Probable Causes and OutlookDocumento10 páginasRupee Depreciation - Probable Causes and OutlookAshok ChakravarthyAinda não há avaliações

- Financial Accounting 02Documento48 páginasFinancial Accounting 02Ashok ChakravarthyAinda não há avaliações

- Advtgs and Disadvtgs-IfRSDocumento2 páginasAdvtgs and Disadvtgs-IfRSAshok ChakravarthyAinda não há avaliações

- Bonds and Their ValuationDocumento7 páginasBonds and Their ValuationRoyce Maenard EstanislaoAinda não há avaliações

- Robusta Coffee Shop A Feasibility StudyDocumento26 páginasRobusta Coffee Shop A Feasibility StudysabberAinda não há avaliações

- USA State-Wise Email Leads PDFDocumento6 páginasUSA State-Wise Email Leads PDFSimeon Dwight100% (1)

- Questions 2Documento8 páginasQuestions 2Test DriveAinda não há avaliações

- Price Elasticity of Demand (PED) : Price. PED (Of A Product) % Change in Quantity Demanded / % Change in PriceDocumento4 páginasPrice Elasticity of Demand (PED) : Price. PED (Of A Product) % Change in Quantity Demanded / % Change in PriceHmzaa Omer PuriAinda não há avaliações

- CH 07Documento56 páginasCH 07SuperAinda não há avaliações

- Marketing ResearchDocumento14 páginasMarketing ResearchRajalaxmi pAinda não há avaliações

- Vikash Kumar LL.M Dissertation 2022Documento145 páginasVikash Kumar LL.M Dissertation 2022Raj SinhaAinda não há avaliações

- Chapter - 18 Marketing RNDDocumento41 páginasChapter - 18 Marketing RNDDuyên VõAinda não há avaliações

- Call Outs For Blade HQDocumento73 páginasCall Outs For Blade HQSnöBer GardenAinda não há avaliações

- Porter's Five ForcesDocumento3 páginasPorter's Five ForcesBibhuti SahuAinda não há avaliações

- QFIP-159-F23 Private Debt Fund Returns, Persistence, and Market ConditionsDocumento54 páginasQFIP-159-F23 Private Debt Fund Returns, Persistence, and Market ConditionsNoodles FSA100% (1)

- Case Study Market LeadershipDocumento5 páginasCase Study Market LeadershipDanish RehmanAinda não há avaliações

- Green Hay Ven STEM 12 11 Business PlanDocumento73 páginasGreen Hay Ven STEM 12 11 Business Planオンタニージア ミルAinda não há avaliações

- Clothing Retailing - UK - 2022 - BrochureDocumento4 páginasClothing Retailing - UK - 2022 - BrochureMainak PaulAinda não há avaliações

- The State of Ecommerce 2021: Navigating The New World of Omnichannel Commerce and Retail MediaDocumento38 páginasThe State of Ecommerce 2021: Navigating The New World of Omnichannel Commerce and Retail MediaDaria B100% (1)

- New ,,,,suzuki QuestionnaireDocumento3 páginasNew ,,,,suzuki Questionnaireviradiyajatin100% (2)

- SIP ReportDocumento111 páginasSIP ReportDesarollo OrganizacionalAinda não há avaliações

- Marketing AnalyitcsDocumento25 páginasMarketing Analyitcsnnbphuong81Ainda não há avaliações

- 601b9f7c3988930021ce6845-1612423290-CHAPTER 2 - BUILDING CUSTOMER LOYALTY THROUGH CUSTOMER SERVICEDocumento5 páginas601b9f7c3988930021ce6845-1612423290-CHAPTER 2 - BUILDING CUSTOMER LOYALTY THROUGH CUSTOMER SERVICEDomingo VillanuevaAinda não há avaliações

- Limited Brands PresentationDocumento49 páginasLimited Brands PresentationIda ManAinda não há avaliações

- Week 2 Solutions To ExercisesDocumento5 páginasWeek 2 Solutions To ExercisesBerend van RoozendaalAinda não há avaliações

- Auctions Slides Part1Documento17 páginasAuctions Slides Part1Eva MorinAinda não há avaliações

- Topic 4. Marketing Information and ResearchDocumento36 páginasTopic 4. Marketing Information and ResearchБогдана ВишнівськаAinda não há avaliações

- AP Topic 9 FuturesDocumento35 páginasAP Topic 9 Futuressumail wangAinda não há avaliações

- The 2 - Ques Fin2603 S1 2022Documento2 páginasThe 2 - Ques Fin2603 S1 2022btsj43254Ainda não há avaliações

- Case Study ScenarioDocumento4 páginasCase Study ScenariokamarulzamaniAinda não há avaliações

- BUS100 Sample Final Chaps 11-16Documento16 páginasBUS100 Sample Final Chaps 11-16Muhammad SaeedAinda não há avaliações

- Mini Case - Blades - Decision To Expand InternationallyDocumento2 páginasMini Case - Blades - Decision To Expand InternationallyTrường Nguyễn VănAinda não há avaliações

- Strategic Analysis of Onida: Assignment For Strategic MarketingDocumento13 páginasStrategic Analysis of Onida: Assignment For Strategic MarketingVikas NigamAinda não há avaliações