Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (120)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- All Fiori ApplicationDocumento49 páginasAll Fiori ApplicationRehan KhanAinda não há avaliações

- Grav SoluDocumento3 páginasGrav SoluAfolabi Eniola Abiola0% (1)

- Nestle - Coffee - Supply Chain PDFDocumento2 páginasNestle - Coffee - Supply Chain PDFAnirudh Kowtha60% (5)

- OneChicago Fact SheetDocumento1 páginaOneChicago Fact SheetJosh AlexanderAinda não há avaliações

- GIO+Course 3 Email Marketing Tahir AshrafDocumento17 páginasGIO+Course 3 Email Marketing Tahir AshrafSayed tahir Ashraf100% (1)

- Marketing NewwwwDocumento25 páginasMarketing NewwwwAhmer RazaAinda não há avaliações

- Asset Management - Lecture 1Documento33 páginasAsset Management - Lecture 1goncalo_almeida92Ainda não há avaliações

- Case Study - Aravind EyeDocumento8 páginasCase Study - Aravind EyeAnirudh KowthaAinda não há avaliações

- Healthymagination at Ge Healthcare SystemsDocumento2 páginasHealthymagination at Ge Healthcare SystemsAnirudh Kowtha100% (1)

- Achieving Relationship Marketing Effectiveness PDFDocumento18 páginasAchieving Relationship Marketing Effectiveness PDFAnirudh KowthaAinda não há avaliações

- Dynamix Dairy Industries Limited PDFDocumento72 páginasDynamix Dairy Industries Limited PDFAnirudh KowthaAinda não há avaliações

- Green Supply Chain ManagementDocumento10 páginasGreen Supply Chain ManagementAnirudh KowthaAinda não há avaliações

- Agent Based b2b MKT PlaceDocumento16 páginasAgent Based b2b MKT PlaceAnirudh KowthaAinda não há avaliações

- The Seven Dimensions of CultureDocumento8 páginasThe Seven Dimensions of CultureAnirudh KowthaAinda não há avaliações

- Medical Device Growth in Emerging Markets InVivo 1206Documento9 páginasMedical Device Growth in Emerging Markets InVivo 1206amirefAinda não há avaliações

- Services Marketing Case Study: Aravind Eye CareDocumento9 páginasServices Marketing Case Study: Aravind Eye CareAnirudh KowthaAinda não há avaliações

- Investor SoftDocumento14 páginasInvestor Soft167supaulAinda não há avaliações

- The Five Competitive Forces That Shape StrategyDocumento18 páginasThe Five Competitive Forces That Shape StrategyAnirudh KowthaAinda não há avaliações

- Case Study - Aravind EyeDocumento8 páginasCase Study - Aravind EyeAnirudh KowthaAinda não há avaliações

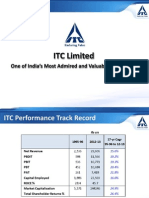

- ITC Corporate Presentation PDFDocumento56 páginasITC Corporate Presentation PDFNeha Bhomia GuptaAinda não há avaliações

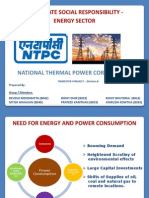

- Corporate Social Responsibility - Energy Sector: National Thermal Power CorporationDocumento23 páginasCorporate Social Responsibility - Energy Sector: National Thermal Power CorporationAnirudh KowthaAinda não há avaliações

- Eight Levers SIDocumento18 páginasEight Levers SIatuletrxAinda não há avaliações

- Yahoo Turnaround StatisticsDocumento2 páginasYahoo Turnaround StatisticsAnirudh KowthaAinda não há avaliações

- Automation KivaDocumento25 páginasAutomation KivaAnirudh KowthaAinda não há avaliações

- Rising Fuel CostsDocumento12 páginasRising Fuel CostsAnirudh KowthaAinda não há avaliações

- Case Study of Titan Integrated Marketing Communication StrategiesDocumento8 páginasCase Study of Titan Integrated Marketing Communication StrategiesG S Sreekiran0% (2)

- Marico PresentationDocumento11 páginasMarico PresentationAnirudh KowthaAinda não há avaliações

- Store Perform and Cust MGMTDocumento33 páginasStore Perform and Cust MGMTAnirudh KowthaAinda não há avaliações

- NTPC - Critical Analysis of Initatives: "To Be The World's Largest and Best Power Producer, Powering India's Growth."Documento6 páginasNTPC - Critical Analysis of Initatives: "To Be The World's Largest and Best Power Producer, Powering India's Growth."Anirudh KowthaAinda não há avaliações

- Managing Brands A AkerDocumento19 páginasManaging Brands A AkerAnirudh KowthaAinda não há avaliações

