Você também pode gostar

- Draft EUETS Reform Legal TextDocumento32 páginasDraft EUETS Reform Legal TextCarbon Brief100% (1)

- State Aid Commission Approves Italian Scheme Under Recovery and Resilience Facility To Support Biomethane ProductionDocumento2 páginasState Aid Commission Approves Italian Scheme Under Recovery and Resilience Facility To Support Biomethane ProductionBalasubramani RanganathanAinda não há avaliações

- Practical Guide Gber enDocumento72 páginasPractical Guide Gber enAnonymous 6C6jgnrUAinda não há avaliações

- CELEX 32010L0030 enDocumento12 páginasCELEX 32010L0030 enMichalisCharalambousAinda não há avaliações

- HarmonisationDocumento27 páginasHarmonisationElda StefaAinda não há avaliações

- UntitledDocumento205 páginasUntitledRaihanAinda não há avaliações

- YenilenebilirenerjidirektifleriDocumento8 páginasYenilenebilirenerjidirektifleriKorkutYigitYigitalpAinda não há avaliações

- Meps Call For More Ambitious and Consumer-Focused Energy Targets Beyond 2020Documento2 páginasMeps Call For More Ambitious and Consumer-Focused Energy Targets Beyond 2020Monika PerezAinda não há avaliações

- Reg.1628 2006Documento12 páginasReg.1628 2006Nastasa DorinAinda não há avaliações

- Customs: Notification Nos. Date Tariff Non-Tariff Central Excise Tariff Non-TariffDocumento15 páginasCustoms: Notification Nos. Date Tariff Non-Tariff Central Excise Tariff Non-TariffsurampudiprasadAinda não há avaliações

- REDIIDocumento55 páginasREDIIMadalina GrigorescuAinda não há avaliações

- COM 2021 823 1 EN ACT Part1 v11Documento72 páginasCOM 2021 823 1 EN ACT Part1 v11claus_44Ainda não há avaliações

- ECS Checklist Crisis 17082022Documento17 páginasECS Checklist Crisis 17082022APointvoglAinda não há avaliações

- Council Directive 2004/67/ec of 26 April 2004 Concerning Measures To Safeguard Security of Natural Gas SupplyDocumento5 páginasCouncil Directive 2004/67/ec of 26 April 2004 Concerning Measures To Safeguard Security of Natural Gas SupplytoshaAinda não há avaliações

- Red IiiDocumento167 páginasRed Iiicjfelbol.4digitalAinda não há avaliações

- Passive Houses Legislation - Cons Cons (2010) 05386 (Rev3) enDocumento71 páginasPassive Houses Legislation - Cons Cons (2010) 05386 (Rev3) enkaliagraAinda não há avaliações

- 1 en Act Part1 v16 PDFDocumento22 páginas1 en Act Part1 v16 PDFMatevz PusnikAinda não há avaliações

- Explanatory Memorandum To The 2018 Carbon Tax Bill - 20 Nov 2018Documento28 páginasExplanatory Memorandum To The 2018 Carbon Tax Bill - 20 Nov 2018Jeannot MpianaAinda não há avaliações

- CARBON TAX - Corrigendum To Council Directive 2004:75:EC of 29 April 2004 Amending Directive 2003:96:ECDocumento2 páginasCARBON TAX - Corrigendum To Council Directive 2004:75:EC of 29 April 2004 Amending Directive 2003:96:ECSofia KentAinda não há avaliações

- Discussion Paper: by The Energy Community SecretariatDocumento25 páginasDiscussion Paper: by The Energy Community SecretariatEngineerAinda não há avaliações

- 2014 Energy Efficiency CommunicationDocumento27 páginas2014 Energy Efficiency CommunicationkktayAinda não há avaliações

- Environment Energy PolicyDocumento18 páginasEnvironment Energy Policydropkick94Ainda não há avaliações

- Export Rebates and The EU Carbon Border Adjustment Mechanism: WTO Law and Environmental ObjectionsDocumento22 páginasExport Rebates and The EU Carbon Border Adjustment Mechanism: WTO Law and Environmental ObjectionsAnnhAinda não há avaliações

- Redii Summary Eba 1Documento6 páginasRedii Summary Eba 1Ademar EstradaAinda não há avaliações

- State Aid Commission Approves 104 Million Croatian Scheme To Support Energy-Intensive CompaniesDocumento2 páginasState Aid Commission Approves 104 Million Croatian Scheme To Support Energy-Intensive CompaniesMateja NovakAinda não há avaliações

- Energy Tax Report 2019 PDFDocumento91 páginasEnergy Tax Report 2019 PDFanacatarinabarradasAinda não há avaliações