- RF Fundamentals PcomDocumento64 páginasRF Fundamentals PcomAnirudh KowthaAinda não há avaliações

- 2579 MicrosoftPowerPoint2010 RTM WSG ExternalDocumento10 páginas2579 MicrosoftPowerPoint2010 RTM WSG ExternalCherlyne DavidAinda não há avaliações

- The State of Employer Branding: A Global Report On The Hottest Topic in Talent AcquisitionDocumento33 páginasThe State of Employer Branding: A Global Report On The Hottest Topic in Talent AcquisitionAnirudh KowthaAinda não há avaliações

- Newell CompanyDocumento26 páginasNewell CompanyAnirudh Kowtha100% (1)

- David Kolb's Learning Styles Model and Experiential Learning Theory (ELT)Documento10 páginasDavid Kolb's Learning Styles Model and Experiential Learning Theory (ELT)Anirudh Kowtha0% (1)

- Forecasting Revenues and CostsDocumento17 páginasForecasting Revenues and CostsNÄ DÏÄAinda não há avaliações

- Advanced Marketing IssuesDocumento14 páginasAdvanced Marketing IssuesLara Nicole PajaroAinda não há avaliações

- Economics (Eco 415) Assignment 3 QAMA 2 (202041)Documento5 páginasEconomics (Eco 415) Assignment 3 QAMA 2 (202041)Ummu KhashiaAinda não há avaliações

- What Is Amazon's Customer Value Proposition? (What Are The Merits of This Proposition? Has It Changed Over Time? How Should It Evolve in The Future?)Documento9 páginasWhat Is Amazon's Customer Value Proposition? (What Are The Merits of This Proposition? Has It Changed Over Time? How Should It Evolve in The Future?)Surbhi JainAinda não há avaliações

- BUS 2201 Discussion Forum Unit 2Documento1 páginaBUS 2201 Discussion Forum Unit 2Cherry HtunAinda não há avaliações

- 13Documento14 páginas13JDAinda não há avaliações

- XI Accountancy Project WorkDocumento1 páginaXI Accountancy Project Workkulsum bhopalAinda não há avaliações

- DBB2104 Unit-14Documento23 páginasDBB2104 Unit-14anamikarajendran441998Ainda não há avaliações

- Timex Case StudyDocumento36 páginasTimex Case StudyShrey KashyapAinda não há avaliações

- 5 30 2022 6:15:45 PM PDFDocumento3 páginas5 30 2022 6:15:45 PM PDFThy TanaAinda não há avaliações

- Investor Presentation (Company Update)Documento18 páginasInvestor Presentation (Company Update)Shyam SunderAinda não há avaliações

- Exploitation of New BusinessDocumento2 páginasExploitation of New BusinessRai AhmedAinda não há avaliações

- Advertising Appropriation Methods & Emerging Forms of AdvertisingDocumento106 páginasAdvertising Appropriation Methods & Emerging Forms of Advertisingchetanprakash077Ainda não há avaliações

- Microsoft Word Analysis of Clothing Supply ChainDocumento20 páginasMicrosoft Word Analysis of Clothing Supply Chainagga1111Ainda não há avaliações

- Barilla SpaDocumento7 páginasBarilla SpaSatrajit Chakraborty100% (2)

- INDIVIDUAL ASSIGNMNENT - Ia - IB1708 - MKT101Documento9 páginasINDIVIDUAL ASSIGNMNENT - Ia - IB1708 - MKT101Nhi NgôAinda não há avaliações

- Company Profile StickEarnDocumento16 páginasCompany Profile StickEarnGalih Widayana PutraAinda não há avaliações

- Far 6815 - Gross Profit Method Far 6816 - Retail Inventory MethodDocumento2 páginasFar 6815 - Gross Profit Method Far 6816 - Retail Inventory MethodKent Raysil PamaongAinda não há avaliações

- Entrepreneurial Marketing: After Completion of The Course, The Students Will Be Able ToDocumento2 páginasEntrepreneurial Marketing: After Completion of The Course, The Students Will Be Able ToMurugan MAinda não há avaliações

- International Macroeconomics: Slides For Chapter 8: International Capital Market IntegrationDocumento54 páginasInternational Macroeconomics: Slides For Chapter 8: International Capital Market IntegrationM Kaderi KibriaAinda não há avaliações

- Inventories TheoryDocumento3 páginasInventories Theoryinfo4chaituAinda não há avaliações

- 2.0assessment Exam Problem 2Documento3 páginas2.0assessment Exam Problem 2Joe Honey Cañas Carbajosa100% (1)

- Review of OreoDocumento4 páginasReview of OreoNaincy Chhabra0% (1)

- Supply ChainDocumento39 páginasSupply ChainAuliaAinda não há avaliações