- State Aid: Commission Updates Guidance For Measures To Support The Green TransitionDocumento2 páginasState Aid: Commission Updates Guidance For Measures To Support The Green TransitionqyhupdxydcluwwfcjsAinda não há avaliações

- Mandate BioMethane Injection Into G+NG Grid - m475Documento4 páginasMandate BioMethane Injection Into G+NG Grid - m475goldanodragonzAinda não há avaliações

- The Article 10C Application by RomaniaDocumento24 páginasThe Article 10C Application by RomaniaRoxana IvanAinda não há avaliações

- CERC - Regulations 2009Documento166 páginasCERC - Regulations 2009Samir Kumar MondalAinda não há avaliações

- B Council Directive 92/42/eec of 21 May 1992 On Efficiency Requirements For New Hot-Water Boilers Fired With Liquid or Gaseous FuelsDocumento16 páginasB Council Directive 92/42/eec of 21 May 1992 On Efficiency Requirements For New Hot-Water Boilers Fired With Liquid or Gaseous Fuelsbzkizo_sbbAinda não há avaliações

- 02006L0032 20081211 enDocumento28 páginas02006L0032 20081211 enbzkizo_sbbAinda não há avaliações

- CBAM GutachtenDocumento44 páginasCBAM GutachtenAnnhAinda não há avaliações

- Renewable Energy StrategyDocumento10 páginasRenewable Energy Strategydanb1Ainda não há avaliações

- ECRB Dispute ResolutionDocumento52 páginasECRB Dispute ResolutionDivyanshu BaraiyaAinda não há avaliações

- Articulo en InglesDocumento24 páginasArticulo en InglesSantiago SandovalAinda não há avaliações

- Note 08Documento9 páginasNote 08nebojsavucinicAinda não há avaliações

- Assignment Task 2Documento11 páginasAssignment Task 2trungkien11a16Ainda não há avaliações

- Fuel Consumption Standards PDFDocumento18 páginasFuel Consumption Standards PDFRavi ShankarAinda não há avaliações

- Case Study: The EU Emissions Trading Scheme (EU ETS)Documento4 páginasCase Study: The EU Emissions Trading Scheme (EU ETS)sondaAinda não há avaliações

- 2018 2002 EuDocumento21 páginas2018 2002 EuAritra DasguptaAinda não há avaliações

- Mandato À CENDocumento3 páginasMandato À CENmayordomo5625Ainda não há avaliações

- 2011 7065 Decision Financing enDocumento8 páginas2011 7065 Decision Financing enJama JamazokaAinda não há avaliações

- X (G/KM) ADocumento17 páginasX (G/KM) AJohn Oneil F. QuiambaoAinda não há avaliações

- 2006 05 05 Consultation enDocumento14 páginas2006 05 05 Consultation enanjgarAinda não há avaliações

- The EU EmissionDocumento3 páginasThe EU EmissionhdvdfhiaAinda não há avaliações

- FuelEU Maritime Adopted by CouncilDocumento144 páginasFuelEU Maritime Adopted by CouncilJai KanadeAinda não há avaliações

- File 33272Documento44 páginasFile 33272EmOosh MohamedAinda não há avaliações

- Regulation EC 2022 - 996 - On VS Low iLUCDocumento62 páginasRegulation EC 2022 - 996 - On VS Low iLUCliliacul2000Ainda não há avaliações

- Offer Contract) Advanced Renewable Tariff or Energy PaymentDocumento2 páginasOffer Contract) Advanced Renewable Tariff or Energy PaymentDaniela AngejaAinda não há avaliações

- Green Paper UeDocumento16 páginasGreen Paper UeCarlos JAinda não há avaliações

- Energy Legislation: Primary Legislation in The Energy Field Also IncludesDocumento5 páginasEnergy Legislation: Primary Legislation in The Energy Field Also IncludesFrancesco SangregorioAinda não há avaliações

- Directive 2001 80 ENVDocumento27 páginasDirective 2001 80 ENVSergio PereiraAinda não há avaliações

- Memo For Road Map of Renewable EnergyDocumento4 páginasMemo For Road Map of Renewable EnergySaleh Al-TamimiAinda não há avaliações

- International Council On Clean Transportation Comments On The Inclusion of Alternative Fuels in The European Union's CO2 Standards For Trucks and BusesDocumento11 páginasInternational Council On Clean Transportation Comments On The Inclusion of Alternative Fuels in The European Union's CO2 Standards For Trucks and BusesThe International Council on Clean TransportationAinda não há avaliações

- Globalization Found BoeDocumento6 páginasGlobalization Found BoemagnoliablancaAinda não há avaliações

- EU Energy Policy PrinciplesDocumento8 páginasEU Energy Policy PrinciplesCimnaz IsmayilovaAinda não há avaliações

- State Aid RES ItaliaDocumento1 páginaState Aid RES ItaliaAnonymous IPF3W1FczAinda não há avaliações

- State Aid Commission Approves Belgian Certificates Schemes For Renewable Electricity and High-Efficiency Cogeneration in FlandersDocumento1 páginaState Aid Commission Approves Belgian Certificates Schemes For Renewable Electricity and High-Efficiency Cogeneration in FlandersJM OVAinda não há avaliações

- EU State Aid Control P.Werner PDFDocumento878 páginasEU State Aid Control P.Werner PDFAnonymous 6C6jgnrUAinda não há avaliações

- I Can I CantDocumento1 páginaI Can I CantAnonymous 6C6jgnrUAinda não há avaliações

- Sa Manproc en PDFDocumento256 páginasSa Manproc en PDFAnonymous 6C6jgnrUAinda não há avaliações

- Decizie Lubeck - Port Cale Ferata PDFDocumento10 páginasDecizie Lubeck - Port Cale Ferata PDFAnonymous 6C6jgnrUAinda não há avaliações

- Fise de Colorat LolDocumento1 páginaFise de Colorat LolAnonymous 6C6jgnrUAinda não há avaliações

- Decizie Aero Germania PDFDocumento21 páginasDecizie Aero Germania PDFAnonymous 6C6jgnrUAinda não há avaliações

- Decizie Aero Germania PDFDocumento21 páginasDecizie Aero Germania PDFAnonymous 6C6jgnrUAinda não há avaliações

- Agenda - Bucharest Workshop - V2Documento6 páginasAgenda - Bucharest Workshop - V2Anonymous 6C6jgnrUAinda não há avaliações

- 1 Write The Number That Comes Out When You Use The Number in The CircleDocumento5 páginas1 Write The Number That Comes Out When You Use The Number in The CircleAnonymous 6C6jgnrUAinda não há avaliações

- Policy Brief enDocumento5 páginasPolicy Brief enAnonymous 6C6jgnrUAinda não há avaliações

- Grid - ResearchDocumento6 páginasGrid - ResearchAnonymous 6C6jgnrUAinda não há avaliações

- Grid - Waste ManagementDocumento9 páginasGrid - Waste ManagementAnonymous 6C6jgnrUAinda não há avaliações

- Grid - PortsDocumento10 páginasGrid - PortsAnonymous 6C6jgnrUAinda não há avaliações

- Grid - Waste ManagementDocumento9 páginasGrid - Waste ManagementAnonymous 6C6jgnrUAinda não há avaliações

- Grid - Sports and MultifunctionalDocumento8 páginasGrid - Sports and MultifunctionalAnonymous 6C6jgnrUAinda não há avaliações

- Article 44 WikiDocumento4 páginasArticle 44 WikiAnonymous 6C6jgnrUAinda não há avaliações

- Maritime Guidelines - Final - 20180612Documento59 páginasMaritime Guidelines - Final - 20180612Anonymous 6C6jgnrUAinda não há avaliações

- Decizie Letonia - Aministie FiscalaDocumento6 páginasDecizie Letonia - Aministie FiscalaAnonymous 6C6jgnrUAinda não há avaliações

- Article 44 WikiDocumento4 páginasArticle 44 WikiAnonymous 6C6jgnrUAinda não há avaliações

- Answer - Aviation Guidelines - Art 51 (4) - Social Aid For Transport For Residents of Remote RegionsDocumento1 páginaAnswer - Aviation Guidelines - Art 51 (4) - Social Aid For Transport For Residents of Remote RegionsAnonymous 6C6jgnrUAinda não há avaliações

- Maths ButterfliesDocumento10 páginasMaths ButterfliesSandra Veronica Parra MarínAinda não há avaliações

- Raport MedicalDocumento2 páginasRaport MedicalAnonymous 6C6jgnrUAinda não há avaliações

- Maths RocketsDocumento12 páginasMaths RocketsdrfsjhkjkjhAinda não há avaliações

- "Up" Meaning To Finish: VerbsDocumento9 páginas"Up" Meaning To Finish: VerbsAnonymous 6C6jgnrUAinda não há avaliações

- GeneralDocumento5 páginasGeneralAnonymous 6C6jgnrUAinda não há avaliações

- The Feminine Giftbook v2.1Documento32 páginasThe Feminine Giftbook v2.1aura_rapeanu2720Ainda não há avaliações

- Decizie Letonia - Aministie FiscalaDocumento6 páginasDecizie Letonia - Aministie FiscalaAnonymous 6C6jgnrUAinda não há avaliações

- Wake Up Its SpringDocumento1 páginaWake Up Its SpringAnonymous 6C6jgnrUAinda não há avaliações

- WorksheetWorks Calculating Prices 1Documento2 páginasWorksheetWorks Calculating Prices 1Julie Navarro100% (2)

- FAR WEEK 6 NCAHS RevieweesDocumento3 páginasFAR WEEK 6 NCAHS RevieweesAdan NadaAinda não há avaliações

- Chap 5 VouchingDocumento20 páginasChap 5 VouchingAkash GuptaAinda não há avaliações

- Week 7 Module 7 TAX2 - Business and Transfer Taxation - PADAYHAGDocumento23 páginasWeek 7 Module 7 TAX2 - Business and Transfer Taxation - PADAYHAGfernan opeliñaAinda não há avaliações

- Certifications - PGMP Application FormDocumento15 páginasCertifications - PGMP Application FormManojJainAinda não há avaliações

- Dabistan-e-Ijtihaad - 99 Names of Holy Prophet Muhammad (Saw)Documento2 páginasDabistan-e-Ijtihaad - 99 Names of Holy Prophet Muhammad (Saw)Salman MirzaAinda não há avaliações

- Tax2 Ch15 Estate Taxes ReviewerDocumento7 páginasTax2 Ch15 Estate Taxes Reviewerlyle_roseAinda não há avaliações

- FINANCE ManualDocumento123 páginasFINANCE ManualcakotyAinda não há avaliações

- Feasibility StudiesDocumento17 páginasFeasibility Studiesdiosanjex100% (1)

- Cir v. LancasterDocumento2 páginasCir v. LancasterGlyza Kaye Zorilla PatiagAinda não há avaliações

- ACT InvoiceDocumento2 páginasACT InvoiceRajatHaldarAinda não há avaliações

- MPhil ThesisDocumento24 páginasMPhil ThesisArichandran AAinda não há avaliações

- Multiple Choice Questions in Tax Review Jan 5Documento1 páginaMultiple Choice Questions in Tax Review Jan 5Gileah ZuasolaAinda não há avaliações

- SRC Income Tax Drop Off FormDocumento2 páginasSRC Income Tax Drop Off FormArvind MishraAinda não há avaliações

- Cosmetic Product Producing PlantDocumento27 páginasCosmetic Product Producing Plantbig john100% (1)

- Employee TypesDocumento16 páginasEmployee TypesEmerson MichalAinda não há avaliações

- Corporate Governance, Incentives, and Tax AvoidanceDocumento17 páginasCorporate Governance, Incentives, and Tax AvoidanceWihelmina DeaAinda não há avaliações

- DRAFT Stay of Demand by CA NITIN KANWARDocumento13 páginasDRAFT Stay of Demand by CA NITIN KANWARAmandeep Vats91% (11)

- Deductions Under Chapter VI ADocumento6 páginasDeductions Under Chapter VI AbabatoofaniAinda não há avaliações

- Nism XV - Research Analyst Exam - Last Day Test 1Documento54 páginasNism XV - Research Analyst Exam - Last Day Test 1roja14% (7)

- Global Cash Card - Paystub Detail PDFDocumento1 páginaGlobal Cash Card - Paystub Detail PDFVerónica Del RioAinda não há avaliações

- LeanIX Whitepaper Nine Key Use Cases Solved With EADocumento15 páginasLeanIX Whitepaper Nine Key Use Cases Solved With EAEduardo ManchegoAinda não há avaliações

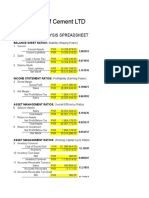

- Maple Leaf CementDocumento2 páginasMaple Leaf CementChampyAinda não há avaliações

- Introduction To Public FinanceDocumento32 páginasIntroduction To Public FinanceClaudine Aguiatan55% (11)

- MIECO 5001 Financial Report PDFDocumento130 páginasMIECO 5001 Financial Report PDFkoneiseongAinda não há avaliações

- BLTDocumento30 páginasBLTJemson Yandug0% (1)

- Economics Unit 4 NotesDocumento23 páginasEconomics Unit 4 NotestaymoorAinda não há avaliações

- Chapter 16 Homework SolutionsDocumento6 páginasChapter 16 Homework SolutionsJackAinda não há avaliações

- Transfer Taxes: Modes of Acquiring OwnershipDocumento31 páginasTransfer Taxes: Modes of Acquiring OwnershipMary Joy DenostaAinda não há avaliações

- IFM TB ch16Documento9 páginasIFM TB ch16Faizan Ch100% (1)